The prevailing belief that speculative development is a volatile gamble ignores the reality that, for the disciplined developer, it’s a precise mechanism for capital optimization. You likely understand the friction caused when institutional-grade opportunities are missed because your liquidity is trapped by traditional underwriting or slow draw processes that halt construction momentum. Obtaining spec home financing for builders shouldn’t be a hurdle to overcome; it’s a strategic partnership designed to maintain construction momentum and exploit the national housing deficit.

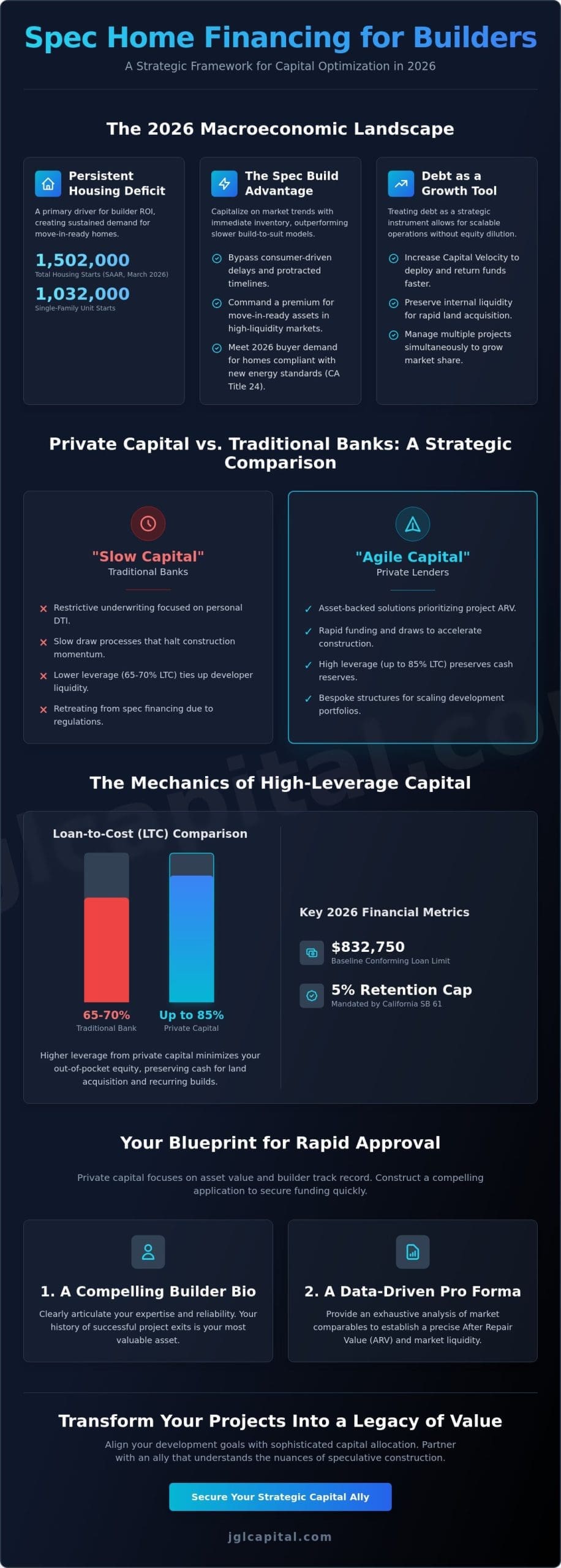

This analysis provides a rigorous framework for securing high-leverage capital, such as 85% loan-to-cost (LTC) structures, which allow you to preserve cash reserves for recurring builds. You’ll discover how to navigate the 2026 landscape, including the $832,750 baseline conforming loan limits and the new 5% retention cap mandated by California SB 61. We examine the transition from restrictive bank debt to agile, asset-backed solutions that prioritize project value over personal income, ensuring your portfolio remains resilient in a rebalancing market. By aligning your development goals with sophisticated capital allocation strategies, you can transform individual projects into a legacy of sustained value creation.

