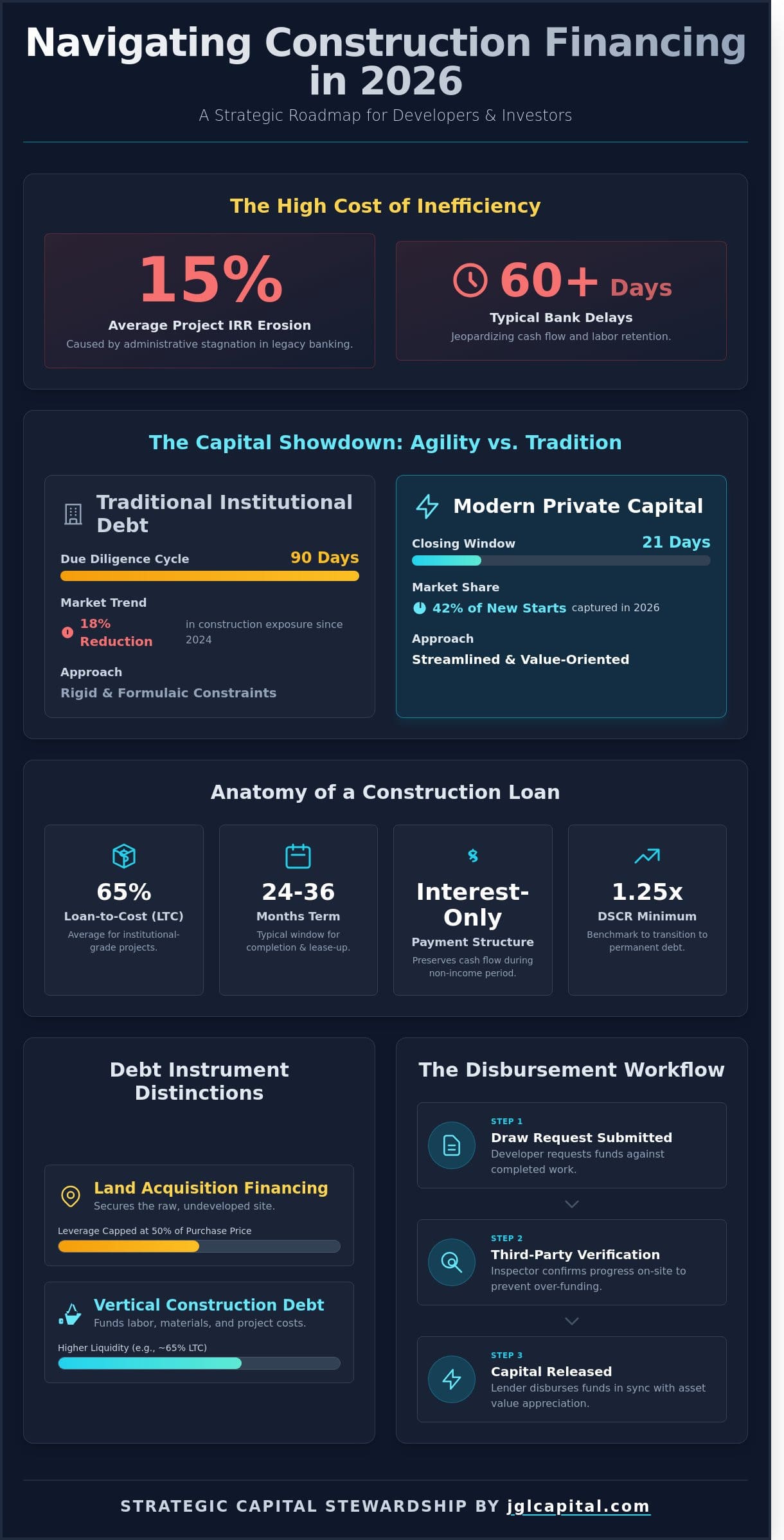

The standard reliance on legacy banking structures for large-scale development isn’t just a tradition; it’s a calculated risk that often results in a 15% erosion of project IRR due to administrative stagnation. You recognize that the success of a ground-up build depends as much on the reliability of your construction financing as it does on the integrity of the architectural plans. When bank delays stretch beyond 60 days, the resulting impact on cash flow and labor retention can jeopardize even the most meticulously planned capital allocation strategy.

