The traditional ninety-day bank underwriting cycle has transitioned from a standard procedure into a strategic liability for the modern institutional investor. While conventional lenders often prioritize rigid, formulaic credit requirements over the intrinsic value of a high-performing asset, a strategically structured bridge loan functions as a precision instrument for rapid capital allocation. This transitional financing allows investors to bypass the bureaucratic inertia that characterized much of the 2024 lending environment, ensuring that time-sensitive acquisitions are secured with the decisiveness that a competitive 2026 real estate market demands.

You likely recognize that the misalignment between immediate liquidity needs and long-term debt structures often results in missed opportunities and suboptimal risk-adjusted returns. It’s our objective to provide a sophisticated analysis of bridge financing as a primary tool for portfolio optimization, moving beyond simple transactional utility to explore its role in long-term wealth preservation. We’ll examine how bespoke capital solutions facilitate seamless transitions between asset classes and provide the necessary strategic oversight to navigate complex transitional periods with absolute confidence.

Key Takeaways

- Gain a sophisticated understanding of how to deploy transitional capital to secure immediate liquidity, allowing for the agile execution of investment strategies in a volatile market environment.

- Analyze the technical architecture of debt financing by examining the strategic application of LTV and LTC ratios to maximize risk-adjusted returns during the asset lifecycle.

- Identify high-value use cases where a bridge loan serves as a vital instrument for securing opportunistic acquisitions and funding early-stage development projects.

- Implement rigorous portfolio preservation techniques by establishing definitive exit trajectories that facilitate the seamless transition from short-term debt to permanent DSCR financing.

- Recognize the importance of institutional-grade stewardship by selecting a capital partner whose extensive industry tenure ensures the alignment of strategic interests and long-term value creation.

Defining the Strategic Role of Bridge Loans in Capital Allocation

A comprehensive overview of bridge loans reveals their primary function as a catalyst for immediate liquidity within a sophisticated investment portfolio. These instruments aren’t mere stopgap measures; they represent a deliberate strategic choice for asset managers who require the agility of asset-backed capital to capture time-sensitive opportunities. Unlike traditional long-term debt, which often involves protracted underwriting cycles, a bridge loan prioritizes the underlying collateral’s value to facilitate rapid deployment. This agility is essential for maintaining a competitive edge in high-stakes environments where capital must move at the speed of the market.

By the second quarter of 2026, the real estate landscape has transitioned into an era where capital efficiency is dictated by the ability to pivot. Sophisticated investors now prioritize execution speed over the nominal cost of capital. They recognize that the premium paid for transitional financing is often offset by the value created through early acquisition or the stabilization of distressed assets. The focus has shifted toward risk-adjusted returns where the certainty of closing outweighs the incremental savings of a lower interest rate that comes with institutional delays.

