The traditional banking sector’s systemic inability to finalize complex commercial underwriting in under 45 days has effectively transformed conventional financing into a strategic liability for the modern institutional investor. You’ve likely experienced the frustration of seeing a prime acquisition fail because a legacy institution’s rigid credit parameters couldn’t account for the intrinsic value of a high-performing asset. Identifying sophisticated bridge loan lenders is no longer optional. It’s a fundamental requirement for the disciplined execution of private capital allocation in 2026.

This guide offers a rigorous analysis of the private debt landscape, providing the analytical tools necessary to identify partners who prioritize transparency and asset-based valuation over opaque fee structures. We’ll explore the specific criteria for vetting lenders who offer the speed and bespoke structuring required to secure high-value real estate assets in an increasingly competitive market. By the conclusion of this strategic overview, you’ll possess a clear roadmap for aligning with capital partners who share your commitment to long-term value creation and disciplined stewardship.

Key Takeaways

- Understand how to transition from reactive financing to a proactive capital allocation strategy that utilizes short-term liquidity as a tactical instrument for real estate acquisition.

- Identify the essential metrics for evaluating institutional bridge loan lenders, focusing on historical tenure and the transparency of complex fee structures.

- Quantify the risk-adjusted benefits of private capital over traditional banking institutions by analyzing the significant opportunity costs associated with prolonged approval timelines.

- Learn to structure bridge financing for optimal portfolio growth by meticulously aligning loan terms with the anticipated stabilization phases of high-value assets.

- Discover how a partnership grounded in three decades of industry stewardship can provide the bespoke financial solutions necessary for sophisticated wealth preservation.