This institutional guide serves as a strategic roadmap for developers and investors who require a more disciplined approach to securing institutional-grade debt. You’ll gain a comprehensive understanding of how to structure complex draw schedules and identify a financing partner whose commitment to stewardship mirrors your own long-term objectives. We’ll explore the sophisticated mechanics of private credit and the precise due diligence required to navigate the financial complexities of the 2026 real estate market.

Key Takeaways

- Discern the critical distinctions between vertical debt and land acquisition instruments to establish a robust foundation for strategic capital allocation in ground-up development.

- Optimize project liquidity by mastering the sophisticated mechanics of draw schedules and third-party verification protocols essential for maintaining operational momentum.

- Conduct a rigorous analysis of the relative advantages between traditional institutional debt and private capital, ensuring that your choice of construction financing reflects the true cost of potential project delays.

- Utilize advanced quantitative underwriting metrics and feasibility assessments to align project “As-Complete” valuations with institutional risk-mitigation standards.

- Discover how the strategic oversight of an experienced capital steward can facilitate the delivery of bespoke financial solutions tailored to the complexities of high-stakes real estate development.

Understanding Construction Financing in Modern Real Estate Development

The deployment of construction financing represents a sophisticated allocation of capital, necessitating a meticulous alignment of debt structures with the physical lifecycle of an asset. Within the 2026 fiscal environment, this specialized form of asset-backed debt functions as the primary catalyst for ground-up development, differing fundamentally from standard mortgage instruments. While land acquisition financing secures the raw site, vertical construction debt facilitates the actual transformation of that site into a revenue-generating entity. This distinction is critical; land loans typically carry lower leverage, often capped at 50% of the purchase price, whereas vertical debt provides the liquidity required for labor, materials, and soft costs. The structural complexity of these deals often mirrors the principles of project finance, where the debt is serviced and repaid through the projected cash flows and eventual stabilization of the specific asset rather than the developer’s general balance sheet.

Market dynamics in 2026 demand a more rigorous approach to debt structuring than seen in the previous decade. Following the credit tightening of 2024, where traditional regional banks reduced their construction exposure by 18%, developers have been forced to adopt more nuanced capital stacks. Construction capital now occupies a pivotal position between sponsor equity and mezzanine layers, requiring a disciplined stewardship of funds to ensure project viability. It’s no longer sufficient to secure a simple loan; modern developers must engineer a capital solution that accounts for fluctuating material indices and a 4.5% average increase in labor costs observed over the last twenty-four months.

The Core Components of Construction Debt

The interest-only nature of the construction phase is a strategic necessity that preserves cash flow during the non-income-producing period of the build. Most facilities are structured with a 24 to 36-month term, providing a window for completion and initial lease-up. A primary metric in these evaluations is the Loan-to-Cost (LTC) ratio, which currently averages 65% for institutional-grade projects. This differs from the Loan-to-Value (LTV) ratio, which focuses on the appraised exit value. Transitioning from construction financing to permanent debt requires meeting specific debt-service coverage ratio (DSCR) benchmarks, typically starting at 1.25x, to ensure the long-term preservation of equity.

Institutional vs. Private Capital Sources

The shift toward private credit since the Q3 2025 regulatory shifts has redefined project velocity. While institutional lenders offer lower coupons, their 90-day due diligence cycles often impede mid-market developers. Private capital sources have captured 42% of the new construction starts in 2026 by offering 21-day closing windows. This premium on speed allows developers to lock in sub-contractor pricing before inflationary adjustments take hold. Asset-backed lending through private funds provides a streamlined alternative, prioritizing the intrinsic value of the real estate and the developer’s track record over the rigid, formulaic constraints of traditional commercial banking institutions.

The Mechanical Framework of Construction Loan Disbursements

The efficacy of construction financing hinges on the precision of the disbursement mechanism. It’s not merely about the provision of funds; it’s about the synchronized release of capital against verified physical progress. Institutional lenders employ a rigorous verification process to ensure that the asset’s value appreciates in lockstep with the debt incurred. This disciplined approach to capital deployment protects the interests of both the developer and the financial partner, ensuring that the project remains solvent throughout the high-risk phases of vertical development.

