What if the most efficient path to portfolio optimization was hidden within the structural shell of a distressed commercial asset? While new development costs continue to escalate, the strategic reallocation of capital into adaptive reuse allows sophisticated investors to create residential density at a fraction of the traditional cost. Securing the appropriate financing a multi-family conversion project requires an institutional partner capable of moving beyond rigid, legacy credit requirements. JGL Capital LLC serves as this essential ally, providing the analytical rigor and asset-based underwriting necessary to navigate the complexities of transitional real estate.

We agree that traditional lending delays and a lack of historical income often create significant capital gaps that stifle project momentum. This guide will empower you to master the complexities of adaptive reuse financing and discover how strategic private capital bridges the gap between underperforming assets and stabilized multi-family revenue. We will outline a clear path from acquisition to permanent agency financing, ensuring your next conversion is positioned for long-term success and wealth preservation through disciplined capital allocation.

Key Takeaways

- Recognize the economic imperative of repurposing underperforming commercial assets into high-density residential developments as a strategic response to evolving urban demands.

- Analyze the selection of sophisticated financial instruments, such as bridge loans, to provide the necessary liquidity for the initial phases of financing a multi-family conversion project.

- Adopt an asset-centric underwriting philosophy that emphasizes the After-Repair Value (ARV) and the intrinsic potential of the real estate over conventional credit metrics.

- Define a structured capital lifecycle that facilitates a seamless transition from acquisition and heavy renovation to long-term stabilization and permanent agency financing.

- Leverage the institutional expertise of a seasoned partner to secure bespoke capital allocations that reflect a disciplined approach to risk-adjusted returns.