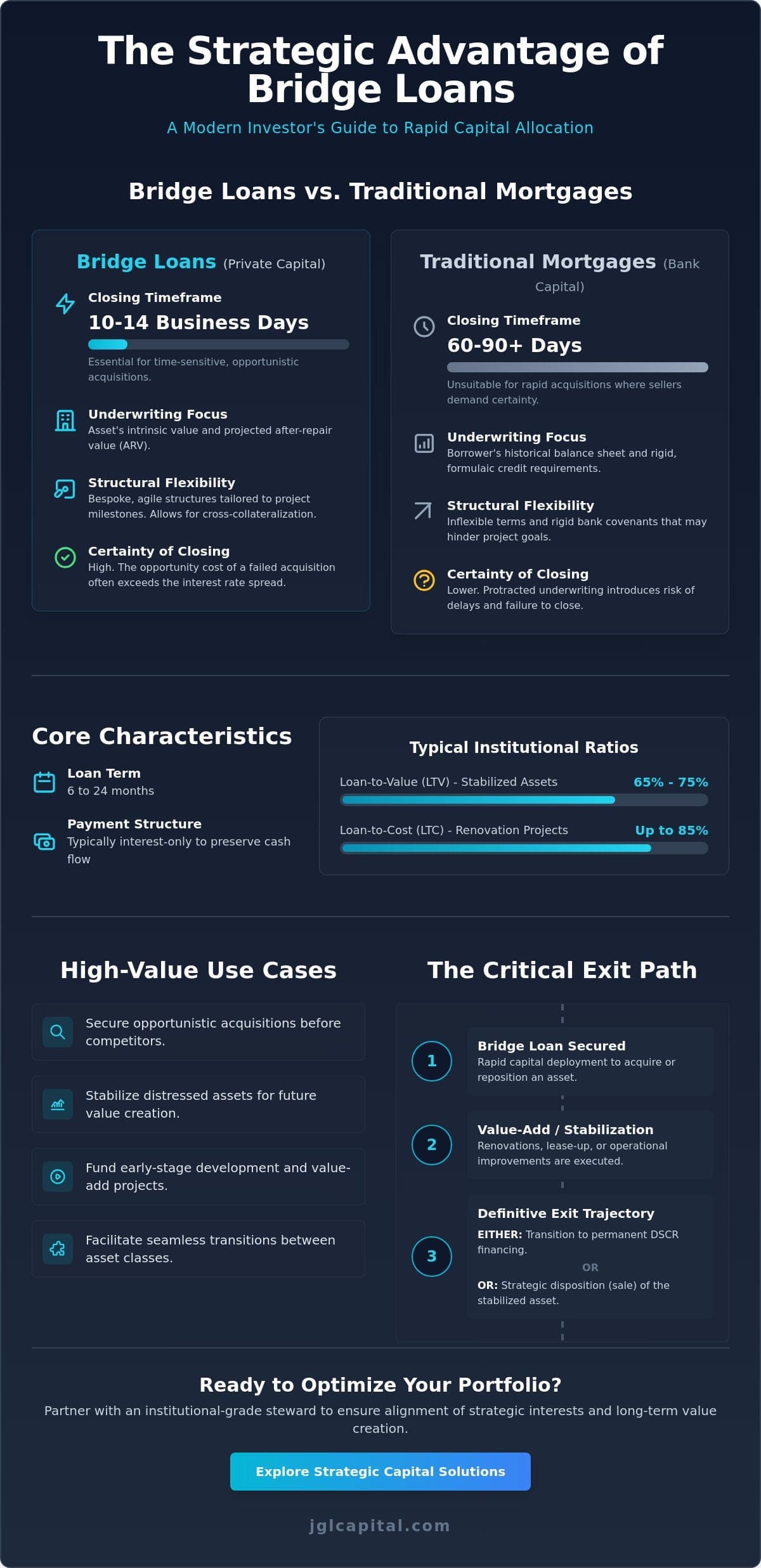

The Core Characteristics of Transitional Liquidity

Bridge financing typically operates within a brief duration ranging from six to twenty-four months. This window provides the necessary timeframe for a borrower to secure permanent financing or execute a value-add strategy. Most structures utilize interest-only payments to preserve operational cash flow during the critical early stages of an asset’s lifecycle. Underwriting has shifted significantly toward asset-centric risk assessment. Lenders in 2026 focus on the exit strategy and the property’s intrinsic potential rather than just the borrower’s historical balance sheet, ensuring that capital allocation remains grounded in the asset’s future performance.

Bridge Loans vs. Traditional Mortgages: A Tactical Comparison

The trade-off between institutional speed and conventional interest rates defines the tactical choice between private and bank capital. Traditional mortgages often require 60 to 90 days for closing. However, private money lenders can often fund within 10 to 14 business days. This discrepancy makes traditional financing unsuitable for rapid acquisitions where sellers demand certainty. Private money terms offer a flexibility that rigid bank covenants can’t match, allowing for bespoke structures that align with a project’s specific milestones. While bank rates might be lower, the opportunity cost of a failed or delayed acquisition frequently exceeds the interest rate spread of a bridge loan. Choosing the right capital partner ensures that the financing structure supports long-term wealth preservation rather than hindering it through inflexible terms.

Operational Mechanics and the Architecture of Bridge Debt

The lifecycle of a bridge loan represents a sophisticated sequence of capital deployment that commences with an analytical inquiry and concludes with a definitive strategic exit. This progression requires a disciplined approach to capital allocation, where the borrower and lender align on the eventual transition to permanent financing or asset disposition. Institutional lenders typically employ Loan-to-Value (LTV) ratios of 65% to 75% for stabilized assets, while Loan-to-Cost (LTC) ratios may reach 85% for projects involving significant renovation. Through the mechanism of cross-collateralization, investors can leverage equity in existing holdings to secure higher loan amounts, effectively reducing the requirement for immediate cash injections. This structural flexibility allows for the optimization of a portfolio’s total return profile without depleting liquid reserves.

