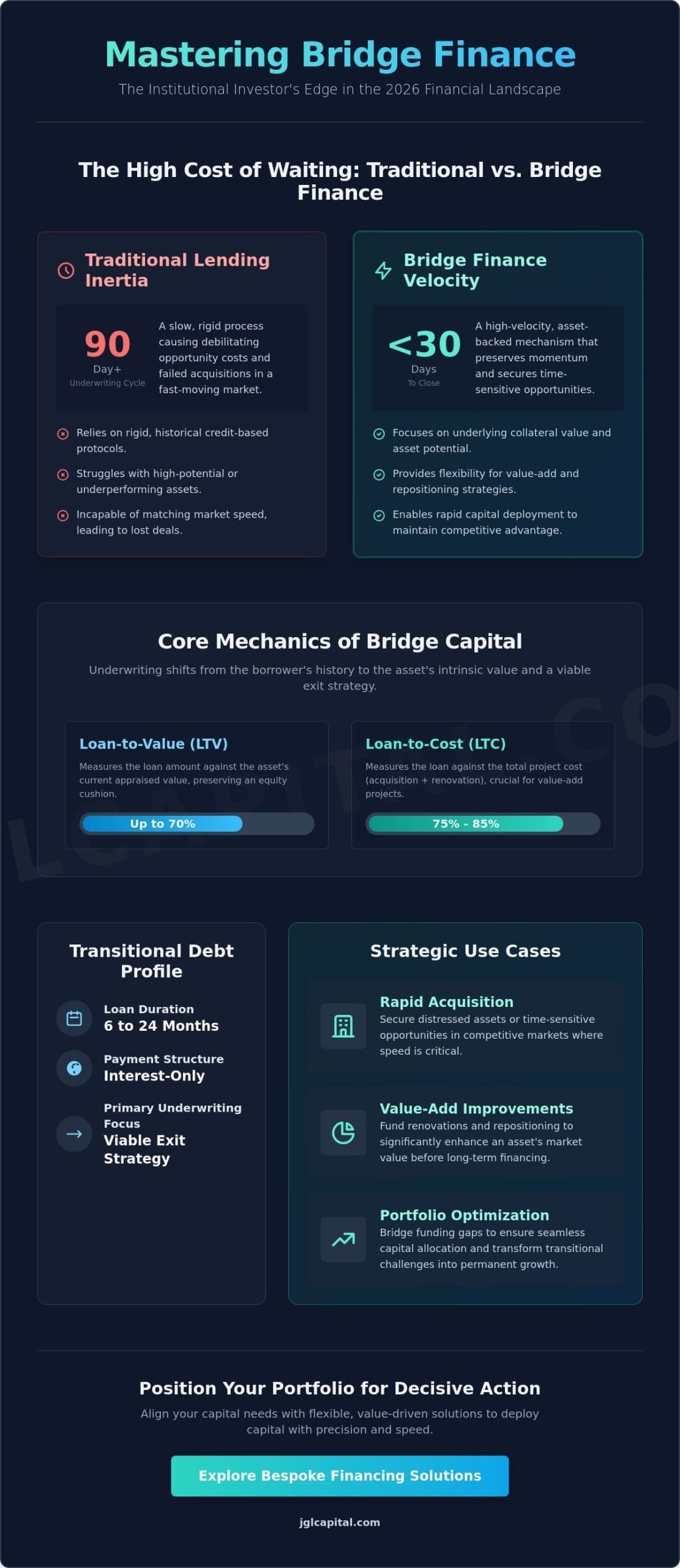

In the high-stakes financial landscape of 2026, the most significant risk to an institutional investment legacy isn’t market volatility; it’s the debilitating opportunity cost created by traditional banking inertia. You’ve likely seen a prime multi-family acquisition or a strategic commercial repositioning falter because a conventional lender’s ninety-day underwriting cycle couldn’t match the speed of the market. This systemic delay is why sophisticated investors are increasingly turning to bridge finance loans to maintain their competitive advantage and ensure seamless capital allocation. We recognize that for the disciplined steward of wealth, the ability to deploy capital with precision and speed is a fundamental requirement of portfolio optimization.

You understand that rigid, credit-based protocols often fail to account for the true value of high-potential assets or the complexities of bespoke development projects. This guide will provide the analytical rigor you need to master bridge financing, offering a clear roadmap to secure rapid liquidity and transition effectively to long-term debt structures. We’ll examine the shift toward asset-centric underwriting and the strategic frameworks necessary to transform temporary gaps into permanent growth. By aligning your capital needs with flexible, value-driven solutions, you’ll be positioned to act with the confidence that only deep-seated expertise can provide.

