In the high-velocity Florida market of 2026, the most sophisticated investors recognize that bridge capital isn’t a loan of last resort; it’s a precision instrument for securing institutional-grade assets before traditional banking even finishes its initial review. You’ve likely experienced the frustration of watching a prime multi-family acquisition or a value-add commercial opportunity slip away because a conventional lender’s underwriting pace couldn’t match the speed of the market. Securing a bridge loan for real estate investors Florida allows you to bypass these systemic delays, providing the strategic liquidity necessary to execute on high-stakes opportunities with confidence.

This guide provides a rigorous analysis of how to structure transitional capital to optimize your ROI and maintain a disciplined capital stack. We’ll examine current SOFR-based pricing benchmarks, the nuances of the 2026 regulatory environment, and the specific underwriting standards required for rapid deployment in Florida’s most competitive regions. By understanding these institutional mechanics, you can transform bridge financing from a temporary solution into a powerful tool for the creation and preservation of wealth.

Key Takeaways

- Analyze the specific quantitative benchmarks of 2026, including LTV and LTC ratios, to maintain a balanced and resilient capital stack.

- Optimize your portfolio’s cash flow by implementing interest-only payment structures during the critical asset stabilization period.

- Identify the most effective deployment strategies for a bridge loan for real estate investors Florida across multi-family, new construction, and high-velocity fix-and-flip projects.

- Accelerate your deployment of capital by mastering the documentation requirements and property-centric underwriting standards favored by institutional-grade partners.

The Role of Bridge Capital in the 2026 Florida Real Estate Landscape

In the sophisticated environment of the 2026 Florida real estate market, capital isn’t merely a commodity; it’s a strategic lever. The institutionalization of this asset class has led to a more predictable lending environment where the focus remains on the underlying property’s performance rather than the borrower’s personal debt-to-income ratios. A Bridge loan functions as an interim financing vehicle, typically secured by real estate, that allows for the immediate deployment of capital during periods of asset transition. For the modern professional, securing a bridge loan for real estate investors Florida represents a shift away from the speculative “hard money” era toward a period of rigorous, transitional finance. This evolution reflects a market that demands analytical depth and a disciplined approach to the creation of value.

