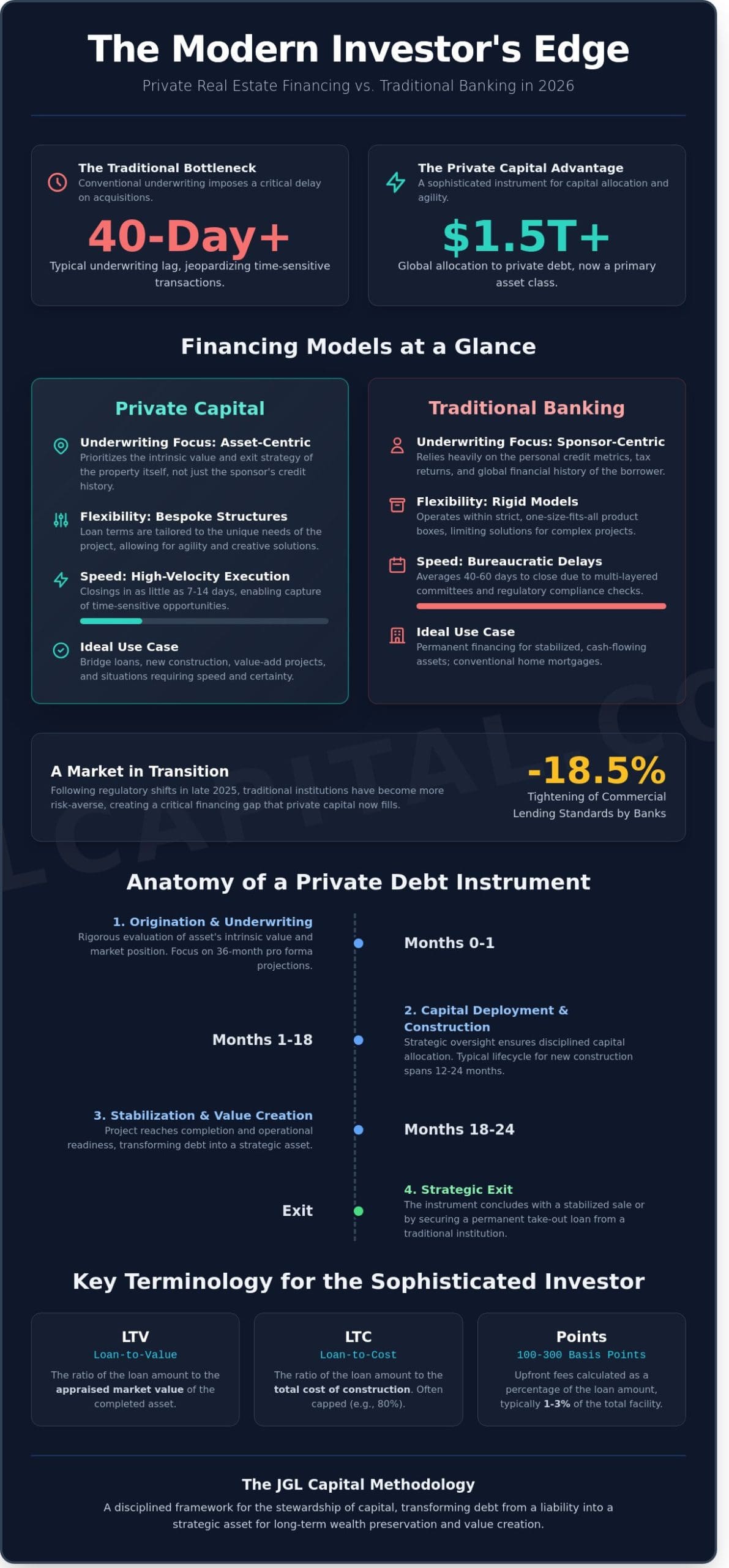

In the projected 2026 fiscal environment, the persistent reliance on traditional depository institutions for high-velocity acquisitions is no longer a sign of stability, but rather a structural vulnerability for the modern institutional investor. You’ve likely observed that the friction inherent in conventional underwriting typically results in a 40-day lag that can jeopardize time-sensitive transactions and lock up vital liquidity in long-term assets. This guide demonstrates how sophisticated principals utilize private financing for real estate loans as a high-level instrument for capital allocation and the precise optimization of risk-adjusted returns within a diversified portfolio.