Key Takeaways

- Comprehend the institutional function of transitional capital as a high-velocity, asset-backed mechanism designed to preserve momentum across various real estate cycles.

- Analyze the sophisticated underwriting frameworks that leverage Loan-to-Value (LTV) and Loan-to-Cost (LTC) metrics to ensure optimal risk-adjusted returns on collateral.

- Master the strategic application of bridge finance loans to navigate complex acquisition timelines and secure high-value commercial assets with precision.

- Develop a rigorous due diligence protocol for evaluating bridge lenders, prioritizing transparency in documentation and a demonstrated commitment to the alignment of interests.

- Explore how bespoke capital allocation strategies can transform transitional challenges into opportunities for disciplined portfolio optimization and long-term value creation.

Defining Bridge Finance Loans in the Institutional Landscape

In the 2026 financial environment, bridge finance loans represent a sophisticated mechanism for institutional investors to manage transitional periods within their portfolios. These short-term, asset-backed capital solutions provide the necessary liquidity to bridge the gap between an immediate funding requirement and a long-term financing event. Unlike traditional bank debt, which often relies on a borrower’s historical cash flow and rigid credit scores, private bridge lenders prioritize the underlying collateral value. This shift in underwriting focus allows for greater flexibility when dealing with properties that are currently underperforming or undergoing a change in use. Those seeking a foundational perspective on the mechanism often investigate What is a Bridge Loan? to understand how these facilities function as temporary liens against real estate.

The distinction between residential swing loans and commercial bridge facilities is fundamental to professional capital management. While swing loans typically facilitate the purchase of a new primary residence before the sale of an existing one, commercial bridge facilities are structured as complex financial tools for large-scale asset optimization. These facilities allow for the seamless execution of investment strategies that would otherwise be stalled by the lengthy approval processes of conventional lenders. By focusing on the asset’s potential and the borrower’s execution capability, bridge capital ensures that momentum is maintained throughout volatile real estate cycles.

The Strategic Function of Bridge Capital

Institutional partners utilize this capital to execute rapid acquisitions in markets where 2026 demand remains high and competition is fierce. Bridge finance is a temporary debt instrument used until permanent financing is secured. This speed of execution is vital for securing distressed assets or seizing time-sensitive opportunities that require closing in fewer than 30 days. Beyond acquisition, this capital provides the essential liquidity for value-add property improvements. By funding renovations or structural changes, investors can significantly enhance an asset’s market value before seeking long-term stabilization.

Core Characteristics of Transitional Debt

The 2026 market expects bridge loan durations to range typically from 6 to 24 months, reflecting the time necessary for asset repositioning. These facilities often utilize interest-only payment structures, a design choice that preserves investor cash flow during the most capital-intensive phases of a project. Underwriting in this sector places immense weight on a clearly articulated exit strategy. Whether the plan involves a traditional refinance into a permanent mortgage or the outright sale of the improved asset, the viability of this path is the primary benchmark for risk assessment. Successful capital allocation depends on the precision of these exit forecasts. This disciplined approach ensures that every deployment of capital is backed by a logical and achievable conclusion.

The Mechanics of Bridge Capital Allocation and Underwriting

The deployment of bridge finance loans requires a sophisticated understanding of collateral-centric underwriting, where the focus shifts from the borrower’s historical balance sheet to the intrinsic value of the underlying asset. Lenders evaluate risk-adjusted returns by scrutinizing the exit strategy, ensuring that the transitional phase of the property is supported by a viable path to permanent financing or a strategic sale. Establishing a foundational bridge loan definition allows institutional partners to distinguish between open and closed structures, which is vital for managing liquidity during volatile market cycles. In the first quarter of 2026, market data indicates that sophisticated lenders are prioritizing Loan-to-Cost (LTC) ratios of 75% to 85% for value-add projects, while maintaining Loan-to-Value (LTV) caps near 70% to preserve equity cushions.

Speed serves as the primary differentiator in this sector. While traditional banking institutions often require 60 to 90 days for thorough due diligence, private capital providers execute funding in as little as 5 to 10 business days. This rapid capital injection is facilitated by private money brokers who curate bespoke capital stacks, matching specific project risks with the risk appetite of high-net-worth individuals and family offices. For those managing complex portfolios, partnering with a dedicated capital steward ensures that these tight execution windows are met without compromising analytical rigor.

