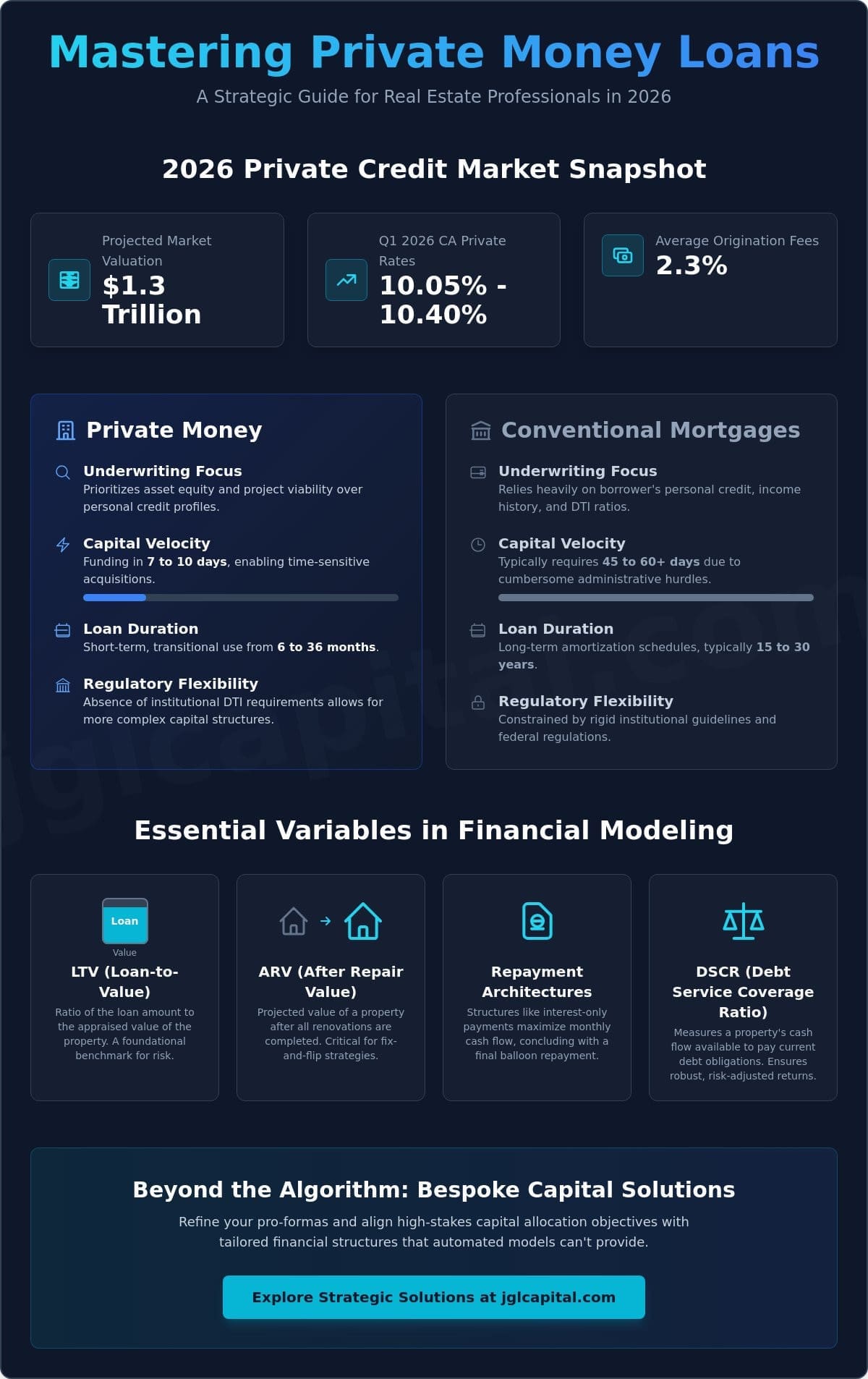

While the U.S. private credit market has ascended to a projected $1.3 trillion valuation in 2026, the delta between a successful exit and a capital loss often resides in the granular details of a pro forma. For the disciplined real estate professional, a robust private money loan calculator serves as a vital instrument of strategic oversight rather than a simple arithmetic tool. It’s insufficient to merely estimate carrying costs when the first quarter of 2026 saw California private money rates fluctuate between 10.05% and 10.40% with average origination fees of 2.3%.