The Underwriting Process: Prioritizing Asset Value

Institutional underwriting in the private debt sector prioritizes the intrinsic value of the real estate over the borrower’s personal financial history. Lenders conduct a rigorous evaluation of the “as-is” market value alongside the projected “after-repair” value (ARV) to ensure the collateral supports the debt service. Because the focus is on asset quality, the role of personal credit scores is often diminished in favor of the property’s income-producing potential or appreciation prospects. This shift in focus facilitates a rapid due diligence phase, often allowing a bridge loan to close within 10 to 14 business days. Such speed is vital for strategic use cases for bridge loans, including time-sensitive acquisitions where traditional bank timelines, which often exceed 45 days, would result in a lost opportunity.

Cost Structures and Interest Rate Dynamics

Pricing for bridge debt is structured to reflect the expedited nature of the funding and the specialized risk profile of transitional assets. The total cost of capital is a composite of interest rates, origination points, and administrative processing fees. Interest rates in the 2024 private lending market generally range from 8% to 12%, depending on the complexity of the transaction and the strength of the exit strategy. Points are a percentage of the total loan amount paid at closing. These higher risk-adjusted returns compensate the lender for providing liquidity in scenarios where traditional institutions remain sidelined. For investors seeking to enhance their wealth through bespoke capital allocation, understanding these cost drivers is essential for maintaining portfolio discipline. This methodical approach to pricing ensures that the interests of the lender and the borrower remain aligned throughout the investment horizon.

Strategic Use Cases for Professional Real Estate Investors

Sophisticated capital allocation requires a toolset that prioritizes speed and certainty of execution. The bridge loan serves as a critical instrument for investors targeting opportunistic acquisitions where the window of availability is narrow. In the 1031 exchange process, the 45-day identification period and 180-day closing requirement demand immediate liquidity that traditional institutional lenders often fail to provide. By utilizing transitional debt, investors maintain their tax-deferred status while securing high-yield assets that would otherwise be lost to competitors with more agile financing structures. It’s a method that values precision over the slow pace of conventional underwriting.

Value-add transformations in the multi-family and commercial sectors represent another primary application for this capital. When a property’s current net operating income doesn’t support long-term agency debt, transitional financing provides the necessary runway for renovations and lease-up activities. This strategic oversight allows the investor to stabilize the asset before seeking a permanent exit or recapitalization. During the credit tightening of 2023, this flexibility proved vital for maintaining portfolio health and ensuring that equity wasn’t trapped in underperforming assets.

New Construction and Development Financing

Early-stage development carries inherent risks that frequently cause conventional banks to hesitate. Developers utilize bridge capital to facilitate land acquisition and cover pre-development costs before a formal construction draw is established. This strategy ensures that project momentum remains uninterrupted during the critical entitlement and site preparation phases. For a more granular analysis of these dynamics, investors should consult our pillar on New Construction Loans. Maintaining this continuity is essential for preserving the projected internal rate of return on high-stakes builds. It’s about bridging the gap between a vision and a bankable project.

Fix and Flip: The Engine of Residential Redevelopment

For seasoned redevelopers, the bridge loan functions as an engine for capital velocity. It allows for the rapid acquisition of distressed properties that require immediate renovation to reach their highest and best use. By leveraging debt for both the purchase and the capital improvement budget, investors optimize their return on equity and preserve cash reserves for additional acquisitions. While our specific insights on Fix and Flip Loans in Florida highlight regional nuances, the underlying principle of using transitional debt to drive value remains a cornerstone of national investment strategies. This disciplined approach to redevelopment focuses on asset stabilization and a swift transition to permanent financing or divestment.

- Secures properties in competitive markets where cash-like speed is required.

- Provides capital for non-warrantable properties that don’t meet traditional standards.

- Allows for the execution of complex business plans that require 12 to 36 months of stabilization.