Asset-Based Evaluation vs. Traditional Credit

Underwriting in the private space is fundamentally asset-based, meaning the property’s current and stabilized value serves as the primary security for the debt. Borrower credit scores, while reviewed, play a secondary role compared to the experience of the sponsor and the viability of the project. Regional experts, such as hard money lenders Florida, utilize granular local market expertise to inform national underwriting, leveraging data on absorption rates and local zoning trends to mitigate risk. This localized intelligence allows for more aggressive funding stances than a centralized, algorithm-driven bank could ever offer.

Fee Structures and Cost of Capital

The cost of bridge finance loans is structured to reflect the expedited nature and higher risk profile of short-term capital. Typical fee structures include origination points ranging from 1% to 3%, alongside interest spreads that often sit 400 to 700 basis points above the prevailing SOFR rate. Bridge loan points are typically paid at the closing of the transaction. While these costs exceed those of permanent debt, they’re justified by the opportunity cost of missed acquisitions. Investors often find that the 12% annual cost of bridge capital is negligible when compared to the 30% yield generated by securing a distressed asset before a competitor can mobilize funds.

- Capital Preservation: Strict LTV limits ensure a significant equity buffer is maintained.

- Strategic Agility: Funding within 72 to 120 hours allows for the capture of time-sensitive market inefficiencies.

- Exit Certainty: Underwriting focuses heavily on the 12-to-24-month liquidity event.

Strategic Use Cases: Acquisition, Renovation, and Development

Professional portfolio managers often encounter a liquidity mismatch when high-value opportunities arise before existing assets are liquidated. Bridge finance loans provide the necessary agility to execute acquisitions without waiting for a 120-day divestment cycle to conclude. This transitional capital is essential for maintaining portfolio momentum. In a 2025 analysis of institutional real estate transactions, approximately 18% of successful acquisitions utilized bridge debt to bypass the rigid timelines of traditional depository institutions. Speed defines modern markets. While traditional banking institutions require exhaustive documentation that can extend closing periods beyond 90 days, bridge finance loans prioritize the underlying asset’s value and the sponsor’s exit strategy.

Consider a scenario where an institutional investor identifies a distressed retail center priced 30% below market value due to a pending foreclosure. A traditional bank might reject the application because of the 45-day closing requirement. By deploying bridge capital, the investor secures the asset within 14 days, subsequently stabilizing the property before seeking long-term refinancing. This disciplined approach to capital allocation ensures that high-alpha opportunities aren’t lost to bureaucratic delays.

Commercial and Multi-Family Applications

Bridging the gap during lease-up periods is a primary function for multi-family assets. Most permanent lenders require a 90% occupancy rate maintained for at least 90 days before they’ll consider funding. Investors utilize commercial real estate loans in a bridge capacity to carry the property through this stabilization phase. This strategy is particularly effective for repositioning distressed commercial assets where significant capital expenditure is required to attract Tier-1 tenants. It’s a calculated method to increase Net Operating Income (NOI) before locking in a lower interest rate on a permanent mortgage.

Bridge Financing for New Construction

Developers frequently use bridge loans to secure land while construction permits are finalized. This prevents competitors from seizing prime locations during the lengthy municipal approval process. Once the “shovel-ready” status is achieved, the developer can seamlessly transition from land acquisition debt to new construction loans. Managing cash flow during this critical pre-development phase requires a partner who understands the nuances of horizontal development. Key benefits include:

- Interest Reserves: Many bridge structures include capitalized interest, reducing the monthly cash burden on the developer.

- Flexible Draw Schedules: Capital is deployed based on specific project milestones rather than rigid calendar dates.

- Asset Repositioning: Facilitating the conversion of obsolete industrial spaces into modern logistics hubs.

JGL Capital acts as a disciplined steward during these transitions. We value long-term growth and integrity, ensuring that every bridge solution aligns with the client’s broader strategic objectives. Our focus remains on providing bespoke capital structures that survive the volatility of shifting market cycles.

