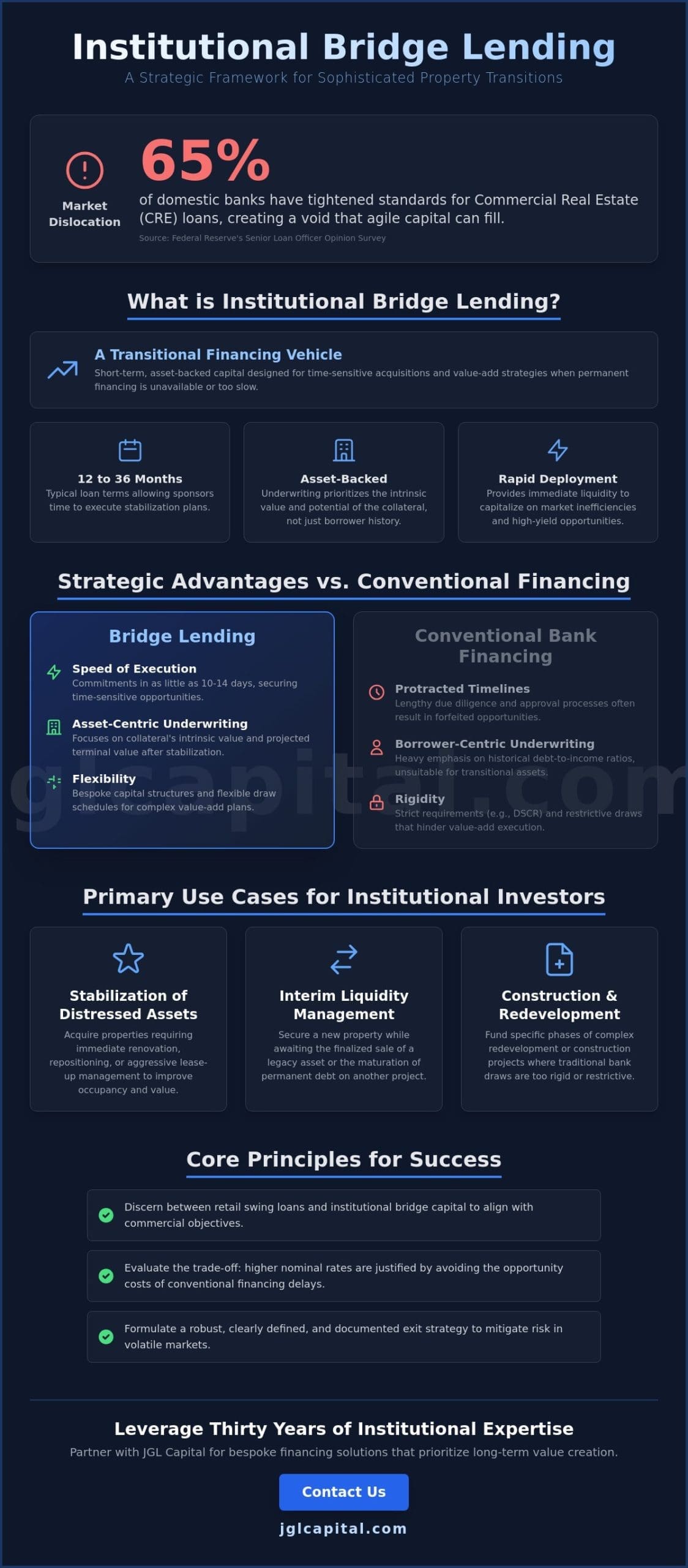

The traditional reliance on conventional bank financing for transitional assets is no longer a viable strategy for the disciplined institutional investor seeking to capitalize on current market dislocations. While the Federal Reserve’s Senior Loan Officer Opinion Survey recently indicated that 65 percent of domestic banks tightened their standards for commercial real estate loans, the necessity for agile bridge lending solutions has never been more acute. You’ve likely found that the rigid underwriting and protracted timelines of depository institutions often result in the forfeiture of high-yield opportunities; it’s a systemic friction that undermines the execution of complex value-add strategies.

This article serves as a comprehensive institutional framework for utilizing bridge lending as a catalyst for sophisticated property transitions. We’ll examine how bespoke capital structures can bridge the gap to permanent financing, allowing you to secure immediate acquisitions while maintaining the analytical rigor required for long-term wealth preservation. Our analysis explores the optimization of risk-adjusted returns and the precise mechanics of transitioning from short-term debt to a stabilized capital stack.