Refinancing and Exit Strategies: The Critical Path to Portfolio Preservation

The acquisition of a bridge loan isn’t an isolated financial event; it’s a tactical phase within a broader lifecycle of capital allocation. Investors shouldn’t enter into bridge debt without a rigorous, stress-tested exit strategy that accounts for both micro-level asset performance and macro-level economic shifts. This capital serves as a temporary conduit, bridging the gap between an asset’s current underperformance and its future stabilization. Without a clear path to liquidity, a transition can quickly devolve into a distressed liquidation. Institutional lenders prioritize the viability of the exit over the current state of the asset. The exit strategy is the most scrutinized element of the bridge loan application because it serves as the sole guarantee of principal repayment in a non-amortizing debt structure.

Transitioning to Permanent Debt Structures

The shift from high-cost transitional debt to stabilized financing requires precise timing and analytical rigor. Lenders evaluate the Debt Service Coverage Ratio (DSCR) to ensure net operating income comfortably exceeds debt obligations. A ratio between 1.20x and 1.35x typically serves as the minimum threshold for institutional quality assets in the current 2024 market. Investors aim to execute the “refi-out” immediately following the achievement of stabilized occupancy or the completion of capital expenditure programs. This captures the improved equity position created by the renovation. For those seeking a comprehensive understanding of long-term capital allocation, our guide on Commercial Real Estate Loans provides the necessary framework for permanent portfolio integration.

Contingency Planning for Market Volatility

Market conditions can shift significantly during the standard 12 to 36-month term of a bridge facility. If the primary exit strategy of a sale or refinance fails due to interest rate spikes or tightened credit markets, secondary liquidity options become vital. These contingencies often involve:

- Securing mezzanine debt to fill the gap during a “cash-in” refinance.

- Negotiating extension options based on pre-defined performance hurdles.

- Utilizing preferred equity infusions to maintain ownership during prolonged stabilization periods.

Choosing a bridge loan partner who understands these transitional hurdles is paramount. A lender with deep-seated expertise provides the stewardship needed to manage the “maturity wall” when interest rates are volatile. They prioritize long-term growth and integrity over transactional speed. This disciplined approach ensures that even when primary exits are delayed, the portfolio remains preserved through careful, deliberate action.

Selecting a Strategic Capital Partner for Bridge Financing

While the financial metrics of a bridge loan are undeniably critical, the identity of the lending partner often dictates the ultimate success of a transitional strategy. Selecting a capital source requires more than a comparison of interest rates; it necessitates an alignment of vision and a shared commitment to long-term value creation. Institutional investors and high-net-worth individuals require a partner capable of navigating the complexities of high-stakes real estate with a disciplined, analytical approach. JGL Capital serves as a sophisticated steward of capital, moving beyond the rigid, one-size-fits-all models of traditional institutional lending to offer bespoke solutions that reflect the unique exigencies of each asset.

The Advantages of Private Capital Brokerage

Private capital brokerage offers access to diverse funding pools that remain inaccessible to conventional banking institutions. These alternative channels provide the discretion and institutional gravity essential for complex, time-sensitive transactions. With over 30 years of industry expertise, JGL Capital leverages a deep-seated track record to provide clients with a distinct competitive edge in capital allocation. This level of strategic oversight ensures that every bridge loan is structured to optimize risk-adjusted returns while maintaining the flexibility required for rapid execution. The firm’s role involves more than simple facilitation; it’s a form of high-level partnership that prioritizes the preservation and growth of the client’s legacy.

- Access to non-bank liquidity providers and private debt funds.

- Sophisticated underwriting that recognizes value beyond standard credit scores.

- Discreet handling of sensitive financial data and high-profile acquisitions.

- Strategic alignment between borrower objectives and lender risk appetites.

Initiating Your Capital Strategy

Securing transitional capital begins with a rigorous, asset-based review designed to validate the underlying value of the collateral. To ensure rapid funding, investors should prepare a professional deal package that includes comprehensive property data, clear exit strategies, and detailed financial projections. This level of preparation mirrors the firm’s own commitment to precision and due diligence. A streamlined review process typically requires a clear executive summary of the investment thesis and a detailed schedule of real estate owned. Sophisticated investors recognize that speed and certainty of execution are the true hallmarks of a successful capital strategy. By engaging a partner that values integrity and intellectual capital, you ensure your project remains on a steady trajectory toward completion. Engage JGL Capital for your transitional capital needs to secure a disciplined ally in your next real estate endeavor.