Evaluating Bridge Lenders: Due Diligence and Risk Mitigation

The selection of a counterparty for bridge finance loans requires a rigorous examination of the lender’s institutional stability and their historical performance in volatile markets. Reputable, institutional-grade lenders demonstrate transparency through exhaustive term sheets that eliminate ambiguity regarding extension options, exit fees, and interest reserves. Sophisticated borrowers prioritize lenders with a documented history of executing high-value transactions, often exceeding $25 million in capitalization, where complexity is the standard. This level of due diligence ensures that the capital provider possesses the liquidity and operational maturity to support the project through its transitional phase without the risk of mid-term funding volatility.

Transparency in closing documentation is a non-negotiable hallmark of a disciplined partner. It’s a safeguard for the borrower’s equity. When a lender provides clear, itemized fee structures and definitive timelines, it signals a commitment to the alignment of interests. You’ll want to avoid lenders who obscure “junk fees” or maintain overly aggressive default triggers that could jeopardize the asset’s long-term value preservation.

The Underwriting Process: What to Expect

Institutional underwriting demands a comprehensive suite of third-party reports, including MAI appraisals and Phase I environmental assessments, to validate the underlying asset’s value. It’s a process that rewards precision. For those new to this space, a what is a bridge loan guide provides the necessary conceptual framework to understand these stringent requirements. Lenders scrutinize the feasibility of the proposed exit strategy by analyzing current cap rates and 2026 interest rate forecasts, ensuring the project’s terminal value supports the debt obligation. They don’t just look at the asset; they look at the market’s capacity to absorb it upon completion.

Risk Management for Borrowers

Prudent capital allocation necessitates a robust secondary strategy to address potential market shifts or construction delays. If a primary exit becomes untenable, having a pre-negotiated extension or a secondary takeout commitment is vital. Because bridge finance loans are asset-backed, default carries the risk of total loss of equity. This reality makes disciplined financial planning indispensable for every stakeholder involved. Working with a broker who offers strategic oversight can bridge the gap between transactional execution and long-term portfolio optimization. They act as a seasoned partner, ensuring that the loan’s structure remains conducive to the borrower’s broader investment objectives.

The JGL Capital Advantage: Bespoke Transitional Financing

JGL Capital operates with a singular mandate of precision; we leverage more than thirty years of institutional experience to address the complexities of transitional capital. Our firm recognizes that bridge finance loans are not merely transactional tools but are essential components of a broader wealth preservation strategy. We prioritize the alignment of interests by ensuring our capital allocation mirrors the long-term objectives of our partners. This commitment to stewardship transforms the lending relationship into a collaborative effort where risk-adjusted returns are meticulously calculated. Our streamlined processing protocols are engineered for the efficiency required in 2026; they provide the speed necessary for modern acquisitions without sacrificing the depth of our due diligence. While our reach is national, spanning diverse markets across all fifty states, our approach remains focused on the granular details of every high-level financial engagement. We act as a seasoned guard for your capital, ensuring that every deployment of funds is backed by a legacy of stability and analytical excellence.

Tailored Solutions for Sophisticated Investors

Sophisticated investors require more than a standardized product; they need a capital partner capable of crafting bespoke loan programs that accommodate the specific nuances of complex real estate portfolios. JGL Capital provides a discreet environment for high-stakes transactions, protecting the privacy and strategic intent of our clientele at every stage of the process. Effective real estate investing demands an ally that understands the inherent volatility of modern market cycles. Our firm serves as this reliable ally, offering the flexibility to pivot when unique opportunities or structural challenges arise. We eliminate the friction often found in traditional institutional lending; we replace it with a disciplined framework that supports your project’s unique requirements while maintaining a focus on portfolio optimization. This bespoke approach ensures that your financing is as sophisticated as the investment it supports, allowing for seamless execution in a competitive environment.

Securing Your Next Deal with JGL Capital

The path to securing capital through JGL Capital is defined by high integrity and a rigorous analytical framework. Our submission process is straightforward yet thorough; it allows our team of experts to quickly assess the viability of your request against our strict institutional underwriting standards. We don’t rely on superficial metrics or fleeting market trends; instead, we employ deep-seated financial scrutiny to ensure your project is positioned for sustainable success. This analytical rigor provides our partners with the confidence that every deal is backed by a sound investment philosophy and a commitment to value creation. By choosing a partner that values intellectual capital as much as financial capital, you secure a firm foundation for your next acquisition. When you’re ready to execute your next strategic move, Partner with JGL Capital for your bridge financing needs and experience the difference that three decades of expertise brings to your portfolio.