Bridging the Gap: Liquidity as a Competitive Advantage

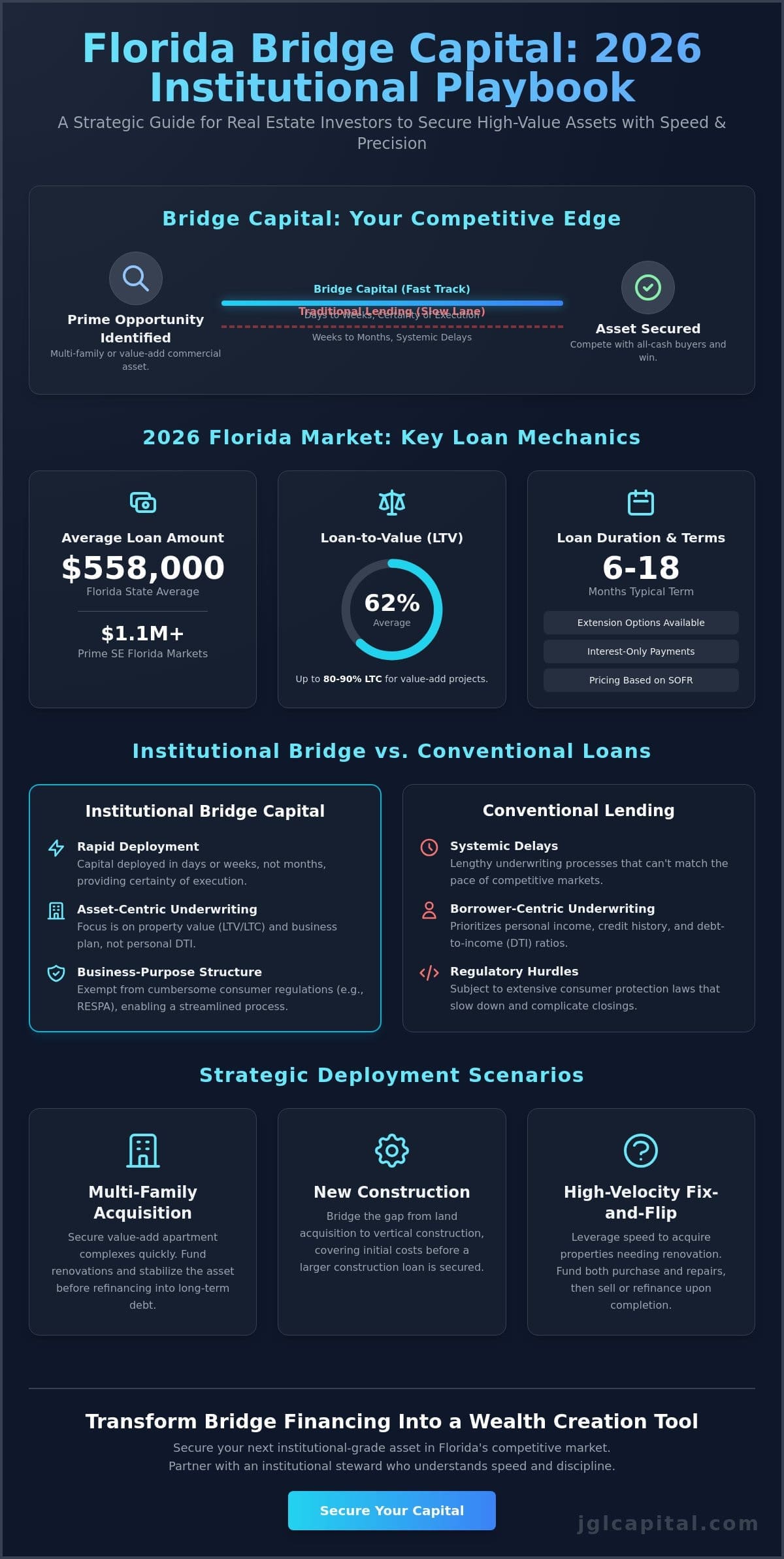

Liquidity is the primary differentiator in Florida’s high-demand corridors. As of the first quarter of 2026, the average bridge loan amount in Florida reached $558,000, while prime markets in Southeast Florida saw averages exceeding $1.1 million. These figures underscore the necessity of rapid execution. Bridge capital allows investors to compete effectively with all-cash buyers by providing certainty of execution that traditional banks cannot match. By leveraging existing property equity, you can fund new acquisitions without the need to liquidate a stabilized portfolio. It’s a strategy that preserves long-term holdings while simultaneously capturing new opportunities. Speed is no longer just a convenience; it’s an essential component of a successful bid in a landscape where acquisition windows are increasingly compressed.

Investment vs. Consumer Bridge Loans: A Critical Distinction

It’s vital to distinguish between the institutional capital intended for property investors and the consumer-grade products offered to homeowners. While many retail banks frame bridge financing as a tool for primary residences, the sophisticated investor requires a business-purpose structure. These institutional-grade loans are strictly for non-owner occupied properties, which exempts them from many of the cumbersome regulations that slow down residential mortgages. This distinction is critical for rapid deployment. By focusing on the asset’s intrinsic value and its potential for appreciation or stabilization, lenders can provide higher leverage and more flexible terms. This disciplined approach ensures that the capital stack remains optimized for maximum ROI, allowing you to focus on the strategic objectives of the investment rather than the administrative hurdles of consumer lending. Relying on an institutional steward who understands this nuance is paramount for building a lasting legacy in the Florida market.

Mechanics of Bridge Loans for Real Estate Investors in Florida

Understanding the structural mechanics of a bridge loan for real estate investors Florida requires an appreciation for asset-centric underwriting. Unlike traditional mortgages, which prioritize personal income and debt-to-income ratios, bridge financing focuses on the property’s Loan-to-Value (LTV) and Loan-to-Cost (LTC) ratios. In the first quarter of 2026, the average LTV for Florida bridge transactions was 62%, reflecting a disciplined approach to risk mitigation by institutional lenders. While institutional programs may extend up to 80% or 90% for specific value-add projects, these higher leverage points are contingent on the property’s intrinsic worth and the viability of the borrower’s business plan. These structures typically utilize the Secured Overnight Financing Rate (SOFR) as the primary benchmark for pricing, ensuring transparency and alignment with broader market shifts.