You understand that ambiguity regarding total capital costs, especially the nuances of interest-only periods and final balloon repayments, can compromise the integrity of your investment thesis. This article provides a comprehensive framework to master the financial modeling of private capital, allowing you to optimize your returns and project feasibility with institutional precision. We’ll analyze how current LTV benchmarks influence interest rates and detail the exact methodology for calculating total loan costs at exit, ensuring your capital allocation remains both defensive and highly productive.

Key Takeaways

- Learn to distinguish asset-backed private capital from traditional credit facilities by prioritizing property viability over personal credit profiles for more agile acquisitions.

- Utilize a private money loan calculator to model critical benchmarks such as Loan-to-Value (LTV) and After Repair Value (ARV) for precise project feasibility.

- Analyze the strategic advantages of interest-only debt structures in maximizing monthly cash flow while preparing for the capital event of a terminal balloon repayment.

- Refine your investment pro-formas by incorporating detailed debt service coverage ratios (DSCR) to ensure robust risk-adjusted returns across your portfolio.

- Understand the limitations of automated modeling and the necessity of bespoke financial structures that align with high-stakes capital allocation objectives.

Distinguishing Private Money from Traditional Credit Facilities

While often misunderstood as a secondary option, private money represents a primary vehicle for asset-backed capital allocation for sophisticated entities. Unlike institutional debt that relies on the borrower’s historical credit performance, private money prioritizes the intrinsic value and projected viability of the underlying real estate asset. This shift in underwriting focus allows investors to bypass the cumbersome administrative hurdles of traditional banking. In this context, a Hard money loan overview clarifies that these instruments are secured by the property itself, making them ideal for time-sensitive acquisitions where conventional financing would fail to meet closing deadlines. Using a private money loan calculator during the due diligence phase ensures that the total cost of capital is aligned with the project’s anticipated profit margins before any commitments are made.

The Role of Asset-Backed Lending in 2026

In the current 2026 market, rapid execution is the hallmark of a disciplined investment strategy. As traditional lenders tighten their credit boxes following the implementation of the FinCEN Residential Real Estate Rule on March 1, 2026, private capital providers offer the agility required to secure distressed assets or opportunistic developments. Utilizing bridge loans allows for the stabilization of properties before they’re transitioned into long-term financing or sold for a profit. Strategic oversight dictates that the cost of capital is a secondary consideration when compared to the opportunity cost of a lost transaction. The ability to fund within 7 to 10 days, rather than the 45 to 60 days required by banks, justifies the premium associated with non-institutional debt.

Private Money vs. Conventional Mortgages

The divergence between private capital and conventional mortgages is most evident in the underwriting process. While a bank may require significant time to evaluate Debt-to-Income (DTI) ratios and personal tax returns, private lenders focus on the equity position and the project’s exit strategy. This distinction is vital when inputting variables into a private money loan calculator, as the tool must account for the shorter, 6 to 36-month terms typical of these facilities. Accurately modeling these variables ensures that the investor maintains a clear view of the risk-adjusted returns throughout the hold period.

- Underwriting Focus: Asset equity and project feasibility vs. personal credit and income history.

- Capital Velocity: Funding in 7 to 10 days vs. 45 to 60 days for traditional retail banking.

- Loan Duration: Short-term transitional use (6 to 36 months) vs. long-term amortization (15 to 30 years).

- Regulatory Flexibility: Absence of institutional DTI requirements allows for more complex capital structures.

Private money is a tactical financial instrument for sophisticated developers, providing the necessary leverage to execute complex, time-sensitive acquisitions that fall outside the rigid parameters of traditional retail banking. Choosing this path allows developers to prioritize project velocity and asset potential over the slow, documentation-heavy processes of institutional finance, ultimately building a more resilient and responsive real estate portfolio.

Essential Variables in Private Money Financial Modeling

Sophisticated investors recognize that a basic interest rate is merely one component of a much larger financial architecture. When utilizing a private money loan calculator, the primary determinants of capital availability are Loan-to-Value (LTV) and Loan-to-Cost (LTC) ratios. These metrics serve as the foundational benchmarks for risk-adjusted capital allocation, dictating the depth of the lender’s security interest in the asset. For those executing specialized strategies such as fix and flip loans florida, the After Repair Value (ARV) becomes the critical variable. It models the future equity position of the asset after capital improvements are completed, providing a projection of project viability that traditional credit models often ignore. This Guide to private lending emphasizes that understanding these nuances is essential for any investor seeking to leverage private debt effectively.

