The conventional paradigm of personal creditworthiness is increasingly insufficient for the sophisticated investor who seeks to manage real estate through the disciplined lens of institutional asset performance. You’ve likely discovered that the bureaucratic constraints of traditional bank red tape often serve as an artificial ceiling, preventing the rapid execution necessary to secure value in high-stakes markets. This guide provides a comprehensive framework to master the current DSCR loan requirements for rental property, ensuring you can leverage asset-based financing to scale your holdings without the burden of personal income verification.

It’s our objective to provide the analytical rigor required to navigate the May 2026 lending environment, where a Debt Service Coverage Ratio of 1.25 or higher remains the benchmark for the most favorable terms. We’ll examine the precise thresholds for credit scores and capital reserves that define institutional eligibility today. By the conclusion of this guide, you’ll possess a clear methodology for calculating property-level debt capacity and identifying a reliable capital partner for your next rental property loan or multi-family acquisition. This disciplined approach to the preservation and creation of value ensures that your portfolio growth remains limited only by the performance of the assets themselves.

Key Takeaways

- Understand the fundamental transition from borrower-centric underwriting to a property-centric model that prioritizes asset performance over personal liability.

- Identify the essential institutional DSCR loan requirements for rental property, including the FICO score thresholds and LTV constraints necessary to optimize capital preservation.

- Master the technical underwriting formula used to determine cash flow sustainability, focusing on the critical 1.20x benchmark for institutional-grade financing.

- Explore the broad spectrum of eligible assets, from standard 1-4 unit residential properties to the complex requirements of multi-family investment structures.

- Discover how strategic alliances in asset-based lending facilitate rapid execution and provide a distinct competitive edge in high-stakes real estate markets.