Key Takeaways

- Discern the fundamental distinctions between retail-level swing loans and institutional bridge lending to better align your capital structure with sophisticated commercial objectives.

- Evaluate the strategic trade-off between nominal interest rates and the significant opportunity costs associated with the inherent delays of conventional permanent financing.

- Master the mechanics of asset-backed underwriting, prioritizing the intrinsic value of collateral to facilitate complex, time-sensitive real estate acquisitions.

- Formulate robust risk mitigation protocols by establishing clearly defined and documented exit strategies essential for navigating volatile market conditions.

- Leverage thirty years of institutional expertise to secure bespoke financing solutions that prioritize long-term value creation and strategic property transitions.

Defining Bridge Lending in the Context of Institutional Real Estate

Institutional capital allocation requires a nuanced understanding of how debt instruments facilitate asset stabilization. Within this framework, bridge lending functions as a transitional financing vehicle for time-sensitive real estate acquisitions where traditional permanent debt remains inaccessible. Unlike consumer-facing “swing loans” used by homeowners to manage residential transitions, institutional bridge capital targets commercial assets with complex business plans. These loans occupy a critical position in the capital stack, providing the necessary leverage for value-add and opportunistic strategies that demand rapid deployment. Bridge lending is a short-term, asset-backed solution for liquidity gaps.

While a standard bridge loan definition identifies the product as an interim financing option, in the institutional sphere, it represents a sophisticated tool for navigating market inefficiencies. These facilities typically feature terms ranging from 12 to 36 months, allowing sponsors to execute capital improvement plans or resolve vacancy issues before seeking long-term agency or CMBS financing. This flexibility is essential for assets that don’t yet meet the debt service coverage ratio requirements of conservative bank lenders.

The Core Philosophy of Transitional Capital

In high-stakes transactions, the speed of execution often outweighs the nominal cost of capital. Strategic investors recognize that securing a distressed or high-potential asset within a 14-day window provides a competitive advantage that justifies a higher interest rate. This approach ensures an alignment of interests between the lender and the investor; both parties prioritize the successful execution of a stabilization plan to ensure a profitable exit. For a foundational understanding of these mechanics, investors may reference our strategic guide to transitional real estate capital. The philosophy centers on stewardship and the calculated use of leverage to unlock inherent property value.

Primary Use Cases for Sophisticated Investors

Institutional bridge capital facilitates several distinct investment maneuvers that require agile funding structures:

- Stabilization of Distressed Assets: This involves the acquisition of properties requiring immediate renovation or aggressive management to improve occupancy rates.

- Interim Liquidity Management: Investors use bridge funds to secure a new property while awaiting the maturation of permanent debt or the finalized sale of a legacy asset.

- Construction Transitions: These loans provide funding for specific project phases where traditional bank draws are too restrictive, offering a more flexible draw schedule for complex redevelopments.

By utilizing bridge lending, sophisticated partners can navigate the gap between acquisition and stabilization. It’s a disciplined approach to wealth creation that relies on analytical rigor and a clear vision for the asset’s future. The focus remains on risk-adjusted returns and the precise articulation of strategic objectives.

The Mechanics of Asset-Backed Bridge Financing

The operational lifecycle of asset-backed financing initiates with a rigorous assessment of the underlying property’s intrinsic value. This transition from borrower-centric underwriting to collateral-focused analysis distinguishes bridge lending from traditional mortgage sectors. While conventional institutions emphasize historical debt-to-income ratios, it’s a model that prioritizes the asset’s current state and its projected terminal value. Private money brokers facilitate this by condensing the due diligence timeline, often securing commitments within 10 business days. This agility is essential for securing distressed assets or meeting strict acquisition deadlines that traditional banks cannot accommodate.

The bridge loan lifecycle follows a structured path from origination to exit. It begins with the submission of a comprehensive executive summary and pro forma, followed by a preliminary letter of intent. Once the valuation is verified, the lender moves into a rapid due diligence phase, focusing on title clarity and the feasibility of the renovation or repositioning plan. The exit is usually achieved through a long-term refinance or the sale of the stabilized asset, ensuring the capital is recycled efficiently.