We’ll examine the specific mechanics of bespoke loan structures and the strategic oversight of debt-to-equity ratios that allow for the preservation of agility when traditional capital markets contract. Precision defines every allocation. By prioritizing analytical rigor over speculative trends, you’ll discover a disciplined framework for the stewardship of capital, transforming debt from a mere liability into a strategic asset for long-term wealth preservation and value creation. This approach ensures that your capital remains deployed where it’s most effective, allowing for the seamless execution of project lifecycles without the constraints of rigid, one-size-fits-all financing models.

Key Takeaways

- Master the evolution of private debt as a sophisticated asset class and learn to differentiate institutional-grade capital from informal lending structures.

- Analyze the rigorous underwriting processes that ensure superior risk-adjusted returns throughout the lifecycle of a private real estate debt instrument.

- Discover how to leverage private financing for real estate loans to bypass the bureaucratic delays of traditional banking while maintaining institutional-level financial discipline.

- Identify precise scenarios for deploying bridge and construction capital to optimize portfolio performance and scale new development projects with agility.

- Explore the JGL Capital LLC methodology of disciplined stewardship, focusing on the alignment of interests and the delivery of bespoke, long-term financial solutions.

Table of Contents

- Defining Private Financing for Real Estate Loans in 2026

- The Structural Anatomy of Private Real Estate Debt

- Private Capital vs. Hard Money vs. Traditional Banking

- Strategic Implementation: When to Deploy Private Financing

- JGL Capital: Disciplined Stewardship in Real Estate Debt

Defining Private Financing for Real Estate Loans in 2026

As of January 2026, the global allocation toward private debt has surpassed $1.5 trillion, marking its definitive transition from a niche alternative to a primary asset class within the real estate sector. Institutional investors in Orange County now distinguish between sophisticated private capital and the fragmented, informal lending circles that characterized previous market cycles. This evolution reflects a broader maturation of the credit markets where private debt provides a necessary counterweight to the cyclical constraints of traditional banking. Understanding what is a private mortgage involves recognizing the transformation of these instruments into asset-backed securities that offer a hedge against the volatility found in public equities.

Investors are pivoting toward non-bank strategic partners because traditional depository institutions have tightened their commercial lending standards by 18.5% following the regulatory shifts of late 2025. These strategic partners operate with a level of agility that the traditional banking sector cannot replicate. They provide private financing for real estate loans that prioritize the strategic viability of a project over the bureaucratic box-ticking of legacy institutions. It’s a shift that favors speed and certainty in execution, which are the two most critical variables in the high-stakes Orange County development market.

The Core Philosophy of Asset-Based Lending

Asset-based lending prioritizes the intrinsic value of the development site rather than relying exclusively on the personal credit metrics of the sponsor. This shift toward asset-centric underwriting allows for a precise evaluation of risk-adjusted returns based on the project’s projected exit strategy. By focusing on the underlying collateral, private capital preserves critical liquidity for institutional developers. It’s a disciplined approach that ensures capital remains available even when personal balance sheets are heavily leveraged in other active projects.

Key Terminology for the Sophisticated Investor

- LTV (Loan-to-Value): The ratio of the loan amount to the appraised market value of the completed asset.

- LTC (Loan-to-Cost): The ratio of the loan amount to the total cost of construction, typically capped at 80% for new builds in Florida.

- Points: Upfront fees calculated as a percentage of the total facility, usually ranging from 100 to 300 basis points.

Private financing is a non-depository credit facility used for time-sensitive real estate acquisitions. Mastering these metrics allows developers to optimize their capital stack while ensuring that the cost of capital aligns with the project’s long-term growth objectives.

The Structural Anatomy of Private Real Estate Debt

The lifecycle of a debt instrument begins with a rigorous evaluation of the asset’s intrinsic value and its projected market position. In Orange County, where residential inventory remained 18% below historical averages throughout 2023, the path from origination to strategic exit requires a disciplined framework. Unlike traditional depository institutions that often stall during the intake phase, private financing for real estate loans prioritizes the velocity of capital without compromising on analytical safety. This lifecycle typically spans 12 to 24 months for new construction projects, concluding when the developer secures a permanent take-out loan or executes a stabilized sale.

Strategic oversight isn’t just a procedural requirement; it’s the mechanism that mitigates volatility. By maintaining a disciplined approach to capital allocation, firms ensure that every dollar deployed is backed by a clear path to liquidity. Investors often consult a guide to private lending to understand how these non-bank entities function as agile partners. Precision matters here. A well-structured loan accounts for market fluctuations and construction timelines from day one.