The legal framework for these transactions is distinct from consumer lending. Because these are business-purpose instruments, they fall outside the Coverage of RESPA, allowing for a more streamlined closing process. This regulatory clarity enables lenders to prioritize the property’s potential over the borrower’s individual credit metrics, though a minimum credit score of 680 remains a common benchmark for the most favorable terms. Most loan durations range from 6 to 18 months, providing sufficient time for property stabilization while offering extension options for more complex projects. This flexibility is vital for investors who need to maintain agility during the transitional phase of an asset’s lifecycle.

Asset-Based Underwriting: The Institutional Approach

Professional lenders utilize the Debt Service Coverage Ratio (DSCR) to evaluate the viability of rental-focused deals. This metric ensures the property’s projected income can comfortably cover debt obligations. Institutional lenders recognize that a bridge loan for real estate investors Florida is often the most efficient path toward long-term asset stabilization. A clear exit strategy, such as a stabilized refinance or a strategic sale, is the cornerstone of the underwriting process. Without a well-defined path to repayment, even high-equity assets may fail to meet institutional standards. Lenders conduct a rigorous review of cash reserves and documentation to ensure the project’s sustainability through its lifecycle.

Capital Stack Optimization: Points, Rates, and Fees

Optimizing the capital stack involves more than just selecting the lowest interest rate. Investors must account for origination fees, which averaged 2.1% in Florida during early 2026. Most bridge structures utilize interest-only payments to preserve cash flow during the renovation or stabilization phase. This allows capital to remain deployed in the project rather than being tied up in principal reduction. Identifying all costs, including exit fees or administrative charges, is essential for maintaining transparency. For those seeking to refine their approach to capital allocation, engaging with a disciplined investment partner can provide the necessary clarity on total cost structures and individual solutions.

Deployment Strategies: Fix-and-Flip, Multi-Family, and New Construction

The strategic deployment of a bridge loan for real estate investors Florida extends across several distinct asset classes, each requiring a tailored approach to capital allocation. While the initial phase of an investment often centers on acquisition, the subsequent phase focuses on the transition of the asset toward its highest and best use. This process relies on a lender’s ability to provide structured draws and property-centric underwriting that accounts for the intended finality of the project. Because these instruments are classified as business-purpose, they remain exempt from many federal regulations on bridge loans, such as RESPA, which facilitates the rapid movement of capital required for complex, multi-phased developments. This speed is essential for maintaining momentum in a market where delays can erode the projected internal rate of return.

Fix-and-Flip: Maximizing Velocity in Florida

For active participants in the residential market, fix and flip loans Florida provide the necessary leverage to execute high-velocity renovation projects. These structures often fund up to 100% of renovation costs through a series of structured draws, ensuring that capital is deployed in alignment with project milestones. Success in this sector depends on rapid appraisal turnarounds and a lender’s deep familiarity with local market comps. By utilizing bridge debt to secure and improve the asset, you can effectively transition to long-term rental financing once the property is stabilized, recycling capital for the next acquisition with minimal friction.

Multi-Family and Commercial Repositioning

Institutional investors frequently utilize bridge capital to acquire multi-family assets that suffer from low occupancy or significant deferred maintenance. This “Bridge-to-Perm” strategy allows for the acquisition and stabilization of an underperforming property before transitioning into a permanent, lower-interest financing structure. In these scenarios, the After-Repair Value (ARV) serves as the primary underwriting metric, allowing the lender to project the asset’s future worth once the value-add program is complete. This approach is equally applicable to commercial repositioning, where underperforming office or retail spaces are upgraded to meet current market demands, requiring a disciplined capital partner who understands the nuances of local commercial cycles.

For developers focused on ground-up projects, the bridge-to-construction model is an essential tool. Securing land and funding the initial pre-development phases through a bridge facility provides the runway needed to finalize permits and architectural plans. Once the project is “shovel-ready,” the debt can be refinanced into new construction loans. This methodical progression ensures that the capital stack remains aligned with the risk profile of each development stage, protecting your equity while maintaining project momentum. Whether you’re repositioning a multi-family complex or initiating a new build, the alignment of your financing structure with your operational timeline is the cornerstone of institutional-grade property management.