Calculating LTV and ARV Impact

There’s a direct correlation between Loan-to-Value ratios and the risk-adjusted interest rate premiums applied to a facility. In the first quarter of 2026, average LTVs for private money loans hovered around 67%, reflecting a disciplined approach to asset protection. When modeling a project, investors typically utilize a 70% to 75% ARV threshold to determine their maximum allowable offer. This conservative ceiling ensures that even if market conditions fluctuate, the project retains sufficient equity to cover the principal debt. Using a private money loan calculator to stress-test these thresholds allows developers to maintain strategic oversight, ensuring that their capital remains protected against unforeseen appraisal variances.

The Math of Origination Points

Origination points represent a significant upfront capital allocation that must be factored into the project’s total cost of capital. Usually ranging between 2% and 3% of the total loan amount, these fees can substantially alter the effective interest rate over a short-term hold. To find the “real” monthly cost, you must amortize the cost of these points over the expected duration of the loan. A project with a lower interest rate but higher origination points may actually be more capital-intensive if the exit occurs sooner than anticipated. It’s vital to model these scenarios to avoid liquidity constraints during the final phases of a project. For those seeking to refine their capital structures, consulting with a strategic partner can help clarify how these fees impact your overall pro-forma.

Beyond these immediate costs, the loan term and potential extension options serve as vital safeguards for capital preservation. Project delays are a common reality in high-stakes development; therefore, modeling the cost of a three-month or six-month extension is a necessary component of any robust financial model. By accounting for these variables, you move from simple estimation to a level of analytical rigor that mirrors institutional-grade investment strategies.

Evaluating Repayment Architectures: Interest-Only vs. Balloon Structures

The architecture of a private money facility is fundamentally distinct from the self-amortizing structures found in traditional retail banking. While conventional mortgages focus on the gradual reduction of principal over thirty years, private capital is designed for speed and transitional efficiency. When utilizing a private money loan calculator, the primary objective is often the optimization of monthly liquidity rather than the retirement of debt. Most private money loans in 2026 are structured with interest-only payments, allowing developers to preserve their operational capital for project-specific expenses. This approach is particularly vital for managing new construction loans, where interest reserves are often utilized to mitigate the risk of carrying costs before the asset begins generating revenue.

Liquidity Benefits of Interest-Only Payments

Interest-only debt service serves as a powerful lever for maximizing cash-on-cash returns during the hold period. By deferring principal repayment, investors can reinvest their monthly cash flow into property improvements or other high-yield opportunities. This liquidity is essential in multi-family stabilization projects where the goal is to increase the Net Operating Income (NOI) before transitioning to permanent financing. A private money loan calculator helps model these scenarios by comparing the monthly debt service of an interest-only facility against an amortized alternative. The results often reveal a significant delta in available capital, which can be the difference between a project’s success and a liquidity crunch. In the first quarter of 2026, the funding of 1,683 short-term private money loans in California demonstrates how pervasive this strategy has become among professional developers.

Navigating the Balloon Payment Exit

A balloon payment represents a terminal capital event that requires meticulous planning from the inception of the loan. Since these facilities typically carry terms ranging from 6 to 36 months, the exit strategy must be clearly defined and stress-tested. Whether the plan involves a property sale or a refinance into long-term debt, timing is the most critical variable. Analytical rigor suggests that investors should model multiple exit valuations to account for potential market volatility. With Moody’s predicting the private credit market will exceed $3 trillion by 2028, the availability of “take-out” financing is expected to remain robust. However, the implementation of the FinCEN Residential Real Estate Rule on March 1, 2026, adds a layer of regulatory oversight that may impact the speed of non-financed transfers. Successful developers use these models to ensure they have sufficient capital to satisfy the principal debt at maturity, maintaining their standing with institutional partners.

Risk mitigation in this environment depends on a disciplined approach to contingency modeling. It’s not enough to assume a best-case scenario. Professional investors calculate their total loan costs at exit, including any potential extension fees, to ensure the project remains profitable even if the timeline shifts by several months. This level of strategic oversight transforms a simple loan into a sophisticated tool for wealth creation.

