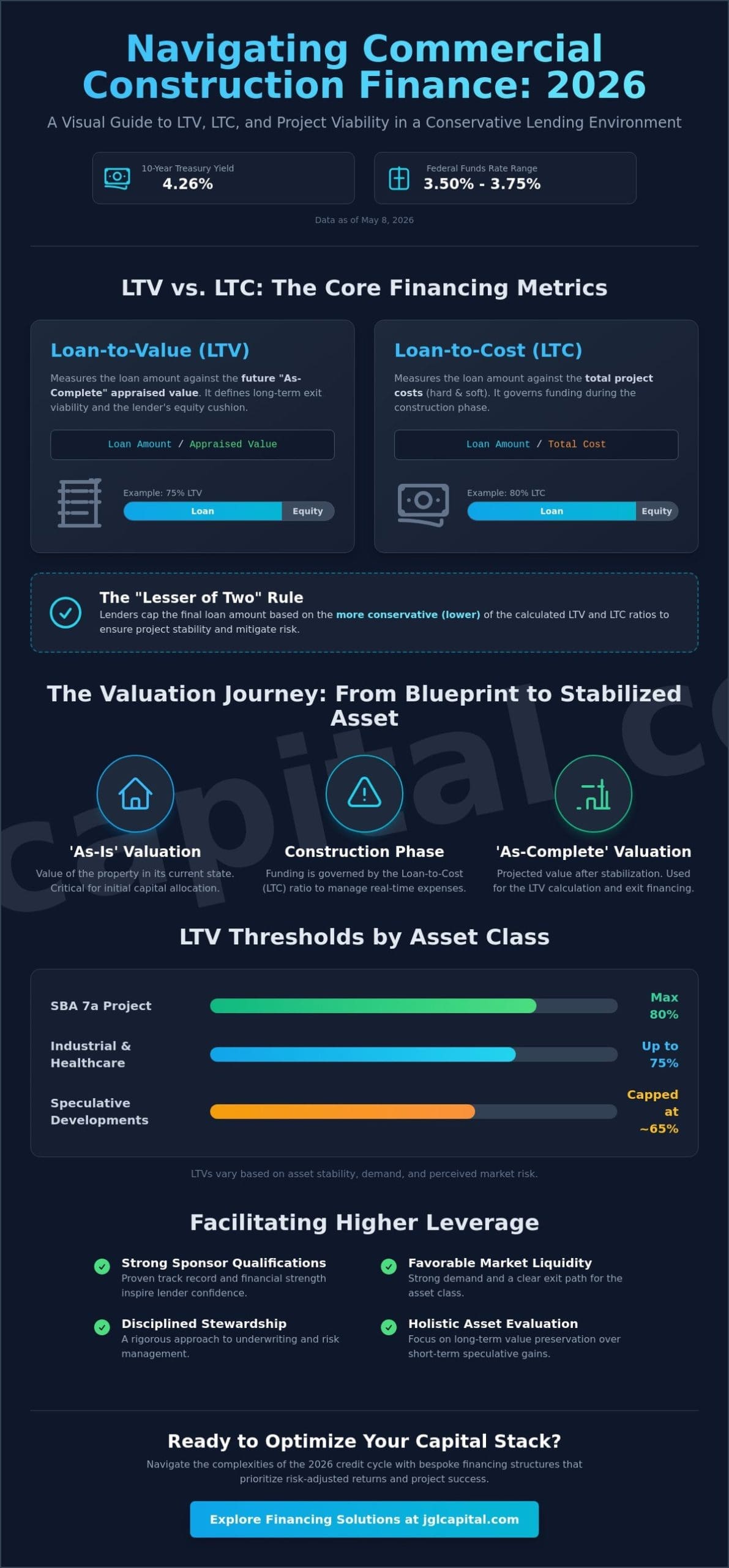

Could the traditional reliance on static leverage ratios be the primary impediment to your firm’s capital efficiency in the 2026 fiscal year? With the 10-year Treasury yield holding at 4.26% as of May 8, 2026, the metrics governing a commercial construction loan LTV have transitioned from simple formulas into complex, risk-adjusted variables. You’ve likely found that balancing equity requirements with project ROI is increasingly difficult as the Federal Reserve maintains the funds rate at a range of 3.50% to 3.75%. Securing the maximum 80% LTV for an SBA 7a project or navigating the 65% cap on speculative developments requires a precise alignment of cost and projected value.