The Underwriting Process: Speed vs. Diligence

Internal reviews focus on 36-month pro forma projections and specific Orange County zoning ordinances. Leveraging 30 years of industry expertise allows for a streamlined due diligence phase that identifies potential roadblocks before they impact the balance sheet. It’s a balance of institutional-grade risk assessment and the rapid funding cycles required in competitive Florida markets. We don’t sacrifice depth for speed; we use experience to move faster through the data.

Capital Structures and Flexible Terms

Bespoke solutions are essential for complex new builds. These structures often include:

- Interest-only periods: Typically lasting 12 to 18 months to preserve cash flow during the vertical construction phase.

- Cross-collateralization: Utilizing equity from existing multi-family assets to enhance the loan-to-cost ratio on a new project.

- Balloon payments: Structured to coincide with the issuance of a Certificate of Occupancy.

Evaluating the impact of prepayment penalties is critical for project ROI. While some lenders impose rigid 12-month lock-outs, a collaborative strategic ally will tailor these terms to align with the developer’s exit strategy. This alignment ensures that the capital structure remains a tool for growth rather than a constraint on liquidity.

Private Capital vs. Hard Money vs. Traditional Banking

The distinction between institutional debt and professional private financing for real estate loans is frequently obscured by a misunderstanding of underlying capital structures. While traditional banks operate within the constraints of federal regulations and rigid internal credit committees, professional private capital provides a level of agility that is essential for the Orange County development landscape. Institutional lenders often require 60 to 90 days for full underwriting; this delay represents a tangible fiscal loss when a developer must secure a site within a competitive 21-day escrow window. Hard money, conversely, often functions as a purely transactional tool. These lenders typically focus on the asset’s liquidation value rather than the developer’s long-term strategic objectives, often imposing predatory points ranging from 3% to 5% of the total loan volume.

A professional private brokerage acts as a strategic ally by bridging the gap between these two extremes. This middle path prioritizes disciplined stewardship and the alignment of interests. By maintaining adherence to the ethical and operational standards established by the American Association of Private Lenders, sophisticated firms ensure that capital allocation is both transparent and predictable. This approach rejects the speculative nature of high-interest hard money in favor of structured, risk-adjusted returns that support the entire lifecycle of a new build project.

The Efficiency Gap: Why Speed is a Form of Capital

In the current Florida market, the ability to close a transaction in 14 days rather than 60 days can result in a purchase price reduction of 5% to 10%. Sellers often value the certainty of a private close over the higher, yet tenuous, offers backed by traditional bank financing. Private financing for real estate loans transforms speed into a quantifiable asset. For a $2,000,000 acquisition, securing an “all-cash” equivalent position through private debt allows a developer to bypass the appraisal contingencies that frequently derail institutional bank approvals. This efficiency enables the immediate deployment of construction crews, potentially saving $15,000 per month in carrying costs and soft-cost inflation.

Risk Profiles and Borrower Requirements

The assumption that private debt is reserved for borrowers with distressed credit is a persistent fallacy. In high-stakes development, sophisticated entities with liquid reserves exceeding $1,000,000 often choose private debt to maintain liquidity for multiple concurrent projects. While a bank may demand a 1.25 debt service coverage ratio (DSCR) and personal guarantees that encumber a borrower’s entire portfolio, private terms are typically more surgical. These bespoke solutions focus on the project’s projected 18% to 25% internal rate of return (IRR) rather than the borrower’s historical tax returns. This shift from backward-looking bureaucratic criteria to forward-looking financial engineering allows for more aggressive portfolio optimization and the preservation of personal balance sheet flexibility.

Strategic Implementation: When to Deploy Private Financing

The deployment of private financing for real estate loans requires a disciplined approach to risk-adjusted returns and capital velocity. Sophisticated developers in Orange County prioritize these instruments when the opportunity cost of traditional bank delays exceeds the higher cost of capital. In high-yield scenarios, bridge loans provide the necessary liquidity to secure land or commence site work before institutional permanent financing becomes accessible. This strategic use of debt facilitates a more aggressive acquisition pace, allowing partners to capture market appreciation in submarkets like Winter Garden or Lake Nona where inventory remains constrained.

- Capital Velocity: Using private debt allows for 30% faster closing times compared to conventional institutional lenders.