The Philosophy of DSCR Lending: Asset Performance vs. Personal Liability

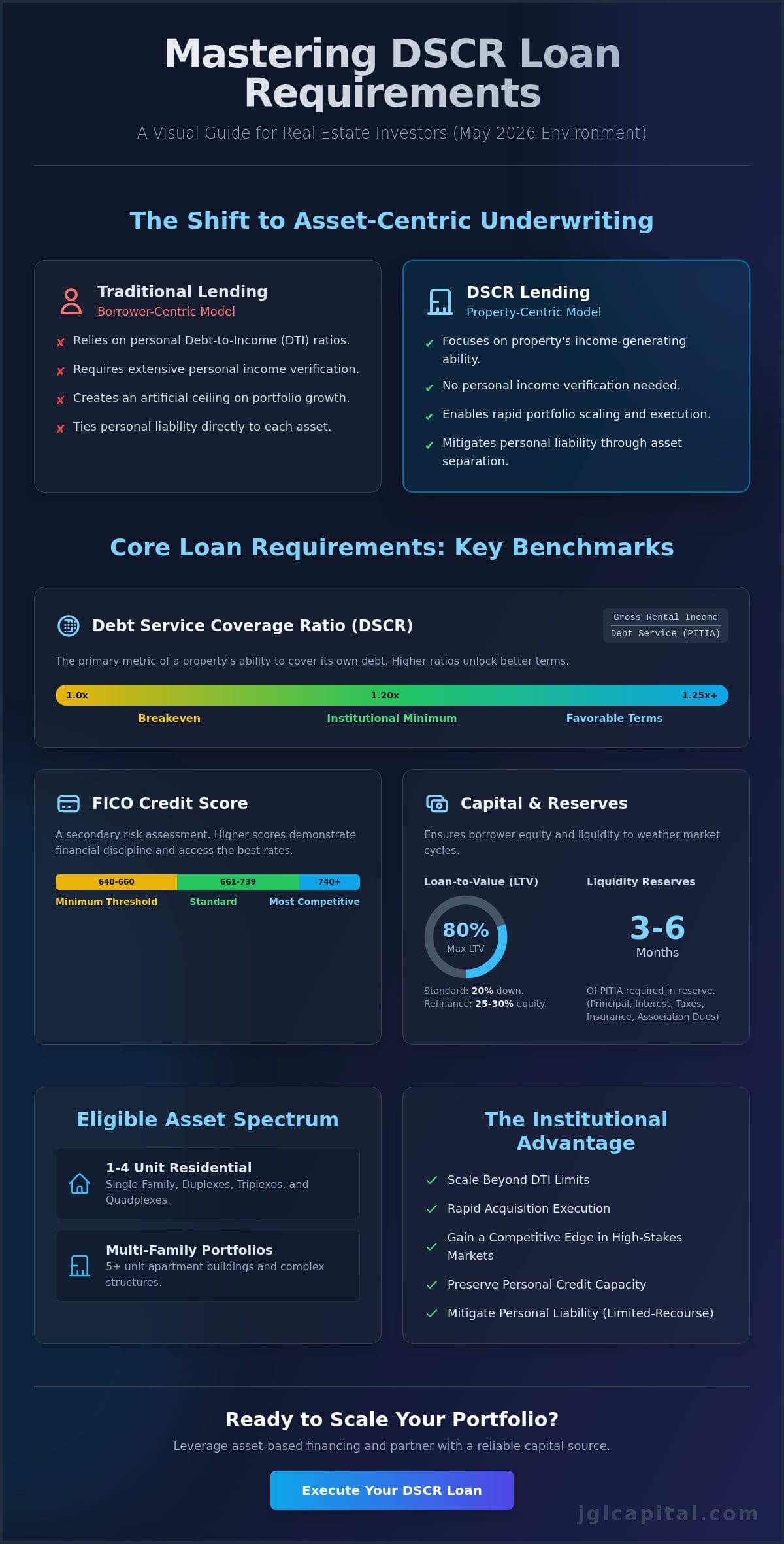

The evolution of real estate finance has necessitated a strategic departure from the restrictive frameworks of consumer lending. Sophisticated stakeholders recognize that true portfolio growth depends on the intrinsic value and income potential of the asset rather than the personal balance sheet of the individual. At its core, the Debt Service Coverage Ratio (DSCR) serves as the primary metric for assessing the long-term viability of an investment. It represents a precise calculation of cash flow sustainability, ensuring that the property generates sufficient revenue to cover its debt obligations. This fundamental shift toward property-centric underwriting allows for a more objective analysis of risk, grounding the investment in the actual performance of the real estate.

Understanding the nuanced DSCR loan requirements for rental property is essential for those who intend to build lasting legacies through real estate. By prioritizing asset performance, investors can move beyond the limitations of traditional banking, which often relies on outdated documentation standards. Private capital plays a vital role here, providing the transitional liquidity needed for rapid acquisitions in competitive markets.

The Departure from Traditional Debt-to-Income Ratios

Traditional Debt-to-Income (DTI) ratios often impose an artificial ceiling on portfolio scalability. Once a borrower reaches a specific volume of personal debt, conventional institutions often decline further credit, regardless of the profitability of the prospective acquisition. This creates a friction point for those seeking to expand their holdings. DSCR lending effectively decouples personal wealth from investment potential. It allows for the acquisition of Rental Property Loans based on the property’s capacity to sustain its own debt. This strategic separation preserves the borrower’s personal credit capacity for other high-level management needs. Many private capital structures also offer limited-recourse options, which serves to mitigate personal liability while maintaining a disciplined approach to growth.

Institutional Logic: Why Lenders Prioritize Property Income

Institutional lenders prioritize property income because it provides a more stable indicator of long-term performance than personal tax returns. In the context of high-stakes management, risk-adjusted returns are calculated through the lens of analytical rigor. Market rent volatility remains a key factor in these decisions. Therefore, a disciplined approach to asset evaluation is mandatory. Lenders scrutinize historical performance and projected rental schedules to ensure that capital is deployed responsibly. This institutional logic ensures that every strategic alliance is grounded in the preservation of value, focusing on the property’s ability to remain self-sustaining throughout varying market cycles.

Core DSCR Loan Requirements: Benchmarks for Eligibility

Securing institutional capital for real estate ventures requires meticulous adherence to established eligibility benchmarks. While the underwriting process prioritizes the asset’s income, the borrower’s financial profile serves as a secondary layer of risk mitigation. The DSCR loan requirements for rental property in the current May 2026 market are structured to balance aggressive portfolio growth with the necessity of capital preservation. Lenders typically look for a minimum credit score between 640 and 660, though a score of 740 or higher is generally required to access the most competitive interest rates. This credit depth serves as a proxy for institutional trust, signaling a disciplined history of financial management.