The Strategic Role of Bridge Loan Lenders in Real Estate Capital Structures

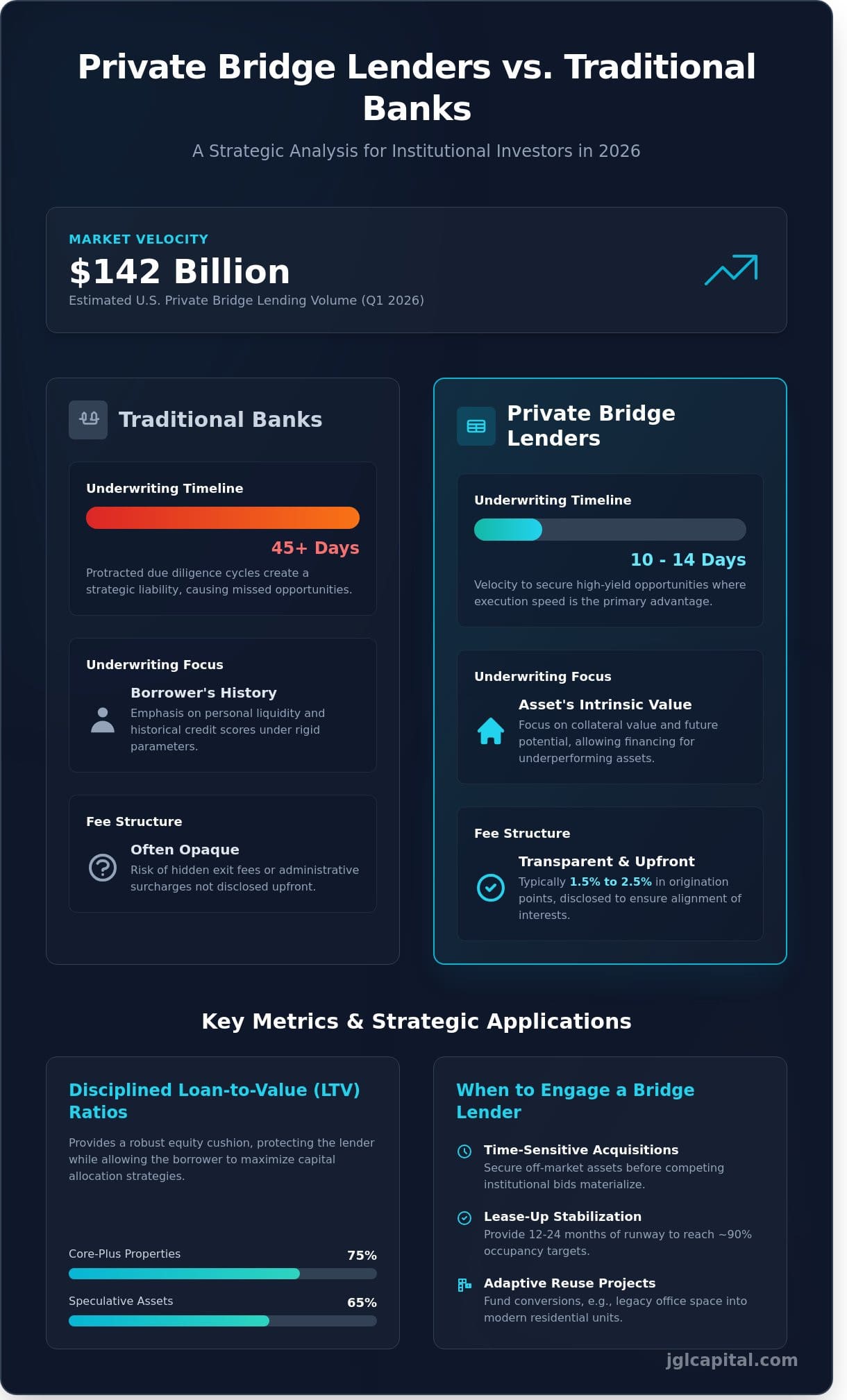

The contemporary financial landscape of 2026 identifies bridge loan lenders as essential architects of liquidity within sophisticated capital stacks. These entities provide the requisite velocity for institutional investors to secure high-yield opportunities long before traditional banking institutions can finalize their protracted due diligence cycles. The historical perception of bridge capital has undergone a fundamental transformation since the market corrections observed in 2023; it’s no longer categorized as a financing mechanism of last resort for distressed assets. Instead, disciplined fund managers utilize this debt as a proactive instrument to capture value in volatile environments where execution speed serves as the primary competitive advantage. By the first quarter of 2026, the volume of private bridge lending in the United States reached an estimated $142 billion, reflecting a calculated shift toward flexible, short-term debt structures that prioritize agility over low-cost, rigid alternatives.

Institutional partners leverage this capital to maintain portfolio fluidity, ensuring that equity isn’t unnecessarily sidelined during lengthy stabilization periods. This strategic oversight allows for the optimization of risk-adjusted returns by utilizing bridge loan lenders to facilitate the transition between acquisition and long-term capitalization. The reliance on these lenders is particularly evident in high-stakes metropolitan markets where the window for property acquisition often closes within 15 business days, a timeframe that traditional balance sheet lenders simply cannot accommodate. Sophisticated market participants are increasingly turning to real estate bridge loans as a primary instrument for transitional capital optimization, ensuring that time-sensitive acquisitions aren’t lost to more nimble competitors who possess immediate liquidity.

When to Engage a Bridge Lender

Investment committees typically engage bridge loan lenders when acquisition timelines are compressed into 10 to 14 days, allowing them to bypass the 60-day requirements of conventional commercial mortgage-backed securities (CMBS) conduits. This tactical deployment of capital is most effective during the critical gap between construction completion and the procurement of permanent financing, often referred to as the ‘take-out’ phase. In 2026, approximately 38% of all opportunistic property repositioning projects utilized bridge financing to fund immediate value-add improvements. These include:

- Time-sensitive acquisitions: Securing off-market assets before competing institutional bids materialize.

- Lease-up stabilization: Providing the 12 to 24 months of runway needed to reach 90% occupancy.

- Adaptive reuse: Funding the conversion of legacy office space into modern residential units.

Understanding the Asset-Backed Underwriting Model

The underwriting philosophy of private bridge capital focuses primarily on the intrinsic value of the real estate rather than the borrower’s personal liquidity or historical credit score. This approach facilitates a streamlined approval process, as the collateral serves as the primary security for the debt. Loan-to-Value (LTV) ratios in 2026 remain disciplined, typically ranging from 65% for speculative assets to 75% for core-plus properties. These ratios provide a robust equity cushion that protects the lender’s principal while allowing the borrower to maximize their capital allocation strategies. Asset-backed loans represent a financing model prioritized by collateral value over borrower liquidity. This emphasis on the asset’s future potential rather than its current cash flow allows for the creative financing of properties that are currently underperforming but possess significant upside potential through active management.

Key Criteria for Evaluating Institutional Bridge Lenders

Selecting the right partner among bridge loan lenders requires a rigorous assessment of historical resilience. Investors should prioritize firms with at least a decade of operational experience; specifically those who successfully navigated the volatility of the 2022 to 2024 interest rate cycles. A lender’s tenure serves as a vital proxy for their ability to manage risk across varying market conditions. Transparency remains a cornerstone of institutional quality. Precise fee structures, typically involving 1.5% to 2.5% in origination points, must be disclosed upfront to ensure the alignment of interests. Hidden exit fees or administrative surcharges often signal a transactional rather than a partnership-oriented mindset.