The Underwriting Process: Valuation Over Credit

Underwriting protocols center on the Loan-to-Value (LTV) and After-Repair Value (ARV) metrics. Lenders frequently restrict initial disbursements to 70% of the current value, while total exposure may reach 75% of the ARV after accounting for renovation draws. Strategic oversight during this phase involves an exhaustive review of the borrower’s exit strategy, ensuring the transitional period is supported by realistic market data. Administrative tasks, including the collation of title reports and the execution of internal risk assessments, are executed with precision to maintain the integrity of the capital stack. Understanding the nuances of Commercial real estate financing is vital for developers who require capital that matches the pace of their project milestones.

Capital Allocation and Funding Timelines

Bridge facilities are structured as short-term instruments, typically ranging from 3 to 18 months in duration. These facilities often include extension options that provide flexibility if market conditions or construction schedules shift. The cost of capital is reflected in the interest rate and the “points” paid at closing, which represent a percentage of the gross loan amount, typically between 1% and 3%. These points provide the necessary liquidity to source private capital while aligning the interests of the lender and the borrower. By serving as a financial lifeline during complex, multi-stage transactions, these loans enable the preservation of equity during periods of illiquidity. A sophisticated capital allocation strategy ensures that these high-leverage opportunities are balanced against a broader framework of risk-adjusted returns.

Strategic Advantages: Bridge Lending vs. Conventional Permanent Financing

While conventional permanent financing offers lower nominal interest rates, its rigid underwriting criteria often render it unsuitable for transitional assets or time-sensitive acquisitions. Bridge lending serves as a sophisticated alternative, prioritizing the intrinsic value of the underlying collateral over the borrower’s historical cash flow. This shift in perspective allows for a more agile deployment of capital in volatile markets where opportunities vanish within short windows.

Speed as a Competitive Moat

In institutional real estate, the ability to close a transaction within 10 to 14 business days often determines the success of an acquisition. Conventional lenders typically require 60 to 90 days for full due diligence, which includes exhaustive personal income verification and standardized appraisals. Bridge lending eliminates this friction by focusing on asset-based metrics. Rapid capital deployment preserves deal integrity, preventing the loss of earnest money deposits and securing favorable purchase prices that would otherwise be unavailable to those tethered to traditional banking cycles.

The higher cost of capital associated with bridge loans is often misconstrued as a disadvantage. When investors calculate the opportunity cost of a delayed closing, the interest rate premium becomes a secondary concern. For instance, losing a project with a projected 20% internal rate of return because a bank failed to fund on time represents a total loss of profit. A bridge loan, despite its higher coupon, secures that 20% return. It’s the more fiscally responsible choice for time-sensitive opportunities where the cost of inaction exceeds the cost of capital.

Flexibility in Loan Structure

Bridge structures offer bespoke solutions that align with the specific cash flow requirements of a transitional property. Interest-only payment structures are common, allowing developers to maximize liquidity during the renovation or stabilization phase. This level of customization distinguishes bridge loans from the rigid frameworks of traditional banks. When evaluating private capital allocation, sophisticated investors recognize that bridge lending provides a middle ground between high-cost hard money and slow-moving bank debt.

For fix-and-flip and ground-up developments, asset-based lending is the superior mechanism. This is particularly evident in this guide for real estate developers, which details how construction-specific draws and flexible release schedules facilitate smoother project management. By decoupling the loan from the borrower’s global cash flow, bridge lenders empower developers to scale their portfolios with greater precision. They value the project’s future potential rather than its current stagnation.

Ultimately, bridge lending functions as a strategic tool for portfolio optimization. It provides the necessary runway to execute a value-add business plan before transitioning into long-term, low-cost permanent debt. This phased approach ensures that capital is always aligned with the asset’s current lifecycle stage.

Critical Underwriting Criteria and Risk Mitigation

The deployment of bridge lending within a transitional capital stack demands a rigorous adherence to analytical precision. In a volatile market characterized by fluctuating cap rates and shifting liquidity profiles, institutional lenders prioritize assets with clear paths to stabilization. Conservative Loan-to-Value (LTV) ratios serve as the primary structural safeguard in transitional finance, effectively insulating the lender’s principal against market-wide price corrections and ensuring a sufficient equity cushion remains during periods of illiquidity. Most institutional bridge facilities in 2024 have retracted to the 60% to 70% LTV range to account for this heightened sensitivity to valuation volatility.