Capital contribution standards often mandate a minimum down payment of 20%, reflecting an 80% Loan-to-Value (LTV) ratio. For high-value acquisitions or cash-out refinances, this requirement often increases to 25% or 30% to ensure a sufficient equity cushion. Beyond the initial equity, liquidity reserves are a non-negotiable component of the approval process. Most lenders require three to six months of Principal, Interest, Taxes, Insurance, and Association dues (PITIA) to be held in cash or cash equivalents. For loan amounts exceeding $1 million, these requirements often escalate to 12 months of reserves to protect against prolonged vacancies or market contractions. Because these benchmarks vary by asset class, it’s helpful to review DSCR requirements for various loan types to understand how different structures impact your leverage options.

Credit and Capital Contribution Standards

The transparency of capital origin is a focal point for private lenders. Sourcing of funds must be clearly documented to satisfy anti-money laundering protocols and to confirm the borrower’s “skin in the game.” While purchase scenarios allow for 80% LTV, cash-out refinances are typically capped at 70% to 75%. This conservative approach ensures that the strategic alliance between the lender and the investor remains grounded in mutual security. If you’re currently evaluating a specific property’s potential, a disciplined review of rental property loans can help align your capital strategy with current market constraints.

Operational and Experience Requirements

Investor experience significantly influences underwriting flexibility. A documented history of managing similar assets can lead to more favorable LTV limits or reduced reserve requirements. This is particularly true for short-term rental (STR) properties, where lenders often require proof of historical performance or data from specialized services like AirDNA. Furthermore, most sophisticated investors choose to take title through an LLC or Special Purpose Entity (SPE). This structure provides essential asset protection and aligns with the institutional preference for treating the loan as a commercial business arrangement rather than a personal consumer obligation.

The Underwriting Formula: Calculating the Debt Service Coverage Ratio

The mathematical core of asset-based lending lies in the precision of the underwriting formula. The Debt Service Coverage Ratio (DSCR) is determined by dividing the property’s gross rental income by the total debt obligations, commonly referred to as PITIA. For those navigating the DSCR loan requirements for rental property, achieving an institutional benchmark of 1.20x or 1.25x is paramount. This ratio signifies that the asset generates 20% to 25% more income than is required to service its debt. It provides a necessary buffer against market fluctuations. While some opportunistic structures allow for “no-ratio” or “low-ratio” lending for properties with a DSCR below 1.0, these products often carry higher interest rates and require larger equity positions to offset the increased institutional risk.

Lenders don’t rely solely on existing lease agreements. They utilize a disciplined approach to verify market-rate sustainability through a Form 1007 Rent Schedule. Underwriters typically apply the lower of the actual lease amount or the appraiser’s market rent estimate. This ensures that the financing is grounded in the reality of the local submarket. It’s a method that prevents over-leveraging based on temporary market anomalies or inflated rental claims.

Nuance in Income Calculation

A sophisticated analysis of cash flow must account for more than just the mortgage payment. Professional lenders often incorporate Homeowners Association (HOA) dues and, in some instances, property management fees into the denominator of the calculation. Vacancy factors, typically ranging from 5% to 10%, are often applied to stabilize the income projection. This analytical rigor ensures the asset remains viable during tenant transitions. The role of the 1007 Rent Schedule is vital here, as it provides a neutral, third-party verification of what the property can realistically command in the current May 2026 climate.

Optimizing the Ratio for Better Terms

Improving a property’s ratio is a matter of strategic capital management. Utilizing interest-only payment structures is a common method to reduce the monthly debt obligation, which serves to increase the coverage ratio. Escrowing for taxes and insurance also provides lenders with the security of knowing these obligations are prioritized. By employing advanced real estate investing techniques, you can maximize net operating income before seeking financing. This proactive management ensures that the asset meets or exceeds the most stringent DSCR loan requirements for rental property, positioning you for more favorable interest rates and higher leverage.

Property Eligibility: From Single-Family to Multi-Family Assets

While many discussions on digital forums focus exclusively on the residential 1-4 unit sector, the institutional application of DSCR capital extends into significantly more complex asset classes. Residential properties serve as the foundational entry point, but the strategic investor often transitions into larger multi-family structures to achieve greater economies of scale. The DSCR loan requirements for rental property vary based on the specific asset type, with larger buildings requiring a shift from simple rental schedules to comprehensive commercial underwriting standards. Specialized assets, such as rural land or highly niche commercial properties, often face hurdles because their income streams lack the predictable stability required by institutional stewards. Prohibited property types typically include those that don’t produce consistent rental revenue or those with limited marketability in the event of a liquidation scenario.