The Strategic Landscape of Adaptive Reuse and Multi-Family Conversions

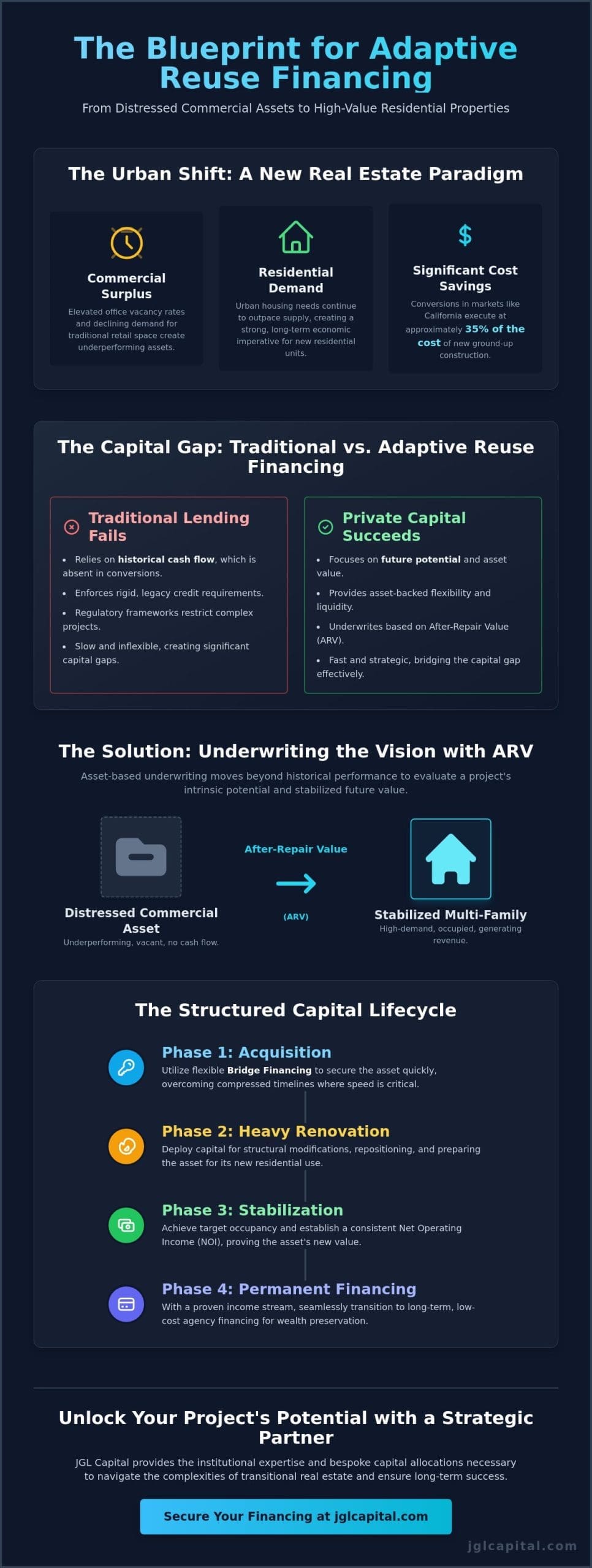

The current paradigm of urban development is undergoing a fundamental transformation, driven by a pronounced divergence between commercial utility and residential necessity. Institutional investors increasingly view the multi-family conversion as a sophisticated strategic response to the structural decline in demand for traditional office and retail environments. This shift isn’t merely a tactical adjustment; it represents a disciplined approach to portfolio optimization that prioritizes long-term value creation over the retention of underperforming assets. The Strategic Landscape of Adaptive Reuse serves as the foundation for this evolution, allowing for the preservation of architectural integrity while meeting the urgent requirements of modern housing density. Within this context, financing a multi-family conversion project emerges as a critical competency for the modern steward of capital who seeks to navigate the complexities of transitional real estate.

The Macroeconomic Shift Toward Residential Density

As of May 2026, the real estate market is characterized by a significant surplus of commercial square footage, particularly in urban cores where office vacancy rates remain elevated. Conversely, the demand for residential units continues to outpace supply, creating an economic imperative for the repurposing of existing structures. Adaptive reuse is the strategic repurposing of a building for a use other than that for which it was originally designed. Recent legislative advancements, such as the “Office-to-Anything” program in Washington, D.C., which offers property tax abatements for up to 15 years, underscore the public sector’s commitment to this transition. In California, these projects are executing at approximately 35% of the cost of new construction, demonstrating a clear financial advantage for those who can efficiently manage the capital lifecycle. These zoning evolutions directly impact project feasibility, often unlocking latent value that traditional models fail to capture.

Why Traditional Financing Fails Conversion Projects

Conventional lending institutions typically rely on historical cash flow and stabilized performance metrics, which are inherently absent during the initial stages of a conversion. This reliance creates a significant “Capital Gap,” as banks retreat from assets that lack a proven income stream. Regulatory frameworks often restrict commercial banks from engaging with high-complexity projects that involve heavy structural modifications or significant zoning hurdles. The necessity of asset-backed flexibility becomes paramount during these early phases. Private capital acts as the essential catalyst, providing the strategic oversight and liquidity required to navigate the transition from an underperforming commercial asset to a stabilized multi-family revenue generator. By focusing on the After-Repair Value (ARV) rather than historical data, seasoned partners can facilitate a more efficient approach to financing a multi-family conversion project, ensuring that the vision for the asset isn’t compromised by rigid, outdated credit requirements.

Financial Instruments for Multi-Family Conversion Projects

The selection of an optimal capital structure for financing a multi-family conversion project necessitates a granular understanding of the project’s risk-adjusted trajectory. As an asset transitions from its legacy commercial use toward a stabilized residential profile, the risk profile shifts, requiring a sophisticated blend of debt instruments that align with specific development milestones. JGL Capital LLC ensures that institutional investors evaluate these instruments not merely as sources of liquidity, but as strategic tools that dictate the pace of execution and the ultimate efficiency of the capital stack. This disciplined approach to capital allocation ensures that the project remains viable through the volatile phases of heavy rehabilitation and market repositioning.

Bridge Financing: The Engine of Acquisition

Institutional investors often encounter compressed acquisition timelines where the capacity to deploy capital rapidly determines the viability of a transaction. Bridge loans serve as the primary engine of acquisition, providing the necessary liquidity to secure high-potential assets before traditional underwriting can even commence. These facilities are frequently structured with interest-only periods, which allow developers to preserve essential cash flow during the initial demolition and structural assessment phases. The strategic advantage of speed is particularly evident in the 2026 national real estate market, where the ability to close within a few days allows sophisticated partners to capitalize on distressed commercial opportunities. Many of these instruments offer non-recourse options, which align with a firm’s broader risk management objectives by isolating the liability to the specific asset under development.