A primary concern for any sophisticated allocator is the “bridge to nowhere.” This occurs when a borrower secures short-term capital but fails to achieve the operational milestones necessary to qualify for permanent financing or a profitable divestment. To mitigate this, underwriting must focus on the feasibility of the pro-forma net operating income (NOI) and the realism of the timeline. If a project requires 24 months for stabilization, a 12-month bridge with no extension options represents a structural failure of capital allocation.

The Anatomy of a Strong Bridge Loan Application

Securing competitive terms requires more than just a viable asset; it demands a demonstration of institutional-grade stewardship. Lenders scrutinize the sponsor’s track record, specifically looking for successful completions of similar value-add programs between 2021 and 2024. A robust application includes:

- Third-party feasibility studies that validate local market demand and rent premiums.

- Detailed property appraisals that account for “as-is” and “as-stabilized” values.

- A comprehensive schedule of real estate owned (SREO) illustrating the sponsor’s liquidity and experience.

For a granular analysis of these requirements, please consult our commercial real estate loans guide which outlines the criteria for 2026 capital allocation.

Exit Strategy Optimization

The viability of bridge lending is inextricably linked to the exit strategy. A documented plan for refinancing into permanent debt, such as a conventional bank loan or a Debt Service Coverage Ratio (DSCR) facility, is mandatory. In the current interest rate environment, sponsors must stress-test their exit strategies against a 100 to 150 basis point increase in long-term rates to ensure the project remains bankable upon maturity.

Multi-family bridge loans are frequently utilized for property stabilization, allowing owners to increase occupancy or complete renovations before seeking agency financing. This strategic pause provides the necessary window to optimize the asset’s financial profile. It’s vital to align the loan term with the physical renovation schedule to avoid a liquidity crunch. By maintaining a disciplined approach to these underwriting standards, JGL Capital ensures that every capital infusion serves as a bridge to a stronger, more resilient portfolio. To discuss a bespoke capital solution for your next acquisition, connect with the experts at JGL Capital.

Partnering with JGL Capital for Bespoke Financing Solutions

JGL Capital functions as a disciplined steward of capital, drawing upon 30 years of institutional experience to facilitate complex real estate transactions across the United States. Our methodology transcends the traditional, often narrow, scope of transitional financing. We focus on long-term value creation and analytical rigor. This commitment ensures that every capital allocation aligns with the overarching strategic objectives of our partners. By maintaining a high-register, professional standard, we provide the stability required for high-stakes financial management. Effective bridge lending remains a vital instrument in our repertoire, allowing investors to bridge the gap between acquisition and long-term stabilization with absolute confidence.

Our national scope enables diverse portfolio optimization across various asset classes, from multi-family developments to sophisticated industrial conversions. We don’t just provide funds; we offer strategic oversight. We’ve built a reputation on the ability to analyze risk-adjusted returns with a level of precision that few firms can match. This disciplined approach is essential for wealth preservation in volatile markets. Our clients benefit from a streamlined brokerage process that prioritizes clarity over marketing hyperbole, ensuring that every transaction is grounded in factual due diligence.

A Legacy of Strategic Partnership

Transitioning from a transactional mindset to a collaborative alliance is the hallmark of the JGL Capital experience. We utilize our extensive private money brokerage network to source exclusive capital for niche deals that traditional banks often overlook. Our role is to serve as a sophisticated and knowledgeable entity that values integrity above all else. For those seeking tactical asset examples, we recommend reviewing our fix and flip strategic guide. This resource illustrates our approach to asset-backed evaluation and portfolio growth.

Securing Your Next Acquisition

Speed is a byproduct of our expertise, not a compromise of our standards. Our asset-backed review process is designed for efficiency, providing rapid funding without sacrificing the thoroughness of our underwriting. We remain committed to transparency and the preservation of investor wealth through every phase of the capital lifecycle. It’s our belief that a well-structured bridge lending solution is the foundation of a successful transitional strategy. We invite you to engage with our team to discuss your specific capital needs and witness our commitment to excellence firsthand. Partner with JGL Capital for your transitional funding requirements.