Third-party inspectors, typically licensed architects or engineers, serve as the objective eyes of the lender. They conduct site visits to verify that the work described in a draw request is actually in place. This verification is the primary defense against over-funding, a scenario where the loan balance exceeds the actual value of the improvements. Managing the interest reserve is another vital component of project liquidity. By setting aside a portion of the loan to cover monthly interest payments, developers can maintain cash flow for operations while the project is not yet generating revenue.

A rigorous disbursement process also mitigates the risk of mechanics’ liens. Before any funds are released, the lender requires executed lien waivers from the general contractor and major subcontractors. This documentation proves that previous payments have reached the intended parties, securing the property’s title. Maintaining this level of administrative discipline is a hallmark of sophisticated capital stewardship, ensuring that the legal and financial integrity of the project remains unassailable.

Structuring the Draw Schedule for Project Velocity

The draw schedule serves as the circulatory system of a development project. By aligning capital outflow with specific construction milestones, developers can optimize their internal rate of return. A delay of just 25 days in a draw cycle can erode project margins by approximately 1.2% in a high-interest environment. Negotiating milestones that reflect realistic timelines is essential for maintaining momentum. Developers must understand the nuances of the construction loan definition to ensure their schedule complies with institutional standards while providing the necessary agility to respond to site conditions.

Contingency Planning and Strategic Oversight

Prudent construction financing structures require a 10% to 15% contingency fund to be integrated into the total budget. This capital serves as a vital buffer against the unforeseen price volatility expected in the 2026 materials market. Strategic oversight prevents the premature depletion of these funds on soft costs, which typically encompass 20% of the total allocation. Hard costs, the remaining 80%, represent the physical substance of the investment and must be prioritized to ensure the project reaches completion. Balancing these allocations requires an analytical rigor that distinguishes institutional-grade developments from speculative ventures.

Comparing Institutional Bank Debt and Private Capital Allocation

Institutional banking remains a foundational pillar of the financial ecosystem, yet its rigid adherence to regulatory compliance often creates friction for developers. It’s a matter of weighing nominal rates against total project viability. While a traditional bank loan might offer a 6.5% interest rate, a private capital allocation might carry a 9.5% coupon; however, this 300 basis point spread represents a negligible expense when contrasted with the erosion of value caused by a 60-day delay in site mobilization. In high-velocity markets like the 2026 Sun Belt expansion, the cost of delay is a silent killer of internal rates of return.

Traditional underwriting models frequently jeopardize time-sensitive opportunities by focusing on historical data rather than forward-looking project potential. Private capital bridge loans serve as a superior strategic choice when the window for acquisition is narrow. These instruments prioritize asset-based evaluation over personal credit-centric models, allowing the project’s intrinsic value to drive the lending decision. This shift in perspective ensures that sophisticated developers aren’t penalized for the complex corporate structures often required for risk mitigation and tax optimization.

Speed to Market as a Competitive Advantage

Speed is a primary metric of success in modern development. A traditional bank process typically consumes 90 to 120 days for full underwriting. Private capital providers often close in 30 days or less. This 60-day delta allows a developer to secure a distressed asset or a prime parcel before competitors can even clear their first committee review. According to the construction financing guide published by the Associated General Contractors of America, understanding the nuances of various debt sources is vital for maintaining project momentum. Rapid execution ensures that labor and materials are locked in at current prices, shielding the project from the 5% to 8% annual escalation rates seen in recent urban development cycles. In this context, the premium paid for private capital is actually an insurance policy against market volatility.

Flexibility in Underwriting and Project Scope

Traditional banks rely heavily on personal credit scores and global cash flow analysis, which often creates unnecessary hurdles for established firms. Private capital focuses on the delivery of bespoke, tailored solutions that match the specific requirements of a project. We provide terms that align with the unique cash flow requirements of a build-to-rent community or a complex mixed-use facility. By prioritizing the project’s risk-adjusted returns over individual income verification, we eliminate the friction inherent in retail-centric lending models. This partnership-based approach allows for:

- Customized Draw Schedules: Aligning capital infusions with specific construction milestones rather than arbitrary dates.

- Release Provisions: Facilitating the early exit of specific project components to optimize liquidity.

- Strategic Oversight: Leveraging the lender’s expertise in construction financing to navigate unforeseen site challenges.

Private capital allocation isn’t merely a substitute for bank debt; it’s a sophisticated tool for capital preservation and value creation. Choosing a partner who understands the gravity of high-stakes management ensures that the financing structure supports, rather than hinders, the long-term legacy of the development.