- Portfolio Scaling: Leveraging private capital enables the simultaneous management of multiple projects without exhausting traditional credit lines.

- Risk Mitigation: Short-term debt structures align with the specific milestones of the build-out phase, preventing long-term exposure to interest rate volatility during construction.

New Construction and Multi-Family Development

Private capital serves as the primary engine for funding the vertical build-out phase of residential and multi-family assets. Unlike traditional lenders that may impose rigid restrictive covenants, private structures offer the agility required to manage complex draw schedules and provide strategic oversight throughout the construction lifecycle. Investors can utilize New Construction Loans to bridge the gap between initial groundbreaking and the eventual stabilization of the asset. Maintaining a disciplined build-out timeline ensures that interest carry doesn’t erode the projected internal rate of return, which typically targets a 15% to 20% threshold for institutional-grade projects. For developers seeking to optimize their construction financing strategy, understanding the nuances of new construction loans for real estate developers can provide the competitive advantage necessary to secure superior loan-to-cost ratios while compressing approval timelines. For those managing large-scale ground-up developments, implementing a comprehensive approach to strategic construction financing ensures that draw schedules align with project milestones while maintaining the capital velocity required for successful project completion.

Refinance and Recapitalization Strategies

Optimizing a portfolio involves a systematic transition from short-term construction debt to long-term, stabilized equity positions. Cash-out refinances allow developers to extract initial capital and redeploy those funds into subsequent acquisitions, effectively compounding wealth through a repeatable cycle of value creation. The Debt Service Coverage Ratio (DSCR) remains the critical metric during this phase of portfolio optimization. A DSCR of 1.20 or higher typically signals a viable private financing candidate. By securing a 1.25x coverage ratio, an investor demonstrates the cash flow stability necessary to support a long-term rental holding strategy. When the asset reaches full occupancy, many partners choose to deleverage by refinancing private debt into traditional equity or permanent agency debt to lower their weighted average cost of capital.

Effectively managing this cycle of value creation is a core discipline, and investors focused on premier assets can further refine their strategy when they explore Real Estate Portfolio Management with specialized firms.

JGL Capital: Disciplined Stewardship in Real Estate Debt

JGL Capital operates at the intersection of rigorous analytical discipline and sophisticated capital allocation. With three decades of experience managing complex transactions, our firm provides bespoke financial solutions that transcend traditional lending models. We view every new build project in Orange County as an opportunity to apply timeless principles of integrity and fiscal stewardship. This approach ensures that your pursuit of private financing for real estate loans is supported by a foundation of stability and strategic oversight. We prioritize the alignment of interests, transforming the traditional broker-client dynamic into a collaborative partnership focused on long-term value creation and the preservation of capital.

Our commitment to transparent brokerage means every transaction is scrutinized for its ability to deliver risk-adjusted returns while maintaining the health of your broader portfolio. We don’t just facilitate debt; we engineer capital structures that provide the necessary liquidity for ambitious developments. By securing a reliable flow of capital, we enable developers to focus on project execution rather than the uncertainties of the credit markets. It’s this level of strategic oversight that distinguishes our principals as quiet experts in the field of institutional-grade debt.

The Value of a Seasoned Brokerage Partner

The 2026 real estate market demands a discreet ally capable of navigating shifting interest rate environments and evolving regulatory frameworks. JGL Capital leverages a national reach to source capital for intricate commercial developments while maintaining acute localized intelligence within the Florida market. Our brokerage model provides access to diverse liquidity pools, ensuring that even the most complex debt structures are executed with precision. This localized expertise allows us to identify nuances in the Orange County landscape that broader national lenders might overlook, providing our partners with a distinct competitive advantage.

Initiating Your Strategic Partnership

Securing institutional-grade debt requires a methodical approach to documentation and risk assessment, often involving private financing for real estate loans that align with specific risk-adjusted return profiles. Our streamlined application process is designed for efficiency, moving from initial inquiry to term sheet without unnecessary delay. Before your consultation with our principals, prepare detailed site plans, historical performance data, and a clear articulation of your portfolio’s strategic objectives. This preparation allows us to provide the most accurate assessment of your project’s viability. If you’re ready to secure the future of your development, contact JGL Capital for a tailored financing consultation to discuss your specific requirements and begin a partnership rooted in excellence.