This guide offers a rigorous examination of how LTV dictates project viability and capital allocation in the current credit cycle, providing the analytical depth necessary to navigate conservative lending environments. We’ll analyze the divergence between as-is and as-complete valuations, the disclosure implications of California Senate Bill 362, and the strategic integration of private credit. By understanding these nuances, you can optimize your capital stack to ensure your financing structure remains both resilient and performant through completion.

Key Takeaways

- Analyze how institutional lenders utilize Loan-to-Value ratios to establish necessary equity cushions against 2026 market volatility.

- Distinguish between the tactical application of Loan-to-Cost (LTC) during construction and the strategic role of a commercial construction loan LTV in defining long-term exit viability.

- Evaluate the critical impact of ‘As-Is’ versus ‘As-Complete’ valuation methodologies on initial capital allocation and eventual project stabilization.

- Identify the specific sponsor qualifications and market liquidity factors that facilitate higher leverage within the current conservative lending environment.

- Explore the advantages of bespoke financing structures that prioritize risk-adjusted returns through disciplined stewardship and holistic asset evaluation.

Understanding the Fundamental Mechanics of Loan-to-Value (LTV) Ratios

The Loan-to-Value (LTV) ratio functions as the primary mechanism for quantifying credit risk and determining the structural integrity of a capital stack. In the sophisticated credit environment of May 2026, where the federal funds rate remains at 3.50% to 3.75%, this metric serves as the definitive gatekeeper for institutional capital allocation. A precisely calculated commercial construction loan LTV ensures that a project possesses sufficient residual value to satisfy the senior debt obligation in the event of a market correction. Lenders prioritize this ratio to establish an equity cushion that absorbs the impact of fluctuating cap rates and construction cost overruns, which have stabilized but remain elevated compared to historical averages.

As of early 2026, the 10-year Treasury yield of approximately 4.26% has necessitated a more rigorous approach to underwriting. A commercial construction loan LTV isn’t just a numerical value; it’s a reflection of the lender’s confidence in the stabilized asset value and the sponsor’s ability to execute. Institutional partners use these ratios to filter projects, ensuring that capital is only deployed to developments with a clear path to stabilization and a robust risk-adjusted return profile. This disciplined oversight protects the interests of all stakeholders by preventing over-leverage in a climate of tighter bank lending.

The Mathematical Foundation of LTV

The calculation of LTV involves dividing the total requested loan amount by the appraised “as-complete” value of the property. This ratio significantly influences the project’s weighted average cost of capital (WACC). As risk-adjusted returns become harder to secure, an increase in LTV typically results in higher interest rates, often pushing financing costs into the 9% to 12% range for more flexible structures. The Loan-to-Value ratio serves as the primary structural safeguard for senior lenders by ensuring that a project’s debt remains subordinate to a sufficient equity buffer, thereby insulating the capital position from market fluctuations.

Why LTV Thresholds Vary Across Asset Classes

Lender appetite for leverage is rarely uniform across the commercial landscape. In 2026, industrial developments and healthcare facilities often command more favorable LTV ratios due to strong demand and projected spending growth of 5% to 7% in regions like Texas, as reported by the Associated General Contractors of America. Conversely, speculative retail construction often faces more stringent constraints, with lenders capping leverage to mitigate the risk of prolonged lease-up periods. This variance is a direct result of how property types influence the lender’s tolerance for risk. While a pre-leased industrial warehouse might secure an LTV toward the higher end of the 65% to 75% range, a speculative project’s exposure is frequently limited to ensure project stability. This disciplined approach to capital allocation ensures that every project is underwritten with a focus on long-term value preservation rather than short-term speculative gains.

The Critical Distinction Between Loan-to-Value (LTV) and Loan-to-Cost (LTC)

In the sophisticated landscape of 2026 financing, understanding the divergence between Loan-to-Cost (LTC) and Loan-to-Value (LTV) is essential for strategic capital allocation. LTC represents the ratio of the loan amount to the total hard and soft costs of the project, including land acquisition, labor, and materials. While the commercial construction loan LTV focuses on the projected stabilized value at completion, LTC measures the developer’s immediate financial commitment. Lenders typically utilize LTC during the vertical construction phase to ensure the sponsor maintains sufficient capital at risk, whereas LTV serves as the definitive metric for the long-term exit or permanent financing strategy.

Institutional lenders strictly adhere to the “Lesser of Two” rule, where the final loan proceeds are capped by whichever metric is more conservative. For instance, if a project qualifies for an 80% LTC but the resulting loan amount exceeds 75% of the appraised as-complete LTV, the lender will likely reduce the funding to align with the lower LTV threshold. This methodology provides a secondary layer of protection for the senior debt position, ensuring that the loan remains well-collateralized even if market conditions shift. For owner-occupied projects, the SBA 504 loan program remains a robust option, often allowing for higher leverage than traditional private credit structures which may target risk-adjusted returns of 15% to 20% in the current environment.