Speed serves as a primary catalyst for bridge financing. While traditional banks often require 60 to 90 days to close, institutional private lenders should demonstrate the capacity to fund within 14 business days. This agility shouldn’t compromise the depth of due diligence. Sophisticated deals, such as adaptive reuse projects or distressed asset acquisitions, demand a departure from rigid, box-checking criteria. Lenders who offer bespoke amortization schedules or interest-only periods during the stabilization phase provide the strategic oversight necessary for complex capital stacks.

Capital Reliability and Funding Capacity

Direct access to balance sheet capital distinguishes elite bridge loan lenders from intermediary-dependent entities. Relying on broker-only platforms introduces significant execution risk; these firms often lack the autonomy to guarantee funding if their third-party sources retreat. Verification of a lender’s discretionary fund size is vital. A firm managing a $500 million private credit fund offers a level of certainty that smaller syndicators can’t match. This capacity ensures that multi-million dollar transactions, such as a $25 million multi-family bridge facility, remain insulated from external liquidity fluctuations.

The Sophistication of the Underwriting Team

Underwriting is more than a mathematical exercise; it’s an exercise in real estate stewardship. A team’s ability to analyze a property’s net operating income growth potential through a granular lens is non-negotiable. Expertise in specific asset classes, such as the 18% growth observed in industrial logistics hubs in late 2025, allows a lender to act as a strategic advisor. This partnership model ensures that the allocation of private capital is grounded in fundamental value creation rather than speculative trends. Sophisticated underwriting teams identify risks that others overlook, ensuring the long-term preservation of wealth for all stakeholders involved.

Private Bridge Lenders vs. Traditional Banks: A Risk-Adjusted Analysis

Traditional banking institutions operate under a regulatory framework that prioritizes historical compliance over current market opportunity. This bureaucratic inertia often results in documentation cycles extending 60 to 90 days beyond the initial application; a timeline that frequently proves fatal in high-velocity real estate markets. Private bridge loan lenders distinguish themselves by deriving risk-mitigation strategies from deep-seated asset expertise rather than exhaustive red tape. While a bank focuses on a sponsor’s tax returns from three years ago, a private lender analyzes the collateral’s terminal value and the immediate viability of the business plan.

The total cost of capital must be weighed against the potential return on investment for the specific deal. A bank’s 6% interest rate is irrelevant if the 90-day approval window causes an investor to lose a property with a 25% projected internal rate of return. Private capital carries a higher nominal cost, yet it facilitates the capture of equity that would otherwise remain inaccessible. Sophisticated investors treat the interest spread as a necessary acquisition cost, ensuring that the speed of execution preserves the deal’s integrity. Understanding capital funding for real estate provides essential context for optimizing your capital stack through sophisticated private capital strategies.

- Asset-Centric Underwriting: Focus remains on the property’s stabilized value.

- Regulatory Agility: Private firms aren’t bound by the same Basel III capital requirements as commercial banks.

- Precision in Risk Assessment: Decisions are made by committees of principals, not automated credit scoring models.

Speed as a Competitive Advantage

Execution speed is often the primary determinant of success in distressed or off-market acquisitions. A 10-day funding cycle allows an investor to bypass the traditional bidding war, providing the seller with the certainty of a cash-like closing. This psychological advantage shouldn’t be underestimated; sellers in 2026 frequently accept a lower purchase price in exchange for a guaranteed, rapid exit. Bridge financing serves as a liquidity bridge that traditional banks are structurally incapable of providing because their internal audit protocols and capital reserve mandates require a deliberate, slow-moving pace.

Flexibility in Deal Structuring

Institutional private capital offers a level of customization that retail banks cannot match. This includes the ability to negotiate interest-only periods that align perfectly with a project’s renovation or stabilization timeline. Investors can often secure exit strategies that avoid the punitive prepayment penalties common in 10-year bank notes. There’s a natural synergy between this short-term bridge capital and the eventual transition into long-term rental property loans. By utilizing bridge loan lenders for the initial phase, sponsors can optimize their capital stack before seeking institutional permanent financing once the asset is seasoned and cash-flowing.

Structuring Your Bridge Loan for Optimal Portfolio Growth

Precision in capital structure is paramount for the institutional investor. While nominal interest rates often capture the focus of less experienced sponsors, sophisticated parties scrutinize the effective cost of capital. This calculation includes origination points, which generally range from 1% to 3%, and exit fees that typically hover around 50 to 100 basis points. When engaging with bridge loan lenders, you must evaluate how these costs impact the net internal rate of return (IRR) over a compressed 12 to 36-month hold period. A comprehensive understanding of real estate bridge loans as instruments for transitional capital optimization is essential for structuring facilities that align with your portfolio’s specific stabilization timeline and exit requirements.