Key Takeaways

- Gain a strategic understanding of how spec home financing for builders serves as essential transitional capital to exploit the persistent housing supply deficit in 2026.

- Master the mechanics of institutional underwriting by focusing on After Repair Value (ARV) and Loan-to-Cost (LTC) ratios to maximize your project’s risk-adjusted returns.

- Analyze the hidden costs of “slow capital” from traditional lenders and how the agility of private capital can accelerate your construction momentum and land acquisition.

- Learn to construct a compelling Builder Bio and Project Pro Forma that clearly articulate market liquidity and your historical track record of successful project exits.

- Discover how bespoke, asset-backed financing solutions provide the strategic oversight necessary to scale your residential development portfolio while preserving internal liquidity.

The Evolution of Speculative Construction Financing in 2026

Speculative construction financing represents a sophisticated deployment of transitional capital, specifically engineered for residential projects initiated without a pre-existing purchase contract. In the fiscal environment of 2026, this instrument has transitioned from a niche funding source to a critical component of institutional-grade project management. As traditional depository institutions continue to retreat into more restrictive underwriting postures, private capital markets have emerged as the primary stewards of builder liquidity. This shift is not merely a reaction to banking regulations but a strategic evolution within the real estate development process, where speed and certainty of execution dictate market leadership. Securing spec home financing for builders enables a transition from reactive project management to a proactive, inventory-driven model that captures market share before competitors can break ground.

The Macroeconomic Necessity for Speculative Builds

The national housing deficit remains a primary driver of builder ROI, with March 2026 data indicating a seasonally adjusted annual rate of 1,502,000 housing starts. Of these, single-family units account for 1,032,000 starts, reflecting a robust yet undersupplied market. Builders who utilize spec home financing for builders effectively bypass the protracted timelines associated with build-to-suit contracts, which often suffer from consumer-driven delays. In high-liquidity suburban markets, move-in-ready assets are commanding a premium. This is particularly true as 2026 buyer preferences shift toward homes that already meet the rigorous electrification and energy efficiency standards of California’s Title 24 update, which became effective on January 1, 2026. A build-to-sell strategy allows developers to capitalize on these trends with immediate inventory, outperforming the slower build-to-suit models in both margin and volume.

Debt as a Tool for Scalable Development

Relying on internal equity to fund construction, while seemingly conservative, often restricts a firm’s capacity to capture emerging land opportunities. Strategic leverage allows for the simultaneous management of multiple projects, significantly increasing capital velocity. This metric measures the speed at which capital is deployed and returned; it’s essential for maintaining a competitive market share. From an institutional perspective, the goal is to achieve superior risk-adjusted returns by utilizing asset-backed debt to preserve liquidity. This disciplined approach ensures that a builder’s balance sheet remains flexible. It allows for the rapid acquisition of inventory when market conditions signal an entry point. By treating debt as a strategic instrument rather than a liability, professional developers can scale their operations without the dilution of equity or the stagnation of capital tie-ups.

Underwriting the Asset: Mechanics of Spec Home Capital

The underwriting of speculative assets necessitates a paradigm shift from borrower-centric credit metrics toward asset-centric valuation strategies. While traditional retail mortgages prioritize personal debt-to-income ratios, spec home financing for builders emphasizes the intrinsic value of the proposed structure and the feasibility of its “as-completed” appraisal. This rigorous process begins with an exhaustive analysis of market comparables to establish a precise After Repair Value (ARV). This figure serves as the cornerstone for all subsequent risk-adjusted return calculations, ensuring that the capital allocated is commensurate with the project’s exit potential.

Loan-to-Cost (LTC) and Equity Requirements

Institutional lenders utilize Loan-to-Cost (LTC) as the primary benchmark for capital deployment in new construction. In the 2026 lending environment, traditional depository institutions typically restrict LTC to a range of 65% to 70%, which can significantly tie up a developer’s liquid reserves. In contrast, sophisticated private capital partners may extend leverage up to 85% for developers with a documented history of successful exits. This higher leverage threshold is crucial for builders who wish to minimize out-of-pocket capital. By leveraging existing land equity, developers can often meet their contribution requirements without depleting cash reserves, allowing for a more efficient allocation of capital across multiple project sites.