LTC: Measuring the Developer’s ‘Skin in the Game’

The LTC ratio is the primary tool for assessing execution risk during the most volatile stages of development. In 2026, lenders analyze every line item, from the 5% to 7% growth in Texas commercial spending to the stabilizing but elevated costs of materials. A high LTC ratio suggests that the developer has less of their own capital at risk, which can be a point of concern for private money lenders seeking disciplined stewardship. Maintaining a balanced LTC ensures that the project remains viable even if unforeseen cost overruns occur. Those seeking to optimize their capital stack often consult with a strategic financing partner to balance these competing metrics effectively.

LTV vs. LTC: A Comparative Framework

The relationship between these two ratios shifts as a project moves through its lifecycle, particularly when land value appreciation is involved. A project might exhibit a high LTV but a relatively low LTC if the developer acquired the land years prior and it has since seen significant appreciation, allowing the “equity credit” to act as a buffer. This interplay is essential for sponsors who wish to maximize leverage without compromising the project’s long-term stability.

| Project Stage | Primary Metric | Typical 2026 Range | Strategic Focus |

|---|---|---|---|

| Land Acquisition | LTV (As-Is) | 50% – 65% | Collateral Security |

| Vertical Construction | LTC | 65% – 80% | Execution Risk |

| Stabilization/Exit | LTV (As-Complete) | 65% – 75% | Capital Preservation |

Appraising the Future: ‘As-Is’ Versus ‘As-Complete’ Valuation Methodologies

The transition from raw land to a stabilized asset requires a sophisticated understanding of valuation methodologies, as the denominator in the LTV equation is rarely static. While the ‘As-Is’ value establishes the baseline for initial land acquisition financing, the ‘As-Complete’ value projects the fair market value upon the issuance of a certificate of occupancy. In the 2026 credit environment, where market absorption rates are scrutinized against a 10-year Treasury yield of 4.26%, these projections must be grounded in rigorous data. For multi-family or office developments, lenders often introduce an ‘As-Stabilized’ metric, which accounts for the anticipated lease-up period required to reach a sustainable Net Operating Income (NOI). This distinction is vital because a commercial construction loan LTV based on stabilized value provides a more accurate reflection of the asset’s long-term viability than a simple completion value.

Navigating appraisal volatility in a fluctuating interest rate environment requires a disciplined approach to asset evaluation. As the Federal Reserve maintains the funds rate between 3.50% and 3.75% as of May 2026, the capitalization rates used in these appraisals are subject to frequent adjustment. A project’s success often hinges on the sponsor’s ability to demonstrate that the projected ‘As-Complete’ value isn’t merely a speculative target but a conservative reflection of current market demand and comparable sales data.

The Role of the MAI Appraisal in Construction Loans

Institutional lenders mandate the use of Member of the Appraisal Institute (MAI) certifications to ensure that valuations meet the highest standards of analytical rigor. These appraisals typically utilize three distinct methodologies: the Cost Approach, the Sales Comparison Approach, and the Income Capitalization Approach. As detailed in the OCC Commercial Real Estate Lending Handbook, the Income Capitalization Approach remains the dominant factor in determining the commercial construction loan LTV for income-producing assets. This method utilizes current market cap rates to discount projected cash flows, ensuring that the senior debt position remains protected against potential fluctuations in market sentiment or interest rate shifts.

Managing the Gap: When Appraisals Fall Short

It’s not uncommon for a disconnect to emerge between a developer’s projected value and the appraiser’s conservative ‘As-Complete’ figure. When this valuation gap restricts the necessary funding, sponsors must seek alternative capital structures to maintain project momentum. Utilizing bridge loans can provide the necessary transitional capital to cover these shortfalls until the project achieves the milestones required for a permanent refinance. By presenting a compelling case based on specific market absorption data and verified pre-leasing activity, developers can often justify a higher valuation and maximize their leverage without compromising the project’s overall stability.

Determinants of Maximum Leverage and Risk-Adjusted Capital Allocation

The determination of a project’s maximum commercial construction loan LTV is never a solitary calculation; it’s a dynamic result of converging market liquidity and sponsor-specific risk profiles. In 2026, the “Maturity Wall”—a concentration of maturing commercial debt—has tightened the availability of capital as institutions prioritize portfolio rebalancing. This scarcity means that lenders are increasingly selective, often reserving higher leverage for projects that demonstrate exceptional market absorption potential. A project’s Debt Service Coverage Ratio (DSCR) often acts as a hard ceiling on LTV, as the projected cash flow must comfortably support the debt obligations at current interest rates to ensure project stability.