Institutional grade financing is available for a variety of structures, including condominiums and planned unit developments, provided they meet specific warrantability standards. The May 2026 lending environment has seen an increased standardization in how these properties are evaluated, ensuring that the asset’s physical condition and market position align with the lender’s risk appetite. This disciplined approach to property eligibility ensures that every strategic alliance is built upon a foundation of high-quality, income-producing real estate.

Multi-Family and Commercial Nuances

Transitioning into multi-family loans for buildings with five or more units necessitates a deeper level of analytical rigor. Unlike residential 1-4 unit properties, which may rely on a Form 1007 appraisal, multi-family assets require a detailed rent roll and a Trailing 12-month (T12) operating statement to verify historical performance. This historical data allows lenders to assess the net operating income with greater precision, accounting for actual vacancy rates and maintenance expenditures. For those managing a diverse portfolio, cross-collateralization strategies across multiple rooftops can provide the capital flexibility needed to execute large-scale acquisitions while maintaining a consolidated debt structure.

Short-Term Rental (STR) Considerations

The modern lending environment has become increasingly receptive to the high-yield potential of short-term rentals. Underwriting for these assets often utilizes data from specialized services like AirDNA or the property’s historical platform performance to project income. Institutional partners must account for the inherent seasonality of vacation rentals, ensuring the DSCR remains sustainable even during off-peak periods. It’s also mandatory that the property complies with all local licensing requirements, as regulatory shifts can represent a significant risk to the asset’s income-producing capacity. If you’re prepared to optimize your capital allocation across these diverse asset classes, our team provides the disciplined expertise needed to secure commercial real estate loans that align with your long-term objectives.

Strategic Alliance: Executing Your DSCR Loan with JGL Capital

Successful navigation of the current credit environment requires more than a checklist; it demands a strategic alliance with a firm that prioritizes asset performance over traditional documentation. JGL Capital approaches every transaction with a commitment to disciplined stewardship and rapid execution. We’ve designed our methodology to ensure that investors who meet the DSCR loan requirements for rental property can move with the speed necessary to secure high-value assets in competitive markets. By focusing on the intrinsic worth of the real estate, we provide a definitive competitive edge that traditional banking institutions, burdened by personal income verification protocols, simply can’t match.

The transition from application to funding is managed with a level of analytical rigor that reflects our 30 plus years of industry expertise. We understand that the professional investor values precision over speculative trends. Our process is cumulative, moving logically from the initial asset evaluation to the final allocation of capital. This methodical rhythm ensures that every strategic objective is clearly defined and every claim is qualified before the transaction reaches the closing table. It’s this serious approach to the creation and preservation of value that distinguishes our firm as a leader in the field.

A Legacy of Intellectual Capital

Our extensive history as hard money lenders Florida has fundamentally informed our national DSCR strategy. This regional expertise in one of the country’s most dynamic real estate markets has allowed us to refine our understanding of property value as the primary driver of creditworthiness. We offer highly customized solutions for high-stakes real estate management, recognizing that each project requires an individual approach to the preservation of value. As a seasoned and discreet partner, JGL Capital relies on its intellectual capital to navigate complex deal structures that more transactional competitors might overlook. We’ve built our reputation on the delivery of worth through collaborative, long-term relationships.

Initiating the Strategic Partnership

Securing a refined quote for your rental property acquisition begins with a deliberate analysis of the asset’s cash flow potential. Once the initial benchmarks are met, the project enters the institutional underwriting and appraisal phase. During this period, we conduct a thorough evaluation of the 1007 Rent Schedule and the property’s physical condition to ensure alignment with our high-register standards. Finalizing the allocation of capital is the culmination of a collaborative relationship designed to build lasting legacies. By framing our activities as a high-level strategic alliance, we ensure that your next project is backed by a partner deeply invested in your success. You’ll find that our steady communication rhythm mirrors our patient approach to your long-term objectives.