Construction and Rehabilitation Loans

For conversion projects that involve significant structural overhauls or the addition of new residential wings, new construction loans provide the comprehensive funding required for heavy development. These loans are meticulously structured to manage draw schedules and interest reserves, ensuring that capital is distributed in alignment with verified construction progress. In the current lending environment, the distinction between Loan-to-Cost (LTC) and Loan-to-Value (LTV) is a critical consideration for portfolio optimization. While FHA 221(d)(4) programs may offer up to 87% LTV for market-rate properties as of May 2026, private asset-based underwriting often prioritizes LTC to more accurately reflect the intensive capital requirements of the conversion phase. This precision in structuring prevents the under-capitalization that frequently plagues complex adaptive reuse initiatives.

Larger developments often require a multi-tiered capital stack to achieve the desired leverage. Mezzanine financing and preferred equity fill the gap between senior debt and sponsor equity, allowing developers to maximize their return on invested capital while maintaining a disciplined equity position. This layered approach facilitates the pursuit of large-scale urban revitalization projects that might otherwise be constrained by traditional lending limits. Partnering with a disciplined steward of capital can refine these selections into a cohesive strategy; you may find that bespoke debt structures from JGL Capital LLC are the most effective way to enhance the value of your next acquisition.

Underwriting the Vision: Asset-Based Evaluation vs. Traditional Credit

Traditional financial institutions often falter when evaluating transitional assets because their underwriting models are anchored in historical stability rather than prospective value. For an institutional investor financing a multi-family conversion project, this reliance on past performance creates a structural barrier that ignores the inherent potential of the real estate. Private capital providers, acting as disciplined stewards, shift the focus toward the intrinsic value of the asset. This perspective allows for the funding of projects where current cash flow is negligible, but the After-Repair Value (ARV) suggests substantial long-term equity growth. By prioritizing the terminal value of the property, seasoned lenders provide the strategic oversight necessary to unlock wealth in underperforming commercial sectors.

Analyzing the project’s pro forma requires a rigorous assessment of future stabilized income that transcends simple projections. Lenders examine regional market trends, such as the 0.12% increase in average rents observed in the Midwest during late 2025, to validate projected revenue streams. While the West experienced a slight decline of 0.01% in the same period, a well-structured pro forma accounts for these micro-market fluctuations through analytical rigor. A developer’s track record in executing similar adaptive reuse projects often carries more weight than a personal balance sheet; operational expertise is the primary mitigator of execution risk in high-stakes conversions. This focus on experience ensures that capital is allocated to those with the proven capacity to deliver stabilized multi-family revenue.

The Preeminence of the Asset

Underwriting for conversion projects is fundamentally an exercise in valuing the “as-completed” state of the property rather than its current state of obsolescence. Asset-based lending prioritizes the collateral’s projected market value and income-generating potential over the borrower’s historical personal income or credit score. This approach utilizes third-party appraisals and exhaustive feasibility studies to ensure that the capital allocation is grounded in empirical data. By focusing on the asset’s terminal value, lenders can offer the leverage necessary to bridge the gap between a vacant commercial shell and a stabilized residential community. It’s a methodology that recognizes the property itself as the primary driver of the investment’s success.

Managing Risk-Adjusted Returns

Disciplined capital allocation is essential to protect the interests of all stakeholders involved in the development process. Private lenders function as strategic partners, aligning their interests with the developer to ensure the project’s long-term viability. This alignment is reflected in the use of conservative Loan-to-Value (LTV) ratios and the requirement for robust contingency funds to absorb unforeseen construction hurdles. As of January 2026, benchmark indices like the 10-year Treasury at 4.27% and the 30-day SOFR at 3.69% inform the pricing of these risk-adjusted returns. Maintaining a minimum Debt Service Coverage Ratio (DSCR), such as the 1.15x required for market-rate properties under HUD guidelines, ensures that the project remains resilient against market volatility and operational stress.

Navigating the Capital Lifecycle: From Conversion to Stabilization

The execution of a multi-family conversion isn’t a singular event but a sequenced deployment of capital that mirrors the physical and operational maturation of the asset. For the institutional investor, financing a multi-family conversion project requires a comprehensive understanding of how initial bridge liquidity transitions into permanent, low-cost debt. This lifecycle begins with the acquisition phase, where speed is the primary objective to secure the property and initiate demolition. As the project moves into the construction phase, the focus shifts to managing draw schedules and meeting specific development milestones that satisfy the rigorous oversight of the capital provider. Each phase of this journey is designed to de-risk the asset, moving it closer to the institutional quality required by permanent lenders.