Optimizing Capital Allocation for the Next Era of Real Estate

As the global market moves toward 2026, the strategic deployment of bridge finance loans remains a vital instrument for institutional investors who require immediate liquidity for time-sensitive acquisitions and complex development. Success in this environment demands a shift away from standard credit-focused metrics toward a rigorous, asset-based underwriting philosophy that prioritizes the intrinsic value of the underlying real estate. By aligning with a partner who understands the nuances of capital allocation, you’ll ensure your portfolio remains resilient while maintaining the agility needed for rapid execution across national markets.

JGL Capital provides a foundation of stability with over 30 years of institutional real estate expertise. Our team delivers bespoke, tailored capital solutions that prioritize long-term growth and professional stewardship. We’ve built a reputation for analytical rigor that goes beyond simple transactions to form lasting strategic alliances. It’s this commitment to precision that allows our partners to navigate transitional periods with absolute certainty. Secure your transitional capital with JGL Capital today and position your assets for sustainable success. Your vision for value creation deserves a disciplined financial partner.

Frequently Asked Questions

What are the typical interest rates for bridge finance loans in 2026?

In 2026, typical interest rates for bridge finance loans fluctuate between 8.5% and 12.5% based on the specific asset class and borrower profile. These rates reflect a spread of 350 to 600 basis points over the Secured Overnight Financing Rate (SOFR). While higher than permanent financing, this premium facilitates the rapid deployment of capital for opportunistic acquisitions. Our partners prioritize these instruments for their flexibility during periods of market volatility.

How long does it take to secure funding for a commercial bridge loan?

Securing a commercial bridge loan requires a timeline of 14 to 45 days from the initial application to the final disbursement of funds. This duration is significantly shorter than the 90 to 120 days often required for traditional bank financing. The expedited process allows investors to execute time-sensitive strategies without delay. Efficiency in due diligence and legal documentation ensures that transitional capital is available when market opportunities arise.

Can I use a bridge loan for a property that is currently unrented?

Investors can utilize bridge financing for properties that are currently unrented or undergoing a stabilization phase. These loans are specifically designed for value-add scenarios where a property lacks the historical cash flow required by conventional lenders. Lenders evaluate the pro forma income and the feasibility of the renovation plan. This strategic capital allocation enables the transformation of underperforming assets into stabilized, income-generating portfolios.

What is the minimum credit score required for an asset-backed bridge loan?

Most institutional lenders require a minimum credit score of 650 for bridge finance loans, though the physical collateral remains the primary underwriting focus. While traditional banks rely heavily on personal credit history, bridge lenders prioritize the loan-to-cost ratio and the exit strategy. A score below 650 doesn’t automatically disqualify a borrower if the asset demonstrates strong equity. We view credit as one metric within a broader framework of risk-adjusted returns.

How does a bridge loan differ from a traditional hard money loan?

Bridge loans differ from traditional hard money loans through their lower interest rates and more rigorous institutional underwriting standards. While hard money often carries rates exceeding 12%, bridge financing typically offers more competitive pricing for stabilized assets. Bridge lenders also focus more on the borrower’s experience and the long-term viability of the project. This distinction ensures a more disciplined approach to capital preservation compared to speculative lending.

What happens if I cannot refinance my bridge loan before the term expires?

If a borrower can’t refinance before the term expires, the lender may initiate a formal extension process or exercise default provisions. Extension options often involve a fee ranging from 0.5% to 1.0% of the principal balance. Failure to secure an exit strategy can lead to increased interest rates or foreclosure actions. Proactive communication and a well-defined secondary exit strategy are essential components of responsible stewardship in transitional finance.

Are bridge loans available for new construction projects?

Bridge loans are available for new construction projects, particularly as ground-up bridge or stretch senior debt. These instruments provide the necessary capital to move a project from the entitlement phase through to completion. In 2026, approximately 30% of transitional lending is directed toward mid-market residential and mixed-use developments. This capital allocation supports the initial phases of construction before a project qualifies for permanent take-out financing.

What are the typical loan-to-value (LTV) limits for bridge financing?

Typical loan-to-value (LTV) limits for bridge financing range from 65% to 80% of the current appraised value. For high-quality assets with significant upside, some lenders may extend the loan-to-cost (LTC) ratio to 85% to cover renovation expenses. These boundaries ensure that the lender maintains a protective equity cushion while providing the borrower with sufficient leverage. Adhering to these limits reflects a disciplined approach to portfolio optimization and risk mitigation.