The Anatomy of the Draw Schedule

A granular understanding of How Construction Loans Work is essential for maintaining construction momentum and operational velocity. Unlike standard term loans, spec home capital is disbursed through a stage-funded mechanism that mirrors the physical progression of the build. Each disbursement is preceded by an independent inspection to verify that specific milestones, such as foundation completion, vertical framing, or mechanical rough-ins, have been met with precision. This “inspection and release” cadence protects the lender’s interest while ensuring the builder has the necessary liquidity to satisfy subcontractors and material suppliers. During this phase, the strategic use of interest-only payments serves to minimize carrying costs, which is vital for maximizing the project’s net profitability upon its eventual sale.

The general contractor’s track record serves as a vital qualitative metric in the risk assessment process. Lenders scrutinize previous project timelines and budget adherence to confirm that the builder possesses the operational discipline required to execute the proposed pro forma. A builder’s ability to demonstrate a history of staying within 5% of original budget estimates often leads to more favorable terms. Ultimately, the synergy between a realistic construction budget and an authoritative “as-completed” appraisal dictates the quality of the financing offer. Professional builders who prioritize these technical details position themselves as lower-risk partners, securing the institutional-grade debt necessary to scale their operations in a competitive market.

Private Capital vs. Traditional Banks: A Strategic Comparison

Professional developers often evaluate debt quality through the narrow lens of interest rates, a perspective that frequently overlooks the profound impact of capital velocity on portfolio performance. While traditional depository institutions may offer rates between 6.5% and 9.5%, the associated underwriting friction creates “slow capital” that can stifle construction momentum. In contrast, spec home financing for builders sourced from private capital markets prioritizes certainty of execution, which is an indispensable asset for securing land in high-demand corridors. Speed of execution isn’t just a convenience; it’s a competitive advantage that allows builders to lock in land opportunities before competitors can navigate a bank’s committee-driven approval process.

The Hidden Cost of Traditional Financing Delays

A 60-day delay in bank closing doesn’t merely postpone a project; it inflates total carry costs and generates a significant opportunity cost. In a market where single-family housing starts reached 1,032,000 units in March 2026, the ability to break ground immediately is a distinct competitive advantage. Traditional debt-to-income (DTI) requirements often disqualify capable builders from pursuing multiple concurrent projects, effectively capping their growth potential. Institutional partners understand that new construction loans tailored to speculative timelines provide a more strategic alignment of interests than generic bank products.

Asset-Based vs. Credit-Based Underwriting

The fundamental distinction between these capital sources lies in the focus of the risk assessment. Traditional banks meticulously scrutinize personal tax returns and historical income, whereas private lenders adopt an asset-based approach that prioritizes project profitability and “as-completed” value. This “common sense” methodology, often employed by hard money lenders Florida and national private entities, evaluates the underlying real estate as the primary security. It allows builders to leverage their track record rather than just their personal balance sheet.

Understanding how construction loans work in an institutional context involves the frequent use of a Special Purpose Entity (SPE). This structure isolates project-specific risks, allowing for a more disciplined approach to wealth preservation and strategic oversight. By bypassing the rigid underwriting of traditional banks, builders can maintain a steady rhythm of development, ensuring that capital is always deployed where it generates the highest risk-adjusted returns. This transition from credit-based to asset-based financing represents a more sophisticated stage of capital allocation for the professional developer.

Optimizing the Spec Loan Application for Rapid Approval

The transition from a speculative concept to a funded project relies heavily on the builder’s ability to present a cohesive, data-driven narrative. Securing spec home financing for builders with optimal speed requires more than a viable plot of land; it demands a meticulously prepared package that mirrors institutional standards. Lenders prioritize submissions where architectural plans and permits are already finalized, as this readiness signals that the project is “shovel-ready” and mitigates the risk of bureaucratic delays. A comprehensive “Builder Bio” serves as a qualitative audit of professional competence, providing a transparent record of successfully completed and exited projects. This track record functions as a form of reputational equity, often allowing for more flexible terms when traditional credit metrics might suggest a more conservative posture.