Alignment between loan maturity and asset stabilization is a non-negotiable requirement for disciplined wealth preservation. If a value-add program requires 18 months to achieve 90% occupancy, a 24-month loan term provides a necessary six-month buffer. Managing the Debt Service Coverage Ratio (DSCR) during this interim period often requires an interest reserve. This reserve, frequently sized to cover 12 months of debt service, ensures the project remains solvent while net operating income (NOI) is optimized. Successful sponsors prioritize the following structural elements:

- Interest Rate Floors: Establishing a ceiling on floating-rate debt to protect against 2026 market volatility.

- Prepayment Flexibility: Negotiating minimal lock-out periods to allow for early refinancing once milestones are met.

- Extension Options: Securing one or two 6-month extensions based on specific performance hurdles.

The Exit Strategy: From Bridge to Permanent Debt

A viable “Take-Out” strategy serves as the foundation of any bridge facility. Lenders in 2026 increasingly demand a clear path to institutional refinancing or a sale. This transition often involves moving from short-term private capital into new construction loans or permanent agency debt. Securing this exit requires the asset to meet a 1.25x DSCR and a 65% to 75% Loan-to-Value (LTV) ratio. Property appreciation, driven by a targeted 15% increase in effective gross income, remains the primary catalyst for a successful refinance.

Risk Mitigation for the Sophisticated Borrower

Prudent risk management involves more than just market timing. It requires a 15% contingency reserve for all capital expenditures to insulate the portfolio from inflationary pressures. For large-scale operators, cross-collateralization can unlock higher leverage by pooling equity across multiple assets, though it requires meticulous strategic oversight. Bridge loan lenders value sponsors who conduct rigorous due diligence on sub-market absorption rates, ensuring the property’s position is defensible against 2026 supply projections. Understanding the strategic role of a bridge lender in real estate capital optimization is essential for maximizing portfolio performance. To ensure your next acquisition is supported by a robust financial framework, optimize your capital stack with JGL Capital’s bespoke advisory services.

JGL Capital: Bespoke Bridge Financing for Sophisticated Investors

JGL Capital functions as a disciplined steward of capital, leveraging a legacy of over 30 years in strategic capital allocation to serve the needs of institutional partners. We understand that the 2026 real estate environment demands more than just liquidity; it requires a partner with the analytical rigor to identify value where traditional institutions see only risk. Our firm distinguishes itself from other bridge loan lenders by prioritizing transparency and the meticulous preservation of wealth through every phase of the investment lifecycle. This serious approach to wealth creation ensures that our interests remain perfectly aligned with those of our high-net-worth clients.

- Institutional Integrity: We operate with an unwavering commitment to clarity, ensuring that every strategic objective is articulated without the ambiguity often found in retail lending.

- Operational Precision: Our streamlined internal protocols are engineered for the pace of modern acquisitions, allowing for a 48-hour preliminary assessment of complex deal structures.

- Asset-Centric Solutions: We provide capital where traditional hurdles exist, focusing on the underlying collateral’s intrinsic value rather than rigid, outdated credit metrics.

The JGL Capital Advantage

Our philosophy centers on the belief that every high-stakes project deserves a unique financial architecture. We don’t offer off-the-shelf products; instead, we craft bespoke loan structures that align with the specific cash flow requirements and exit strategies of our clients. This tailored approach grants our partners access to a sophisticated spectrum of capital solutions, including specialized hard money lenders. By focusing on long-term value creation, we ensure that each allocation serves as a catalyst for portfolio optimization. It’s a method that values the historical performance of the asset as much as its future potential.

Securing Your Next High-Value Asset

The underwriting team at JGL Capital employs a rigorous methodology that places deal viability at the forefront of the decision-making process. We’ve moved away from the standardized reliance on credit scores, recognizing that sophisticated investors often possess complex financial profiles that require nuanced interpretation. Our transition from initial inquiry to a funded deal is characterized by a steady, logical flow of information, maintaining the discretion our high-net-worth clients expect. This deliberate pace ensures that every risk is quantified and every opportunity is maximized. If you’re prepared to execute on a strategic acquisition, Consult with our strategic advisors to secure your bridge capital and experience a partnership defined by stability and expertise.