Pre-leasing activity remains a decisive factor in unlocking superior leverage. For industrial or retail developments, a high volume of signed letters of intent (LOIs) or executed leases can push a lender’s tolerance toward the upper bounds of the 70% to 80% range. Without these commitments, a project is viewed through a speculative lens, typically resulting in more conservative caps to mitigate the risk of an extended lease-up period. This disciplined approach ensures that capital is allocated to projects with the highest probability of achieving stabilized value. Execution risk is a primary concern. Sponsors with a proven track record of delivering new construction loans on schedule often find more flexibility in their financing terms.

Macroeconomic Influences on LTV Caps

Federal Reserve policy, which has maintained the funds rate at 3.50% to 3.75% as of early 2026, continues to influence commercial mortgage-backed securities (CMBS) spreads and national lending standards. Regional economic health also plays a significant role, as areas with robust building spending growth, such as the 5% to 7% growth projected in Texas by the AGC, often benefit from more aggressive lending appetite. As interest rates remain elevated, the maximum permissible LTV tends to contract to ensure that the asset’s net operating income can sustain the increased cost of debt service. These macro factors create a shifting baseline for every capital request.

Sponsor Strength and Recourse Obligations

Underwriting standards in 2026 place a premium on the financial resilience and track record of the sponsor. Lenders scrutinize liquidity and net worth to ensure that the borrower can withstand unforeseen cost overruns or market shifts. When structuring commercial real estate loans, the distinction between recourse and non-recourse debt becomes a critical lever for LTV flexibility. While non-recourse options offer significant protection, they often require lower LTV ratios; conversely, a personal guarantee may unlock higher leverage by aligning the sponsor’s interests more closely with the lender’s capital preservation goals. Cross-collateralization of existing assets can also serve as a sophisticated method to improve the LTV on a specific project by providing additional security. To navigate these complex variables and secure optimal terms, it’s advisable to engage a strategic capital partner who understands the nuances of risk-adjusted allocation.

Bespoke Construction Financing Strategies Through JGL Capital

JGL Capital operates as a disciplined steward of capital, transcending the rigid and often prohibitive formulas employed by traditional depository institutions. While conventional banks may impose inflexible caps on a commercial construction loan LTV due to regulatory pressures or internal liquidity constraints, our firm utilizes a methodology rooted in analytical rigor and holistic asset evaluation. With 30 years of institutional experience, we facilitate access to a sophisticated network of private capital, including specialized hard money lenders florida and national institutional funds. This strategic oversight is particularly critical in 2026, as the commercial real estate sector navigates a stabilized but elevated interest rate environment where the Federal Reserve has maintained the funds rate between 3.50% and 3.75% as of May 8, 2026. Our approach ensures that every project is underwritten with a focus on long-term value preservation rather than transient market trends.

Sourcing capital for complex, multi-phase developments requires more than just a list of lenders; it demands an alignment of interests and a deep understanding of risk-adjusted returns. By framing our activities as a form of high-level partnership, we help sponsors navigate the nuances of capital allocation to ensure project viability from inception to stabilization. This commitment to stewardship distinguishes our firm from transactional competitors, as we prioritize the delivery of tailored solutions that respect the gravity of high-stakes financial management.

Navigating the Private Money Landscape

The private credit landscape offers a level of agility that traditional banks cannot replicate. Private money brokers and institutional funds prioritize the underlying asset’s potential and the sponsor’s execution capability over standardized credit scoring models. Our role involves identifying the optimal capital partner whose risk appetite aligns with your specific commercial construction loan LTV requirements, ensuring that capital is deployed efficiently without compromising project stability. We streamline the underwriting process by conducting thorough due diligence that anticipates lender concerns; this reduces the time to close and secures necessary liquidity for sophisticated developments.

Securing Your Project’s Future

Professional representation is a prerequisite for success in high-stakes real estate investing. As market conditions evolve, the ability to articulate a project’s value proposition to sophisticated capital providers becomes a competitive advantage. JGL Capital serves as a collaborative ally, ensuring that every financing structure is bespoke and tailored to the unique objectives of the sponsor. We invite you to initiate a consultation to examine how our intellectual capital can optimize your next development. Contact JGL Capital for a strategic evaluation of your construction financing needs.