Strategic Integration into Real Estate Investment Pro-Formas

The transition from a conceptual investment thesis to a finalized project budget requires a rigorous synthesis of all anticipated capital costs. While retail investors may view a private money loan calculator as a means to verify monthly affordability, institutional partners utilize these data points to perform sophisticated sensitivity analyses. By modeling how a 1% increase in private capital rates impacts the Net Present Value (NPV) of a development, a steward of capital can determine the precise threshold at which a project ceases to be viable. This analytical discipline allows for the justification of capital allocation to equity partners, providing a transparent view of the risk-adjusted returns associated with the debt structure. Precision dictates success.

Modeling ROI and IRR with Private Capital

The strategic use of private money is often predicated on the leverage effect, where the deployment of non-institutional debt increases the Internal Rate of Return (IRR) despite the higher cost of capital compared to traditional bank facilities. When a developer utilizes a private money loan calculator, they must account for comprehensive holding costs that extend beyond the simple interest expense, including property taxes, insurance, and maintenance reserves. Precise debt modeling serves as a critical safeguard that prevents the erosion of principal and ensures the long-term preservation of investor equity. By maintaining a clear understanding of these variables, sophisticated investors can optimize their capital stacks to achieve superior performance metrics without compromising the project’s defensive posture. The results are cumulative.

DSCR and Long-Term Rental Viability

For those acquiring income-producing assets, the Debt Service Coverage Ratio (DSCR) remains the primary metric for evaluating long-term viability. A property must generate sufficient Net Operating Income (NOI) to comfortably cover the debt service, a calculation that becomes increasingly complex when transitioning from a short-term bridge facility to permanent financing. This modeling is essential for commercial real estate loans, where the break-even point is dictated by the interplay between debt service and property management expenses. Identifying this point early in the acquisition phase ensures that the investor has a clear path to stabilization and eventual recapitalization. To ensure your pro-forma reflects the most accurate market conditions, you should analyze your project’s financial architecture with JGL Capital.

The inclusion of these metrics within a comprehensive pro-forma demonstrates a level of strategic oversight that distinguishes professional developers from speculative participants. It provides a methodical presentation of facts that builds a persuasive case for the firm’s competence, fostering a sense of security among high-net-worth individuals and institutional allies. By framing these activities as a form of high-level partnership, you align the interests of all stakeholders involved in the value creation process.

Beyond the Algorithm: Bespoke Capital Solutions with JGL Capital

Digital tools provide a necessary mathematical foundation, yet they lack the cognitive depth required to navigate the intricacies of high-stakes real estate development. A private money loan calculator is an effective starting point for preliminary due diligence; however, it remains a static instrument in an increasingly complex and regulated market environment. JGL Capital leverages over 30 years of industry expertise to provide a level of security and strategic oversight that a standard spreadsheet simply cannot replicate. This transition from theoretical modeling to funded reality is where the alignment of interests between a developer and their capital partner becomes paramount, ensuring that every financial structure is designed for the long-term preservation of wealth and the achievement of specific strategic objectives.

The Value of a Strategic Ally

The firm specializes in providing tailored financial structures that automated systems often ignore, such as bespoke draw schedules and customized repayment architectures. JGL Capital optimizes loan structures based on specific project milestones, ensuring that capital is available exactly when it’s needed to maintain project velocity. For high-net-worth developers, the benefit of a discreet, institutional-grade partner extends beyond mere funding; it involves a collaborative approach to value creation that prioritizes integrity. There are numerous scenarios, such as complex cross-collateralization or unique interest reserve requirements, where “off-the-shelf” calculators fail to provide the necessary clarity. By providing bespoke solutions that account for these nuances, the firm acts as a disciplined steward of capital, moving beyond the limitations of automated algorithms to deliver precise, actionable results.

Securing Your Capital Allocation

The movement from calculation to closing is defined by the JGL Capital advantage in execution speed, a critical factor in a market where the U.S. private credit market is projected to exceed $3 trillion by 2028. Our streamlined application process for bridge and construction financing is designed to minimize administrative friction while maintaining the analytical rigor required for asset-based underwriting. This efficiency ensures that developers can secure opportunistic acquisitions with the confidence that their capital partner is deeply invested in the project’s success. It’s this commitment to tailored financial structures and timeless principles of finance that distinguishes a true strategic ally from a transactional service provider. We invite you to experience a partnership grounded in analytical rigor and a rejection of speculative trends. Engage with JGL Capital for a tailored evaluation of your next acquisition.