The Professional Pro Forma and Budgeting

A professional construction budget must transcend simple cost estimation, incorporating a granular analysis of all hard and soft costs. In the 2026 development landscape, institutional lenders expect a dedicated contingency fund, typically ranging from 5% to 10% of the total construction cost, to absorb potential fluctuations in material pricing or labor availability. This pro forma should clearly demonstrate market liquidity by presenting recent comparables that support the projected After Repair Value (ARV). When your financial model aligns with current market data, it instills a sense of security in the capital provider. Demonstrating that your project can withstand a 10% market correction while still maintaining a positive risk-adjusted return is a hallmark of sophisticated capital allocation.

Defining the Exit Strategy

Lenders favor projects that possess multiple viable paths to capital return. While the primary objective of a build-to-sell model is a rapid disposition, current days-on-market (DOM) trends in 2026 may necessitate a secondary strategy. A build-to-rent fallback provides a necessary safety net, especially when supported by a transition to rental property loans. This dual-exit approach ensures that the project remains a performing asset regardless of short-term shifts in buyer demand. Understanding what is a bridge loan can also be beneficial, as it serves as a strategic takeout mechanism that allows builders to retire construction debt and hold the property for long-term appreciation. By articulating a clear hierarchy of exit strategies, you present yourself as a disciplined steward of capital. To ensure your next project meets these rigorous institutional standards, you should consult with a capital partner who understands the nuances of sophisticated residential development.

JGL Capital: Your Strategic Ally in Residential Development

JGL Capital functions as a disciplined steward of capital, providing the strategic oversight necessary for professional developers to scale their operations with confidence. In an era where market volatility requires a steady and experienced hand, our firm leverages thirty years of industry expertise to navigate the complexities of residential development. We don’t merely provide liquidity; we offer a high-level partnership that prioritizes long-term growth and the preservation of capital. By aligning our interests with those of our clients, we ensure that every deployment of spec home financing for builders is calculated to maximize risk-adjusted returns while maintaining the flexibility required for recurring builds. This commitment to integrity and analytical rigor distinguishes our firm as a seasoned ally for high-net-worth individuals and institutional partners alike.

Bespoke Solutions for Institutional Partners

Our approach to capital allocation is rooted in the delivery of tailored solutions that address the specific nuances of each residential project. We recognize that institutional partners require more than generic financial products; they need commercial real estate loans that are structured around precise project milestones and construction timelines. This commitment to bespoke financing ensures that capital is available exactly when it’s needed, which maintains project momentum and operational velocity throughout the construction lifecycle. Initiating a strategic capital consultation with our team allows for a thorough due diligence process, where we evaluate the underlying asset and the builder’s track record to create a financing framework that supports scalable growth. Transparency remains at the core of our operations, ensuring that every strategic objective is clearly defined and every claim is qualified by data.

The JGL Advantage: Precision and Speed

The JGL advantage is defined by a rigorous analytical framework that prioritizes project-based underwriting over the restrictive personal metrics favored by traditional banks. We provide a streamlined alternative for professional developers who value precision and speed in equal measure, allowing them to secure land opportunities that would otherwise be lost to bureaucratic delays. Our disciplined approach to wealth creation is grounded in the belief that a reliable capital partner should act as an extension of the builder’s own strategic planning. We invite you to experience a more sophisticated form of partnership, one where your intellectual capital and development expertise are met with the institutional-grade funding they deserve. Contact JGL Capital to discuss your 2026 speculative development strategy and secure the stewardship your portfolio requires to build a lasting legacy.

Navigating the Future of Residential Development

The 2026 residential landscape demands a departure from traditional, restrictive lending models toward a more agile, asset-centric approach to capital allocation. By prioritizing “as-completed” valuations and high-leverage Loan-to-Cost (LTC) ratios, professional developers maintain the capital velocity necessary to exploit the national housing deficit. Success in this rebalancing market depends on the strategic selection of spec home financing for builders that values project profitability over personal debt metrics. It’s a fundamental shift that empowers builders to secure land and maintain momentum without the friction of conventional underwriting.