Capital Optimization Through Institutional Asset Stewardship

The transition from traditional personal liability to property-centric financing represents a fundamental shift in capital management. By mastering the DSCR loan requirements for rental property, investors can decouple their personal wealth from their investment potential, allowing for a more disciplined approach to portfolio growth. The institutional benchmarks detailed in this guide, such as the 1.25 coverage ratio and specific liquidity reserves, serve to protect the long-term viability of the asset while providing the flexibility required for rapid execution. Traditional institutions often don’t provide the agility required for sophisticated acquisitions, making asset-based strategies essential for high-stakes management.

Achieving these objectives requires a partner with a specialized focus on asset-backed lending and a proven history of national execution. JGL Capital brings over 30 years of industry expertise to every deal, providing the analytical rigor and intellectual capital necessary for professional developers to build lasting legacies. We invite you to Secure Your Strategic Capital Allocation with JGL Capital and initiate a partnership grounded in the preservation of value. Your commitment to asset-based performance ensures a steady path toward institutional-grade wealth.

Frequently Asked Questions

What is the minimum credit score for a DSCR loan in 2026?

The minimum credit score for institutional approval generally falls between 640 and 660 as of May 2026. While these figures represent the entry threshold, investors seeking the most competitive interest rates should maintain a score of 740 or higher. This higher credit depth provides lenders with the analytical security required to offer aggressive leverage and pricing. It reflects a disciplined history of financial management that is essential for high-stakes real estate ventures.

Can I qualify for a DSCR loan if my property is currently vacant?

You can qualify for financing even if the property is currently vacant. In such instances, lenders rely on a Form 1007 Rent Schedule, which is a specialized appraisal report that determines the fair market rent for the asset. This projection allows the underwriter to calculate a stabilized DSCR based on current submarket data rather than existing lease agreements. It’s a standard practice for new acquisitions where the previous owner’s rental history may be unavailable or irrelevant.

Do DSCR loans require personal tax returns or W2 statements?

Personal tax returns and W2 statements are not required for the qualification process. Because these are asset-based solutions, the underwriting focus remains strictly on the property’s ability to generate sufficient revenue to cover its debt obligations. This approach is particularly advantageous for self-employed investors or those with complex tax structures that might otherwise inhibit their ability to scale. It allows for a more efficient allocation of capital without the bureaucratic friction of traditional income verification.

How much of a down payment is typically required for a DSCR rental loan?

A standard down payment of 20% is typically required to satisfy the primary DSCR loan requirements for rental property. For high-value acquisitions or to access more favorable institutional pricing, a contribution of 25% to 30% is often recommended. This equity cushion aligns the interests of the investor and the capital partner, ensuring long-term stability for the asset. It’s a disciplined approach to capital preservation that remains a benchmark in the May 2026 lending environment.

Are DSCR loans available for multi-family or commercial properties?

Institutional DSCR capital is available for a wide range of assets, including multi-family properties with five or more units and certain commercial structures. While the core philosophy remains the same, larger assets require a more comprehensive review of rent rolls and historical operating statements. This ensures that the debt service coverage ratio is grounded in the actual performance of the building. We provide the expertise needed to navigate these complex deal structures, ensuring your portfolio expansion remains logically sound.

What happens if my DSCR ratio is below 1.00x?

Properties with a ratio below 1.00x may still qualify through specialized “no-ratio” loan products. These programs are designed for opportunistic acquisitions where the investor expects significant rent growth or intends to implement a value-add strategy. However, these loans typically carry higher interest rates and require a larger equity contribution, often 30% or more, to offset the increased institutional risk. It’s a strategic trade-off that allows for the acquisition of assets with high future potential despite current cash flow constraints.

Can I close a DSCR loan in the name of an LLC or SPE?

Closing in the name of an LLC or Special Purpose Entity (SPE) is not only permitted but often preferred by institutional lenders. This structure provides essential asset protection for the borrower and aligns with the commercial nature of the transaction. It facilitates a professional management framework that separates personal liability from the investment’s performance. By utilizing these entities, investors can build lasting legacies while maintaining a sophisticated and discreet approach to wealth preservation.

How do interest-only options affect my DSCR loan eligibility?

Interest-only payment structures serve to reduce the monthly debt obligation, which directly increases the property’s calculated debt service coverage ratio. By excluding the principal component from the denominator, a property that might otherwise fall below the 1.20x benchmark can achieve institutional eligibility. This strategy is frequently utilized by sophisticated investors to maximize cash flow during the initial years of an acquisition. It’s a precise tool for capital optimization that allows for greater flexibility in managing high-value rental portfolios.