How to Secure a Real Estate Bridge Loan in Florida

Securing a bridge loan for real estate investors Florida requires a methodical approach that prioritizes the asset’s intrinsic value and the borrower’s operational history. Unlike the administrative burden associated with consumer mortgages, this institutional path requires a streamlined yet rigorous documentation package. The process begins with the formalization of a comprehensive investment proposal. This preliminary stage is followed by the engagement of a lender with specific Florida expertise, the execution of an asset-based appraisal, and the finalization of the capital structure. The culmination of this disciplined progression is the rapid funding of the escrow account. Speed is the differentiator. In a market where acquisition windows are narrow, moving from initial application to deployment in a condensed timeframe is essential for success.

The Documentation Package: What Sophisticated Lenders Require

Sophisticated lenders require an executive summary that clearly articulates the property’s specifics, the renovation budget, and a viable exit plan. In Florida, these transactions are almost exclusively conducted through business entities such as an LLC or Corporation. This structure reinforces the business-purpose nature of the capital and ensures compliance with institutional standards. A critical data point in this package is the comparison between the “as-is” value and the “as-completed” value. This allows the lender to assess the project’s feasibility and ensures that the bridge loan for real estate investors Florida provides sufficient liquidity to meet the stabilization objectives without over-leveraging the asset.

Navigating Florida-Specific Closing Logistics

Navigating the closing logistics in Florida involves understanding the state’s specific documentary stamp taxes on promissory notes. These costs must be factored into the initial capital allocation plan to ensure the accuracy of the projected ROI. It is equally important to partner with title companies that possess extensive experience in hard money lenders Florida transactions. Their familiarity with the pace and requirements of private capital ensures that the timeline from application to funding remains within the target window of 7 to 10 days. This efficiency allows professional investors to maintain their competitive edge in high-demand corridors. For those prepared to initiate a high-stakes acquisition, engaging with a senior underwriting professional is the first step toward securing the necessary capital.

JGL Capital: Institutional Stewardship in Florida Bridge Financing

JGL Capital functions as a seasoned steward in the Florida lending environment, bringing more than 30 years of history to every engagement. Our approach to a bridge loan for real estate investors Florida is defined by a rejection of speculative trends and a commitment to timeless principles of asset management. We prioritize the generation of worth through a disciplined, analytical framework, ensuring that every capital allocation aligns with the long-term strategic objectives of our partners. By specializing in complex commercial real estate loans, we provide the stability and expertise required to navigate the high-stakes landscape of property acquisition and repositioning. It’s this commitment to analytical rigor that allows us to instill confidence in our high-net-worth stakeholders.

The JGL Advantage: Speed Grounded in Expertise

Our firm recognizes that in a competitive market, speed is a function of knowledge rather than haste. By maintaining a deep understanding of Florida’s diverse sub-markets, we eliminate the bureaucratic delays that characterize traditional banking institutions. In the first quarter of 2026, our analysis of the Southeast Region revealed 320 funded bridge transactions, including 185 in Miami-Dade County alone. We leverage this granular market data to provide rapid, authoritative decisions. High-net-worth stakeholders and institutional developers benefit from direct access to decision-makers, allowing for the creation of highly customized, individual solutions that address the specific nuances of each asset. Whether you’re operating in the Panhandle, where average loan amounts reached $1,687,872 in early 2026, or the Miami metro area, our process is designed for precision and reliability. We don’t rush the analysis; we simply understand the variables better than the competition.

Partnering for Long-Term Growth

We view our role as more than just a source of capital; we’re a collaborative ally invested in the preservation of investor value. Our commitment to integrity and long-term growth means that we focus on building lasting legacies through careful, deliberate action. We don’t just fund a transaction; we support the strategic evolution of a portfolio through a bridge loan for real estate investors Florida that bridges the gap to permanent stabilization. By framing our activities as a high-level strategic alliance, we distinguish ourselves from more transactional competitors who lack our historical perspective. Our history in Florida demonstrates a consistent ability to fund acquisitions that others find too complex, moving assets from the transitional phase to successful long-term holds. We invite you to Inquire about your bridge financing requirements today to begin a relationship grounded in mutual responsibility and shared success.

Optimizing Your Capital Allocation for Florida’s High-Velocity Markets

Florida’s real estate landscape in 2026 demands a shift from transactional thinking toward high-level strategic alignment. Utilizing a bridge loan for real estate investors Florida allows you to maintain the agility required for complex acquisitions while optimizing your capital stack for maximum ROI. By prioritizing asset-centric underwriting and well-defined exit strategies, professional investors can navigate multi-family, commercial, and new construction projects with unprecedented precision. These financial instruments are the foundation for building lasting legacies in a market that rewards both speed and analytical depth.