JGL Capital remains a steadfast partner in this endeavor, offering over 30 years of industry expertise and a national reach that provides localized asset-based insight. Our firm’s commitment to bespoke capital structures ensures that high-growth developers have the strategic oversight required to build lasting legacies. We invite you to Secure Your Next Project with JGL Capital’s Strategic Financing Solutions and experience the precision of institutional-grade stewardship. Your vision for scalable development deserves a partner who understands the gravity of high-stakes financial management and the importance of timely execution.

Frequently Asked Questions

What is the typical interest rate for spec home financing in 2026?

Interest rates for professional builders in 2026 typically range from 6.5% to 9.5% for bank-led financing, while broader construction lending for speculative projects often falls between 9% and 14% depending on the borrower’s experience. These figures reflect the risk-adjusted returns required by institutional partners in the current economic environment. Factors such as the project’s location and the builder’s liquidity profile will ultimately dictate where a specific offer falls within this spectrum.

How much down payment or equity do builders need for a spec construction loan?

Experienced developers can often secure spec home financing for builders with as little as 15% equity, provided the project demonstrates strong market comparables and a robust after-repair value. While traditional banks typically require a 30% to 35% capital contribution, private capital partners allow builders to leverage land equity to minimize out-of-pocket expenses. This strategic use of leverage is essential for maintaining capital velocity and funding multiple concurrent projects in high-demand suburban markets.

Can a first-time builder qualify for speculative home financing?

A first-time builder can qualify for speculative financing by partnering with an experienced general contractor who possesses a documented track record of successful project exits. Lenders prioritize the operational discipline of the building team; therefore, a novice developer may need to provide a more substantial equity contribution or a comprehensive project pro forma to mitigate perceived risk. Demonstrating a clear alignment of interests with seasoned professionals often bridges the gap in individual experience.

What is the difference between a custom construction loan and a spec loan?

The primary distinction lies in the exit strategy; a custom construction loan is secured for a specific end-user with a pre-existing contract, whereas a spec loan is transitional capital for uncontracted inventory. Speculative builds require a more rigorous analysis of market liquidity and days-on-market trends, as the lender’s primary security is the asset’s eventual sale to the open market. This requires the builder to provide a more sophisticated market analysis during the underwriting process.

How do draw schedules work in speculative home building?

Draw schedules function as a stage-funded mechanism where capital is disbursed only after specific physical milestones, such as foundation pouring or vertical framing, are verified by an independent inspector. This process ensures that the funding remains commensurate with the project’s progression, protecting the interests of the capital partner while providing the builder with the necessary liquidity to maintain construction momentum. It’s a disciplined approach that ensures every dollar of capital is deployed toward tangible value creation.

What happens if the spec home does not sell before the loan term expires?

If a project remains unsold as the loan term approaches maturity, builders typically transition the debt into a bridge loan or a long-term rental property loan to retire the construction capital. This pivot allows the developer to hold the asset for rental income or wait for more favorable market conditions, ensuring that the initial investment remains a performing asset within their portfolio. Sophisticated developers always identify these secondary exit paths during the initial capital allocation phase.

Are personal credit scores a primary factor in spec home loan approval?

Personal credit scores are a secondary consideration in asset-based lending, as the primary focus remains on the project’s profitability and the builder’s historical track record. While a score above 680 is generally preferred to demonstrate financial responsibility, sophisticated lenders prioritize the “as-completed” appraisal and the feasibility of the exit strategy over individual credit metrics. This allows professional builders to scale their operations based on the strength of their assets rather than personal balance sheets.

How long does it take to close a private money spec construction loan?

Private money construction loans often close within 14 to 21 days, providing a significant speed advantage over the 60-day timelines typical of traditional depository institutions. This accelerated pace is essential for builders who need to secure land opportunities or maintain construction velocity in a competitive landscape where delayed capital can lead to substantial opportunity costs. Precision in the initial application package is the primary driver of this expedited closing timeline.