Navigating the Path to Institutional Growth through Strategic Capital Allocation

The utilization of a bridge loan serves as a sophisticated mechanism for professional investors to navigate the complexities of transitional real estate markets. Success in these high-stakes environments depends on a rigorous understanding of operational mechanics and the disciplined execution of a predefined exit strategy. JGL Capital brings over 30 years of industry expertise in private capital markets to every transaction. We ensure that your investment philosophy remains intact throughout the lifecycle of the asset. Our firm’s approach relies on asset-based underwriting that prioritizes property value over conventional credit history. This methodology provides a stable foundation for portfolio optimization. We deliver bespoke capital solutions tailored to the unique requirements of complex investor portfolios. It’s essential to align with a partner who values analytical rigor and long-term value creation. By prioritizing the alignment of interests, we help you build a lasting legacy through careful, deliberate action.

Secure your next acquisition with JGL Capital’s strategic bridge solutions

Your vision for portfolio expansion deserves the precision and stability that only seasoned financial leadership can provide.

Frequently Asked Questions

What is the typical interest rate for a bridge loan in 2026?

Based on projections from the Mortgage Bankers Association, bridge loan interest rates in 2026 typically range from 8.5% to 12.5% depending on the Secured Overnight Financing Rate. These rates reflect a risk-adjusted spread that accounts for the short-term nature of the capital and the speed of execution. Institutional lenders calibrate these figures based on the asset’s specific risk profile and the sponsor’s track record.

Can I get a bridge loan if I have a low credit score but significant equity?

You’re able to secure a bridge loan with a credit score below 650 as long as the loan-to-value ratio remains at or below 65%. Lenders prioritize the underlying collateral’s value and the viability of the project’s exit strategy over the borrower’s personal credit history. This focus on asset-based underwriting ensures that capital remains available for high-equity projects regardless of temporary fluctuations in personal financial metrics.

How fast can a bridge loan be funded compared to a traditional mortgage?

A bridge loan typically reaches funding within 10 to 21 days, while traditional commercial mortgages often require 45 to 90 days for completion. This expedited timeline is a hallmark of bridge financing, allowing investors to capitalize on time-sensitive opportunities without the delays of conventional bank bureaucracy. Our disciplined approach ensures that all due diligence is conducted with both precision and speed to meet aggressive closing deadlines.

What are the most common exit strategies for bridge financing?

The primary exit strategies involve refinancing into permanent agency debt or the outright sale of the asset once it reaches a stabilized occupancy of at least 90%. According to the 2024 Real Estate Capital Markets Report, approximately 60% of borrowers transition to long-term financing after completing value-add improvements. Other sponsors choose to sell the property to realize capital gains once the strategic business plan is fully executed.

Are bridge loans available for new construction and land development?

Bridge loans are frequently utilized to fund land acquisitions and pre-development costs for new construction projects that have reached the shovel-ready stage. Lenders typically provide up to 50% of the land’s appraised value or 75% of the total construction budget to bridge the gap until senior construction financing is secured. This capital is vital for maintaining project momentum during the critical entitlement and permitting phases of development.

What is the difference between a bridge loan and a hard money loan?

The distinction lies in the capital source and cost; bridge loans usually come from institutional funds at rates of 8% to 10%, while hard money originates from private individuals at 12% or higher. Bridge financing requires more rigorous institutional-grade reporting and analytical rigor than the relatively informal structures of hard money. While both provide speed, bridge capital offers a more sophisticated framework for long-term portfolio optimization and wealth preservation.

Is a personal guarantee required for institutional bridge financing?

Institutional bridge financing often utilizes non-recourse structures that only require “bad boy” carve-out guarantees to protect against fraud or gross negligence. These limited guarantees ensure the sponsor remains accountable for specific prohibited acts without putting their entire personal estate at risk for the loan’s performance. It’s a standard practice that aligns the interests of the lender and the borrower while maintaining a professional level of risk management.

Can bridge loans be used for commercial and multi-family acquisitions?

Bridge loans are an essential tool for acquiring commercial offices, retail centers, and multi-family properties that require significant capital improvements to reach stabilization. These loans provide the necessary liquidity to purchase assets that don’t currently meet the strict debt-service coverage ratios required by traditional banks. By executing a strategic renovation plan, investors use bridge capital to increase the asset’s value before transitioning to permanent, low-interest financing.