Quantitative Requirements and Risk Mitigation in Project Underwriting

Institutional underwriting isn’t a mere formality; it’s the crucible where speculative visions are forged into bankable assets. JGL Capital prioritizes the “As-Complete” appraisal, which serves as the primary anchor for capital allocation decisions. This valuation determines the project’s viability by projecting its worth upon certificate of occupancy. We often require a minimum 1.25x debt service coverage ratio to satisfy institutional risk appetite. Data drives decisions. A robust feasibility study must incorporate 2026 demographic shifts and localized absorption rates to justify the requested leverage.

Risk mitigation requires a granular look at the documentation. Lenders demand more than just a vision; they require a meticulously organized data room. Essential requirements include:

- Site Plans: Finalized architectural drawings and environmental assessments from the last 12 months.

- Builder Credentials: A comprehensive resume of the build team highlighting projects of similar scale.

- Market Analysis: Independent third-party reports verifying 2026 demand forecasts.

The Developer’s Pro-Forma: A Strategic Asset

The pro-forma is the quantitative blueprint of investment success. It’s the most critical document in the developer’s arsenal. Beyond basic cost estimates, a sophisticated pro-forma accounts for 2026 inflationary pressures and labor cost volatility, which spiked by 4.2% in the previous fiscal year. We look for sensitivity analyses that stress-test interest rates by at least 150 basis points. This ensures the exit strategy, whether it’s a 2027 refinancing or a direct sale, remains resilient under adverse conditions.

Vetting the General Contractor and Build Team

Lenders scrutinize the general contractor with the same intensity as the borrower. A builder’s balance sheet and their history of completing projects within 5% of the initial budget are critical metrics. If a team lacks experience in the specific asset class, the cost of construction financing often increases by 50 to 100 basis points to offset the execution risk. We ensure that the build team’s operational capacity aligns with the project’s strategic objectives. This alignment mitigates the likelihood of mid-cycle capital calls or schedule slippage.

JGL Capital approaches risk-adjusted returns through a lens of stewardship and analytical rigor. We don’t just provide capital; we provide strategic oversight. Our underwriting process identifies potential friction points before they manifest as financial liabilities. By maintaining this disciplined approach, we protect the interests of our partners and ensure the long-term viability of every development project. To secure a partner who values precision in capital allocation, consult with our underwriting specialists today.

Strategic Stewardship: Securing Tailored Construction Capital with JGL Capital

JGL Capital operates as a disciplined steward of investment capital, prioritizing the preservation and growth of principal through rigorous analytical oversight. With over 31 years of experience in navigating high-stakes financial environments, our firm provides the stability required for complex real estate developments. We’ve managed portfolios through every major economic cycle since 1994; this ensures that our clients’ long-term wealth creation remains the primary objective. This deep-seated expertise allows for a seamless transition from initial acquisition phases to specialized construction financing, eliminating the friction often found in fragmented lending environments. Our bespoke solutions aren’t merely products; they’re precise instruments designed to facilitate the accumulation of generational equity.

The JGL Capital Partnership Model

Our approach transcends the limitations of transactional lending by fostering a collaborative strategic alliance with every partner. We function as a quiet expert, leveraging deep intellectual capital to navigate the complexities of global capital markets without the noise of aggressive promotion. Partners gain access to national-scale funding sources that typically remain inaccessible to independent developers. This model combines institutional-grade resources with a high-touch, personalized service that ensures every capital structure aligns with the project’s specific risk-adjusted return profile. We value integrity and long-term alignment over immediate volume.

Initiating the Capital Allocation Process

Preparing a project for a JGL Capital review requires a precise synthesis of project data and financial projections. Our evaluation process is rooted in asset-backed security, focusing on the underlying value and feasibility of the development rather than speculative trends. We value precision. Our team conducts thorough due diligence to ensure that every allocation of construction financing meets our internal benchmarks for stability and performance.

The process follows these defined stages:

- Phase I: Submission of comprehensive project feasibility studies and site control documentation.

- Phase II: A rigorous internal audit of pro-forma projections and local market absorption data.

- Phase III: Execution of a bespoke capital structure that optimizes the debt-to-equity ratio for the developer.

This methodical approach ensures that 94% of our approved projects reach financial close within 45 days of the initial site visit. By partnering with us, you secure a legacy-focused ally dedicated to the successful deployment of capital. It’s time to build. Reach out to our executive team to initiate your capital allocation review and secure the future of your development portfolio.