Securing Your Position in the 2026 Real Estate Capital Landscape

Navigating the complexities of the 2026 real estate market requires a disciplined approach to capital allocation that prioritizes agility and risk-adjusted returns. Sophisticated investors recognize that the ongoing shift away from traditional banking institutions toward private bridge loan lenders provides the critical flexibility needed to execute high-stakes acquisitions without the constraints of conventional credit metrics. By focusing on asset-backed loans and lending structures, you can bypass credit-score dependencies and secure financing based on the intrinsic value of your underlying collateral. This strategic oversight ensures that your portfolio remains resilient against market volatility while capitalizing on immediate opportunities.

JGL Capital brings over 30 years of industry-leading experience to every transaction, ensuring that each bespoke solution aligns with your long-term objectives. Our national reach provides institutional-grade service across diverse markets, facilitating growth through a rigorous, analytical framework. We’ve built our reputation as a discreet steward of capital, valuing integrity and the creation of lasting legacies above all else. Success in this evolving environment depends on the precision of your strategic partnerships. For sophisticated investors seeking to optimize their portfolio performance through strategic capital allocation, understanding real estate investing strategies and insights for 2026 provides essential context for navigating market complexities. Complementing your financing strategy by engaging with real estate investment clubs can further expand your access to institutional-grade deal flow and private capital networks that support long-term portfolio growth. Partner with JGL Capital for bespoke bridge financing solutions. Your commitment to disciplined wealth preservation will serve as the foundation for your continued expansion in the years ahead.

Frequently Asked Questions

What are the typical interest rates for bridge loans from private lenders in 2026?

In 2026, bridge loan lenders typically offer interest rates ranging from 8.25% to 11.75% for stabilized commercial assets. These yields align with the risk-adjusted returns sought by institutional funds managing private capital. While specific terms vary, the weighted average cost of capital usually sits at 9.5%. Borrowers’ specific rates depend on the asset’s location and the sponsor’s track record in managing similar portfolios.

How long does it take for a bridge loan lender to fund a commercial deal?

Closing a commercial bridge deal typically requires 14 to 28 days from the initial term sheet acceptance. This window allows for the completion of environmental assessments and the verification of rent rolls. While some private firms claim faster speeds, the 21-day mark represents the industry standard for thorough due diligence. It’s essential to have all financial disclosures ready to avoid delays in the funding sequence.

What are the standard credit score requirements for an asset-backed bridge loan?

Asset-backed bridge loans generally necessitate a minimum FICO score of 660 to access the most favorable institutional terms. Although the collateral’s intrinsic value serves as the primary security, the sponsor’s credit profile acts as a critical indicator of their historical financial discipline. Sponsors with scores below 630 may still secure funding, but they’ll likely encounter higher origination fees or requirements for additional interest reserves to offset the perceived risk.

Can a bridge loan be used for new construction projects?

Bridge financing effectively supports new construction by providing the liquidity needed for the vertical development phase once the site is fully entitled. Lenders typically provide up to 75% of the total construction costs, provided the project’s feasibility study confirms a strong market demand. This strategic use of private capital allows developers to maintain momentum when traditional banking institutions don’t have the risk appetite for ground-up projects.

What is the difference between a bridge loan and a hard money loan?

The distinction between these products lies in the institutional underwriting and the intended exit strategy of the borrower. Bridge financing serves as a sophisticated tool for transitioning an asset toward permanent debt or a liquidation event. Conversely, hard money loans are typically more expensive, shorter-term instruments provided by private individuals who focus almost exclusively on the property’s liquidation value rather than the sponsor’s strategic plan.

Are there prepayment penalties associated with bridge financing?

Prepayment penalties in this sector often take the form of a six-month interest minimum or a 1% exit fee. These structures protect the lender’s projected yield when a borrower refinances earlier than expected. You’ll find that most institutional agreements don’t allow for a penalty-free exit during the first 180 days of the loan. This ensures the capital allocation remains profitable for the private debt fund.

How much equity do I need to qualify for a bridge loan?

Bridge loan lenders typically require sponsors to maintain an equity position of 20% to 35% of the total project cost. This skin in the game ensures a strong alignment of interests between the capital provider and the property owner. By limiting the leverage to a maximum of 80% loan-to-cost, the lender mitigates the impact of potential market corrections while allowing the borrower to optimize their internal rate of return.

What happens if I cannot refinance the bridge loan before the term ends?

If a borrower can’t secure a refinance before the maturity date, they typically exercise a pre-negotiated six-month extension for a fee of 1% of the loan balance. Without this extension, the lender may apply a default interest rate, often 5% above the base rate, to the outstanding principal. It’s vital to maintain open communication with the lender, as they’ll often prefer a structured workout over a formal foreclosure process.