Mastering Asset-Backed Capital Allocation in a Sophisticated Market

The evolution of the private credit market, which Moody’s predicts will exceed $3 trillion by 2028, necessitates a transition from basic estimation to institutional-grade financial modeling. While utilizing a private money loan calculator provides the essential quantitative foundation for evaluating debt service and exit costs, the true value lies in the integration of these metrics into a broader strategic pro-forma. Achieving superior risk-adjusted returns requires more than automated data; it demands a disciplined approach to capital stewardship and the alignment of interests with a seasoned partner who understands the gravity of high-stakes management.

JGL Capital offers over 30 years of strategic capital expertise, providing a discreet partnership for high-net-worth real estate investors seeking asset-backed lending with a national reach. We invite you to move beyond the limitations of standard algorithms and secure your next acquisition with professional certainty. Consult with JGL Capital for a Bespoke Financing Strategy to ensure your project’s financial architecture is as resilient as the assets you develop. Your commitment to analytical rigor today will serve as the cornerstone for the lasting legacies you build tomorrow.

Frequently Asked Questions

What is the typical interest rate for a private money loan in 2026?

In the first quarter of 2026, average interest rates for California private money loans ranged between 10.05% and 10.40%. Broader market data for hard money facilities indicates a range from 9.5% to 15% or higher, depending on the lien position. These rates reflect the risk-adjusted nature of asset-backed capital, where the property’s intrinsic value serves as the primary security for the lender.

How do origination points affect the total cost of a private money loan?

Origination points increase the effective interest rate by adding upfront capital costs that are typically paid at the closing of the facility. In early 2026, these fees averaged 2.3% of the total loan amount. When you input these figures into a private money loan calculator, the tool amortizes the cost over the loan’s duration to reveal the true cost of capital for your project.

Can I use a private money loan calculator for new construction projects?

Professional developers frequently use a private money loan calculator to model the financial architecture of new construction projects, specifically to account for interest reserves and draw schedules. These calculators help ensure that sufficient liquidity is maintained throughout the build phase before the asset reaches stabilization. It’s a vital step for maintaining strategic oversight during complex development timelines.

What is the difference between LTV and LTC in private money calculations?

Loan-to-Value (LTV) measures the loan amount against the property’s appraised value, whereas Loan-to-Cost (LTC) compares the loan amount to the total project budget, including acquisition and renovation. While the average LTV in 2026 was approximately 67%, LTC ratios provide a clearer picture of the developer’s equity and the total capital allocation required to reach completion.

Is an interest-only payment structure better for fix and flip investors?

An interest-only payment structure is generally preferred by fix and flip investors because it maximizes monthly cash flow by deferring principal repayment. This liquidity allows developers to reinvest their capital into property improvements, which is essential for meeting the 70% to 75% ARV thresholds common in the 2026 market. It’s a tactical choice that aligns with the short-term nature of the investment.

How does a balloon payment work at the end of a private money loan term?

A balloon payment is a terminal capital event where the entire remaining principal balance becomes due at the end of the loan term, which typically ranges from 6 to 36 months. Investors must plan their exit strategy, such as a property sale or a refinance into long-term debt, to satisfy this obligation. Failing to account for this payoff can jeopardize the project’s final risk-adjusted returns.

Will my credit score impact the results of the private money calculator?

While private capital providers prioritize asset value and project viability, a borrower’s credit history may still influence the final interest rate premium or the required down payment. However, the primary focus remains on the property’s equity position. This approach allowed for the funding of 1,683 short-term loans in California during Q1 2026 despite varying borrower profiles, as it’s the asset that secures the debt.

What fees should I include when modeling the total cost of capital?

When modeling the total cost of capital, you should include origination points, appraisal fees, legal expenses, and processing costs. Accurate financial modeling requires a comprehensive view of all capital requirements to ensure that the project’s returns remain within the intended parameters of your investment thesis. It’s the only way to maintain a defensive and productive posture in high-stakes financial management.