Mastering Capital Resilience in the 2026 Credit Market

Success in the 2026 fiscal landscape demands a transition from reactive borrowing to disciplined capital stewardship. The evolution of private financing for real estate loans has redefined how institutional partners manage risk-adjusted returns and liquidity across 10-year horizons. By prioritizing asset-backed lending structures over volatile traditional banking models, investors can secure the stability required for portfolio optimization. It’s a strategy that relies on analytical rigor and a deep understanding of market cycles rather than speculative trends.

JGL Capital leverages 30+ years of industry expertise to provide the institutional-grade strategic oversight necessary for debt environments impacted by recent 2025 rate adjustments. Our role as an asset-backed lending specialist ensures that every allocation aligns with your broader investment philosophy. We’ve built a legacy on transparency and meticulous due diligence, offering bespoke solutions that traditional lenders often overlook. You’re invited to Secure Your Strategic Capital with JGL Capital and benefit from a partnership rooted in three decades of proven financial integrity. Let’s work together to build a lasting legacy through deliberate action.

Frequently Asked Questions

Is private financing for real estate loans more expensive than a bank?

Private financing for real estate loans traditionally commands a premium; interest rates often range from 8% to 12% compared to the lower yields found in institutional banking. This pricing structure reflects the expedited capital deployment and our firm’s willingness to assume complex risk profiles that traditional lenders avoid. While the cost is higher, the strategic flexibility provided allows developers to secure Orange County parcels before competitors can finalize standard bank documentation.

Can I get private financing for an owner-occupied residential property?

JGL Capital doesn’t provide financing for primary owner-occupied residences, as our mandate is strictly limited to investment and commercial purposes. We focus our capital allocation on non-owner occupied projects where the primary objective is value creation or rental income generation. By maintaining this institutional focus, we ensure that our risk-adjusted returns remain aligned with the sophisticated requirements of our capital partners and the specific regulatory frameworks of Florida.

How fast can JGL Capital fund a private real estate loan?

Our firm executes funding within a 7 to 14 day window once the initial due diligence phase concludes. This timeline is significantly more efficient than the 45 to 60 day cycles typical of traditional depository institutions. By utilizing a streamlined internal underwriting process, we provide the agility necessary for developers to capitalize on time-sensitive opportunities in the competitive Orange County construction market without the delays of a committee-based bank approval.

What property types are eligible for private financing in 2026?

Eligible assets for private financing for real estate loans in 2026 include multi-family residential units, mixed-use developments, and light industrial warehouses. We prioritize projects that demonstrate a projected debt yield of at least 10% and are situated in high-growth corridors within Central Florida. Our strategic oversight ensures that each property type fits within a diversified portfolio designed to withstand market volatility while delivering consistent performance through disciplined asset selection.

Do I need a high credit score to qualify for private real estate debt?

While we consider a minimum FICO score of 620, our underwriting focuses primarily on the intrinsic value of the real estate asset and the viability of the exit strategy. Unlike traditional lenders that rely heavily on personal credit metrics, we prioritize the project’s loan-to-value ratio, typically capped at 75%. This asset-based approach allows experienced developers with complex financial backgrounds to secure funding based on the strength of their collateral rather than personal debt history.

What is the typical duration of a private real estate bridge loan?

The typical duration for our bridge instruments ranges from 12 to 24 months, providing sufficient liquidity to cover the construction or renovation phase. These short-term facilities are designed as transitional capital, allowing sponsors to reach a stabilization point before seeking long-term institutional take-out financing. We structure these terms to align with the project’s specific milestones, ensuring that the capital remains available throughout the most critical stages of the development lifecycle.

How does JGL Capital handle the underwriting of new construction projects?

Our underwriting process involves a rigorous analysis of the construction budget, contractor track record, and the local market’s absorption rates for 2025 and 2026. We mandate a contingency reserve of at least 10% within the project budget to mitigate unforeseen inflationary pressures on materials. This disciplined approach to strategic oversight ensures that every new build project in Orange County is positioned for successful completion and subsequent refinancing or sale.

What are the common fees associated with private loan origination?

Borrowers should anticipate origination fees ranging from 1% to 3% of the total loan commitment; these are settled at the time of closing. Additional costs include a flat processing fee of 1,500 dollars and standard third-party charges for appraisals and legal documentation. These fees support the high-level partnership and bespoke service we provide, ensuring that each transaction receives the analytical rigor and professional stewardship required for sophisticated real estate investment.