Mastering Capital Efficiency in the 2026 Fiscal Cycle

Success in the current credit environment requires a profound understanding of how capital allocation and project viability intersect. The commercial construction loan LTV has evolved from a static metric into a dynamic indicator of risk-adjusted stability. Sophisticated sponsors will be those who master the distinction between cost-based leverage and value-driven exit strategies; they’ll use the precision of MAI appraisals to navigate the 4.26% Treasury yield environment effectively. This analytical approach ensures that every project remains resilient against market shifts and interest rate fluctuations while maintaining the integrity of the senior debt position.

JGL Capital provides the strategic oversight necessary to navigate these complexities through a commitment to stewardship and institutional rigor. With over 30 years of industry expertise and a specialization in complex asset-backed financing, our firm offers the national reach and high-touch guidance required to secure superior terms. We invite you to Secure Institutional-Grade Construction Capital with JGL Capital to ensure your next development is supported by a partner invested in your long-term success. Building a lasting legacy starts with a disciplined approach to capital. We look forward to facilitating your project’s advancement.

Frequently Asked Questions

What is a typical LTV for a commercial construction loan in 2026?

In the 2026 credit cycle, typical leverage is contingent upon the specific financing program and the asset’s risk profile. For instance, the SBA 7a program permits leverage up to 80%, whereas commercial bridge loans are generally capped at 65% to 75% of the as-is value to ensure capital preservation. These thresholds reflect a disciplined approach to capital allocation in an environment where the 10-year Treasury yield sits at 4.26%.

How does the Loan-to-Cost (LTC) ratio differ from LTV in a new build?

LTC measures financing against the aggregate of hard and soft construction costs, with 2026 caps typically ranging between 65% and 80% depending on pre-leasing status. In contrast, the Loan-to-Value ratio assesses debt against the projected stabilized market value of the completed asset. Institutional lenders utilize the more conservative of these two metrics to establish the final loan size, thereby protecting the senior debt position from market volatility.

Can land equity be used to meet LTV requirements for construction?

Land equity is frequently utilized to satisfy the required equity contribution for a commercial construction loan LTV. If a sponsor has held the land through an appreciation cycle, lenders may provide equity credit for the current market value, effectively reducing the cash-in-pocket requirement. This strategy allows developers to leverage existing assets to meet the 20% to 35% equity positions typically required by institutional partners in the current fiscal year.

Do private lenders offer higher LTVs than traditional banks for commercial projects?

Private credit providers often offer more bespoke leverage structures than traditional banks, which are currently constrained by tighter underwriting standards and regulatory oversight. While banks remain conservative, private funds targeting risk-adjusted returns of 15% to 20% can facilitate higher leverage for projects with robust pre-leasing. It’s an essential flexibility for developers navigating a landscape where commercial construction interest rates frequently range from 5.50% to 8.75%.

What factors could cause a lender to lower the maximum LTV during underwriting?

Lenders may reduce maximum leverage thresholds if the project’s Debt Service Coverage Ratio (DSCR) is insufficient to support debt obligations at the current federal funds rate of 3.50% to 3.75%. Other contributing factors include speculative project structures lacking signed letters of intent or regional economic indicators suggesting a cooling in market absorption. These adjustments ensure that the capital stack remains resilient even if the project encounters unforeseen operational challenges during the lease-up phase.

How does the ‘As-Complete’ value affect the final loan amount?

The ‘As-Complete’ value acts as the definitive benchmark for the project’s exit strategy and long-term financing viability, serving as the denominator for the commercial construction loan LTV. A lower projected value directly reduces the total loan proceeds available, as lenders must maintain a disciplined equity cushion. This safeguard protects the investment against potential shifts in capitalization rates or occupancy levels that may occur before the project reaches full stabilization.

Is there a minimum credit score required for high-LTV commercial construction loans?

Institutional underwriting focuses more on a sponsor’s net worth and liquidity than a singular credit score, though a score below 680 typically necessitates additional structural safeguards or recourse obligations. High-leverage projects require a comprehensive demonstration of financial resilience to ensure the sponsor can manage the debt service requirements. Lenders prioritize partners who demonstrate a serious and disciplined approach to wealth preservation, particularly when financing costs remain elevated above pre-pandemic levels.

What happens if the appraisal comes in lower than the expected LTV?

An appraisal that falls short of expectations creates a funding gap that the sponsor must fill with additional equity or mezzanine debt to maintain the required leverage ratios. In such instances, bridge loans often serve as a transitional tool to maintain project momentum until the asset achieves the milestones required for a permanent refinance. It’s a proactive way to manage the capital stack and ensure project completion without compromising the long-term integrity of the development.