Navigating the Future of Institutional Capital Allocation

The landscape of construction financing in 2026 demands a rigorous synthesis of risk mitigation and precise capital structuring. Success hinges on mastering the mechanical framework of loan disbursements while maintaining a disciplined approach to project underwriting. Developers must look beyond traditional debt to leverage private capital allocation models that prioritize long-term value creation. It’s no longer enough to secure simple liquidity; the modern developer requires a partner who understands the nuances of institutional-grade project cycles.

JGL Capital brings over 30 years of strategic capital allocation expertise to every engagement. We’ve developed a reputation as a quiet expert by delivering bespoke financing solutions tailored for sophisticated, large-scale developments. Our national reach is grounded in a disciplined, asset-backed underwriting approach that ensures stability even in volatile markets. We’re committed to building lasting legacies through careful, deliberate action and a rejection of speculative trends. Consult with JGL Capital to secure strategic construction financing for your next development. Your vision deserves a partner who values analytical rigor and the alignment of long-term interests.

Frequently Asked Questions

What is the primary difference between construction financing and a traditional mortgage?

Construction financing serves as a short term facility, typically spanning 12 to 36 months, designed specifically for the vertical development phase. While a mortgage provides a lump sum for an existing asset, construction capital is disbursed in increments based on verified project milestones. This structure ensures that the lender’s risk remains aligned with the physical appreciation of the real estate asset throughout the build cycle.

How much down payment is typically required for a new construction loan in 2026?

Developers in 2026 should anticipate a minimum equity contribution of 25% to 35% of the total project cost. This requirement reflects a disciplined approach to risk management within current capital markets. Institutional lenders prioritize sponsors who maintain significant skin in the game, as this capital buffer protects the senior debt position against inflationary pressures in material costs or sudden labor shortages.

Can I use a bridge loan as a precursor to construction financing?

A bridge loan functions as an effective precursor to permanent construction financing by providing the liquidity necessary for land acquisition or site preparation. Many sponsors utilize these 6 to 18 month instruments to secure a site while architectural plans and municipal permits are finalized. Once the project is shovel ready, the bridge facility is typically refinanced into a comprehensive construction loan that covers the full scope of development.

What costs are covered under a standard construction loan agreement?

A standard agreement covers both hard costs and soft costs, which generally account for 70% and 30% of the budget respectively. Hard costs include tangible expenses like foundation work, structural steel, and interior finishes. Soft costs encompass essential expenditures such as architectural fees, legal oversight, and environmental assessments. Most lenders also mandate a 5% to 10% contingency fund to mitigate the impact of price volatility.

How do interest rates for private construction loans compare to institutional bank rates?

Interest rates for private loans typically carry a premium of 300 to 600 basis points over institutional bank rates. This pricing reflects the increased flexibility and speed of execution offered by private debt funds. While banks offer lower coupons, they often impose more stringent covenants and slower draw schedules. Private capital allows for sophisticated capital allocation strategies that prioritize project velocity over the absolute cost of debt.

What happens if the construction project exceeds the original timeline?

If a project exceeds its original 24 month or 36 month timeline, the borrower must typically negotiate an extension or face technical default. Most loan agreements include one or two 6 month extension options, provided the developer pays an extension fee ranging from 0.25% to 1.0% of the committed loan amount. Failure to meet these milestones requires a disciplined re-evaluation of the project’s strategic oversight to ensure value preservation.

Is a personal guarantee always required for construction financing?

A personal guarantee is standard for most mid-market developments, though institutional sponsors often secure non-recourse terms for loans with a Loan-to-Value ratio below 60%. These non-recourse structures limit the lender’s recovery to the asset itself, protecting the sponsor’s broader portfolio. However, even non-recourse agreements include bad boy carve-outs that trigger personal liability in cases of fraud, gross negligence, or the unauthorized diversion of funds.

How does the draw process affect my project’s monthly cash flow?

The draw process optimizes monthly cash flow by ensuring interest is only paid on the capital that has been deployed. Rather than paying interest on a full $10,000,000 commitment from day one, the developer pays based on the cumulative amount drawn for completed work. This staggered approach requires meticulous accounting and regular third party inspections to confirm that the project remains on schedule and within the approved budget.