Optimizing Portfolio Trajectories with Strategic Transitional Capital

Mastering the intricacies of transitional real estate requires a sophisticated framework that balances immediate liquidity needs with long-term capital preservation goals. This strategic approach demonstrates how liquidity gaps are effectively managed during the 12 to 36 month stabilization period typical of value-add assets. We’ve established that bridge lending serves as a critical instrument for institutional investors, providing the agility necessary to execute on complex repositioning strategies where conventional permanent financing often falls short. By applying rigorous underwriting criteria and focusing on asset-backed specialization, partners can navigate market volatility while securing the necessary time to reach full stabilization. JGL Capital delivers this stability through over 30 years of industry expertise, applying a formal, institutional approach to private capital that ensures every allocation is grounded in analytical depth. Our national reach allows for the precise execution of transactions across diverse jurisdictions, reflecting a commitment to stewardship and the alignment of interests. It’s this disciplined oversight that transforms a simple transaction into a strategic partnership. We look forward to facilitating your next phase of institutional growth and wealth preservation.

Secure your transitional capital with JGL Capital today.

Frequently Asked Questions

What is the typical interest rate for a bridge loan in 2026?

Interest rates for bridge lending in 2026 typically range between 8.5% and 11% depending on the asset’s risk profile. These figures align with the Federal Reserve’s projected long-term neutral rate of 2.5% plus a standard risk premium of 600 basis points. Institutional lenders prioritize capital preservation. Consequently, rates fluctuate based on the Secured Overnight Financing Rate (SOFR) benchmarks.

How does bridge lending differ from a traditional hard money loan?

Bridge lending differs from traditional hard money loans through its reliance on institutional underwriting standards and lower cost of capital. While hard money often carries rates exceeding 12%, bridge capital typically stays below 10.5% for stabilized assets. Institutional structures offer 12 to 36 month terms, whereas hard money lenders usually restrict borrowers to 6 or 12 month windows. This distinction ensures a more disciplined approach to capital allocation.

What are the most common exit strategies for a bridge loan?

The primary exit strategies involve securing long-term permanent financing or executing a strategic asset disposition. Approximately 65% of borrowers transition into Agency or CMBS debt once the property reaches 90% occupancy. The remaining 35% typically sell the asset to realize capital gains. These pathways provide a clear trajectory for returning principal to investors while maintaining portfolio liquidity.

Can a bridge loan be used for new construction projects?

Bridge capital supports new construction projects specifically during the final phases of development or the initial lease-up period. Lenders provide these funds to retire high-cost construction debt once the certificate of occupancy is 100% complete. This strategy allows developers to stabilize the asset over a 24 month period before seeking permanent financing. It’s a vital tool for optimizing risk-adjusted returns in volatile markets.

What is the maximum Loan-to-Value (LTV) usually offered in bridge lending?

Institutional lenders generally cap the maximum Loan-to-Value (LTV) at 75% to maintain a conservative margin of safety. For high-conviction value-add projects, some firms extend to 80% Loan-to-Cost (LTC) if the debt service coverage ratio remains above 1.25x. These thresholds ensure that the sponsor maintains significant equity in the transaction. This alignment of interests protects the capital stack against potential market contractions.

How quickly can a bridge loan be funded compared to a bank mortgage?

Bridge loans typically fund within 21 to 45 days, providing a significant speed advantage over traditional bank mortgages. Conventional commercial banks often require 90 to 120 days to complete their more rigid committee reviews and appraisals. The streamlined due diligence process in bridge financing allows institutional partners to capture time-sensitive opportunities. This agility is essential for acquiring distressed assets or meeting strict 1031 exchange deadlines.

Are there prepayment penalties associated with institutional bridge loans?

Most institutional bridge structures don’t impose traditional prepayment penalties, though they often include a minimum interest requirement of 6 to 12 months. This yield maintenance ensures the lender achieves a baseline return on the deployed capital. After this initial period, borrowers can typically exit the loan without incurring additional fees. This flexibility is a hallmark of bespoke financial solutions designed for transitional real estate assets.

Is a personal credit score a primary factor in bridge loan approval?

A personal credit score isn’t the primary determinant in the approval process for institutional bridge capital. Lenders prioritize the asset’s net operating income and the sponsor’s track record of 5 or more successful projects. While a score below 680 might trigger additional scrutiny, the focus remains on the collateral’s intrinsic value. This analytical rigor ensures that capital is allocated based on project merit.