The successful navigation of this lifecycle culminates in the exit strategy, where the transitional debt is retired in favor of long-term commercial real estate loans. This transition is only possible once the property has reached a state of operational maturity. Effective capital allocation ensures that the developer has sufficient interest reserves and contingency funds to reach this point without liquidity stress. By viewing the financing as a continuous lifecycle rather than a series of isolated transactions, sponsors can better align their development timelines with market conditions and permanent lending requirements. To ensure your project is positioned for a seamless transition to permanent debt, you should consult with a strategic capital ally like JGL Capital LLC who understands the complexities of the full development timeline.

The Critical Stabilization Phase

Stabilization represents the most sensitive juncture in the capital lifecycle, as it is the period where the property must demonstrate its capacity to generate consistent net operating income (NOI). In the 2026 market, stabilization is typically defined by reaching an occupancy rate of at least 90% for a period of 90 consecutive days. During this phase, the asset undergoes intense institutional scrutiny to verify that the Debt Service Coverage Ratio (DSCR) meets the 1.15x minimum required for market-rate agency financing. This metric serves as the primary determinant for the success of the exit strategy, as it confirms the property’s ability to support a long-term mortgage without additional sponsor support. Preparing the project for this level of scrutiny requires meticulous record-keeping and a disciplined approach to property management from the first day of lease-up.

Exit Strategies and Permanent Financing

Once stabilization is achieved, the sponsor must evaluate the most advantageous exit among Agency programs, Life Companies, or CMBS providers. Agency debt through Fannie Mae or Freddie Mac often provides the most competitive leverage, particularly for projects that meet specific affordability or energy-efficiency criteria. As of May 2026, fixed-rate terms for 5-year to 10-year periods are ranging between 5.38% and 5.88%, offering a significant reduction in debt service costs compared to transitional bridge rates. The decision to pivot from transitional debt to permanent capital must be timed with precision, often occurring as soon as the 1.15x DSCR threshold is verified. Securing long-term fixed-rate debt through a partner like JGL Capital LLC provides the stability necessary to preserve the legacy of the asset while maximizing the risk-adjusted returns for the ownership group.

Strategic Partnership with JGL Capital for Multi-Family Success

JGL Capital stands as a seasoned steward of capital, leveraging over 30 years of intellectual capital to navigate the intricate requirements of adaptive reuse. Our approach to financing a multi-family conversion project is rooted in analytical rigor, ensuring that every allocation is designed to optimize risk-adjusted returns for our partners. We recognize that national developers require a partner who can reduce institutional friction, providing the stability and speed necessary to execute high-stakes conversions in a volatile market. Our bespoke financing solutions are meticulously tailored to the unique structural and regulatory requirements of adaptive reuse, acknowledging that no two conversion projects share the same risk profile. By prioritizing the long-term success of the asset, we align our interests with yours, moving beyond simple service provision to establish a collaborative strategic alliance.

A Disciplined Approach to Private Capital

Our expertise extends across the national landscape, with a specific focus on the nuanced requirements of regional markets where traditional lending often falls short. As prominent hard money lenders Florida and a leader in national private credit, we provide the rapid execution required to secure assets in competitive urban environments. We pride ourselves on being a quiet expert, relying on a proven track record of successful capital allocation rather than aggressive self-promotion. This disciplined approach ensures that our investment philosophies remain grounded in timeless financial principles, rejecting speculative trends in favor of sustainable value creation. Our commitment to stewardship means we remain deeply invested in the successful completion and stabilization of your project, providing the strategic oversight necessary to transition from acquisition to permanent agency debt. We don’t just provide capital; we provide a foundation for lasting legacies.

Initiating Your Conversion Project

Initiating a partnership with JGL Capital begins with a methodical assessment of the project’s intrinsic value and the developer’s operational history. For a sophisticated asset-based loan application, we require comprehensive documentation, including detailed pro formas, third-party appraisals, and a verified track record of similar adaptive reuse successes. During our underwriting and due diligence process, we conduct a granular analysis of the project’s capital lifecycle, ensuring that interest reserves and contingency funds are appropriately structured to absorb potential market fluctuations. This deliberate pace reflects our dedication to precision and our rejection of the commodity approach to lending. We invite you to engage JGL Capital for your next multi-family conversion project to experience a level of bespoke financial management that reflects the gravity of your investment goals. Our team is prepared to conduct a thorough review of your portfolio objectives to ensure that our capital solutions align perfectly with your vision for urban revitalization and revenue stabilization.