JGL Capital provides the institutional stewardship necessary for such high-stakes management. With over 30 years of strategic real estate expertise, we offer asset-based underwriting that facilitates rapid 7 to 10 day funding. Our focus remains on delivering highly customized, institutional-grade capital solutions that support the long-term creation and preservation of worth for our partners. We invite you to align your investment objectives with a disciplined ally who values integrity and stability above all else. Your next acquisition deserves the security of a partner who understands the gravity of your vision.

Secure Strategic Bridge Capital for Your Next Florida Acquisition

Frequently Asked Questions

What is the typical interest rate for a bridge loan for real estate investors in Florida?

Interest rates for investment property bridge financing typically range between 10% and 12% as of early 2026. Market data for the first quarter of the year indicates an average rate of 10.45% across the state; however, rates in Southeast Florida have trended slightly lower at approximately 9.55%. These rates are benchmarked against the Secured Overnight Financing Rate (SOFR). They reflect the transitional nature of the capital and the speed of deployment required for competitive acquisitions.

How fast can a bridge loan be funded for a Florida investment property?

Institutional-grade bridge capital can typically be funded within 7 to 10 business days following the submission of a complete documentation package. This timeline is significantly accelerated compared to traditional banking structures because the underwriting process focuses on the property’s intrinsic value rather than extensive personal financial reviews. Rapid execution remains a primary competitive advantage for those utilizing a bridge loan for real estate investors Florida to secure high-demand assets.

Do Florida bridge lenders require a minimum credit score for investors?

Most institutional lenders in the Florida market require a minimum credit score of 680 to qualify for the most favorable terms. While the property’s value is the primary collateral, the borrower’s credit history serves as a metric for financial responsibility and management capability. Some specialized programs may consider lower scores if the project demonstrates exceptional equity or a particularly robust exit strategy; however, a 680 score remains the institutional benchmark.

Can I use a bridge loan for a new construction project in Florida?

Investors can certainly utilize bridge financing as a preliminary step for new construction projects to secure land or fund early-stage development. This capital serves as a transitional vehicle until the project reaches a shovel-ready state, at which point it’s typically refinanced into a formal construction facility. This methodical approach ensures that the capital stack remains aligned with the risk profile of each development phase while preserving equity for the build itself.

What are the typical loan-to-value (LTV) limits for Florida bridge financing?

Loan-to-Value (LTV) ratios for Florida bridge financing are generally capped between 65% and 80% for most investment properties. Market data from the first quarter of 2026 shows an average LTV of 62% across the state, reflecting a disciplined approach to risk mitigation. Certain institutional programs may provide up to 90% leverage for specific value-add or multi-family projects where the after-repair value justifies the additional capital deployment.

Are bridge loans for real estate investors in Florida considered non-recourse?

Most bridge loans for real estate investors in Florida are structured as recourse debt, meaning the borrower or a guarantor remains personally liable for the obligation. While some institutional-grade multi-family or commercial deals may offer non-recourse options for high-net-worth stakeholders, these structures often require lower leverage and higher liquidity reserves. Recourse remains the standard for disciplined capital alliances, ensuring an alignment of interests between the lender and the partner.

What happens if I cannot exit the bridge loan before the term expires?

If an investor cannot exit the loan before the term expires, the primary recourse is to exercise a pre-negotiated extension option or seek a bridge-to-permanent refinance. Most institutional contracts include provisions for extensions, provided the project remains in good standing and the interest-only payments are current. Failure to exit without an extension may result in default interest rates or the initiation of recovery procedures, making a well-defined exit strategy the cornerstone of the underwriting process.

Is an appraisal always required for a private bridge loan in Florida?

An independent, third-party appraisal is almost always required to establish the as-is and as-completed values of the subject property. Institutional lenders rely on these reports to verify the collateral’s worth and ensure the LTV remains within disciplined limits. For certain high-velocity fix-and-flip projects, a simplified Broker Price Opinion might be utilized, but a full appraisal remains the gold standard for maintaining analytical rigor in complex commercial or multi-family transactions.