Optimizing Capital for the Evolution of Urban Density

The transition from commercial obsolescence to high-density residential housing represents a sophisticated evolution in capital allocation that demands both analytical rigor and strategic patience. By prioritizing the intrinsic potential of the real estate asset over historical performance, you can unlock significant value in underperforming urban sectors. We’ve explored how a disciplined approach to the capital lifecycle ensures that your project remains resilient through the complexities of demolition and heavy rehabilitation. Successfully financing a multi-family conversion project ultimately depends on the alignment of interests between the sponsor and a capital partner who values the long-term integrity of the asset.

JGL Capital provides the stability and expertise required to navigate these high-stakes transitions, leveraging over 30 years of experience in strategic capital management. Our asset-based underwriting focuses on the property’s potential, offering streamlined national funding for sophisticated investors who require rapid, reliable execution. We invite you to Secure Strategic Capital for Your Multi-Family Conversion with JGL Capital and establish a partnership grounded in stewardship and precision. It’s time to transform underperforming square footage into a stabilized legacy of multi-family revenue.

Frequently Asked Questions

What is the typical interest rate for financing a multi-family conversion project in 2026?

As of May 7, 2026, interest rates for HUD 221(d)(4) loans for substantial rehabilitation typically range from 5.66% to 6.16%. Financing a multi-family conversion project through private bridge capital generally carries a higher interest rate to account for the transitional nature of the risk. These rates are influenced by benchmark indices such as the 10-year Treasury, which stood at 4.27% in early 2026, and the SOFR 30-day rate of 3.69%.

Can I use a bridge loan for the acquisition of an office building intended for residential conversion?

Bridge loans are specifically designed as transitional tools for the acquisition of office buildings intended for residential repurposing. These facilities allow institutional investors to secure high-potential assets rapidly, often closing within a few days to capitalize on market opportunities. This initial liquidity facilitates the commencement of demolition and structural assessments while the long-term capital stack is being finalized and stabilized revenue is projected.

What is the maximum Loan-to-Value (LTV) offered for multi-family conversion projects?

Maximum leverage for adaptive reuse projects is determined by the specific financing program and the project’s affordability profile. As of May 2026, HUD programs provide up to 87% LTV for market-rate properties and 90% for projects meeting specific affordability requirements, such as Section 8 or LIHTC projects. Private asset-based lenders often focus on Loan-to-Cost (LTC) metrics, providing the necessary flexibility for projects that require intensive capital during the early renovation phases.

How long does the underwriting process take for a private money conversion loan?

The underwriting process for a private money conversion loan is streamlined to reduce institutional friction and can often result in funding within a few business days. Initial term sheets are frequently issued within 24 hours of receiving a sophisticated documentation package. This accelerated timeline is a hallmark of private capital; it allows developers to meet compressed closing schedules that traditional banks cannot accommodate due to rigid regulatory requirements.

Is a personal guarantee required for adaptive reuse financing?

Non-recourse financing is a common feature for institutional-grade projects and experienced developers who demonstrate a strong track record of success. Asset-based underwriting focuses on the collateral’s potential and After-Repair Value (ARV) rather than solely on the borrower’s historical income or credit score. This structure aligns the interests of the lender and the sponsor by isolating the financial risk to the specific asset being converted into residential units.

What happens if the conversion project takes longer than the bridge loan term?

When a conversion project exceeds its initial bridge loan term, developers typically utilize pre-negotiated extension options or transition into a secondary bridge facility. Sophisticated capital partners build these contingencies into the initial loan structure to account for the complexities inherent in adaptive reuse. Maintaining transparent communication regarding project milestones is essential for securing the necessary time to reach the stabilization required for permanent agency financing.

Do you provide financing for multi-family conversions nationwide?

Strategic capital for financing a multi-family conversion project is available nationwide, supporting developers in both established urban cores and emerging secondary markets. Our institutional reach allows for the deployment of funds across various jurisdictions, navigating the unique zoning and regulatory environments of different states. This national presence ensures that sophisticated investors have access to reliable capital regardless of where their next adaptive reuse opportunity arises.

What are the primary exit strategies for developers using transitional capital?

The most prevalent exit strategies involve refinancing into long-term permanent debt once the property reaches a stabilized Debt Service Coverage Ratio (DSCR) of at least 1.15x. Developers often target Agency financing, such as Fannie Mae or Freddie Mac, which offered 5-year fixed rates between 5.58% and 5.88% in January 2026. Other viable exits include Life Insurance Company loans or the sale of the stabilized asset to a long-term institutional holder seeking consistent yields.