The acquisition of high-value assets is rarely constrained by the availability of opportunities, but rather by the sophistication of the capital structures supporting them. Many seasoned investors recognize that the traditional banking sector’s 45-day closing cycles are increasingly incompatible with the velocity of the 2024 real estate market. You’ve likely experienced the frustration of watching a prime multi-family or commercial asset slip away while waiting for a rigid underwriting committee to approve a standard term sheet. Understanding how to find private money lenders for real estate isn’t merely about locating a source of funds; it’s about identifying a disciplined steward of capital whose investment philosophy aligns with your long-term strategic objectives.

We recognize that your priority is a streamlined capital allocation process that yields reliable, asset-backed funding without the predatory terms often found in the shadow banking sector. This guide promises to equip you with the methodologies used by institutional-grade firms to vet potential partners and secure bespoke financing for complex projects like new construction or bridge acquisitions. We’ll examine the rigorous due diligence required to move beyond transactional lending toward a model of enduring partnership and portfolio optimization.

Key Takeaways

- Distinguish between fragmented individual lenders and institutional-grade firms to ensure your capital source matches the scale and complexity of your acquisition.

- Discover how to find private money lenders for real estate by leveraging professional associations and vetted networks that prioritize disciplined stewardship over predatory lending.

- Implement rigorous due diligence protocols to verify a partner’s capital depth and historical funding performance, ensuring they possess the liquidity required for your project’s specific requirements.

- Optimize your capital acquisition strategy by constructing sophisticated loan request packages that feature comprehensive financial modeling and clear risk-adjusted return projections.

- Understand the strategic advantage of professional brokerage in accessing off-market capital and navigating the nuances of transitional bridge financing for high-stakes real estate portfolios.

The Landscape of Private Capital Allocation in Real Estate

The current environment for real estate capital allocation has undergone a fundamental transformation, moving away from the rigid structures of legacy banking toward more agile, asset-backed solutions. While many entry-level guides suggest that private capital is merely “friends and family” funding, professional investors understand that the modern landscape is dominated by institutional-grade firms. These organizations provide the liquidity necessary for large-scale acquisitions, such as multi-family developments or complex commercial re-positioning. Mastering the process of how to find private money lenders for real estate requires a shift in perspective; you must view capital not as a transactional commodity, but as a strategic alignment of interests between the borrower and the steward of capital.

Private Money vs. Traditional Bank Financing

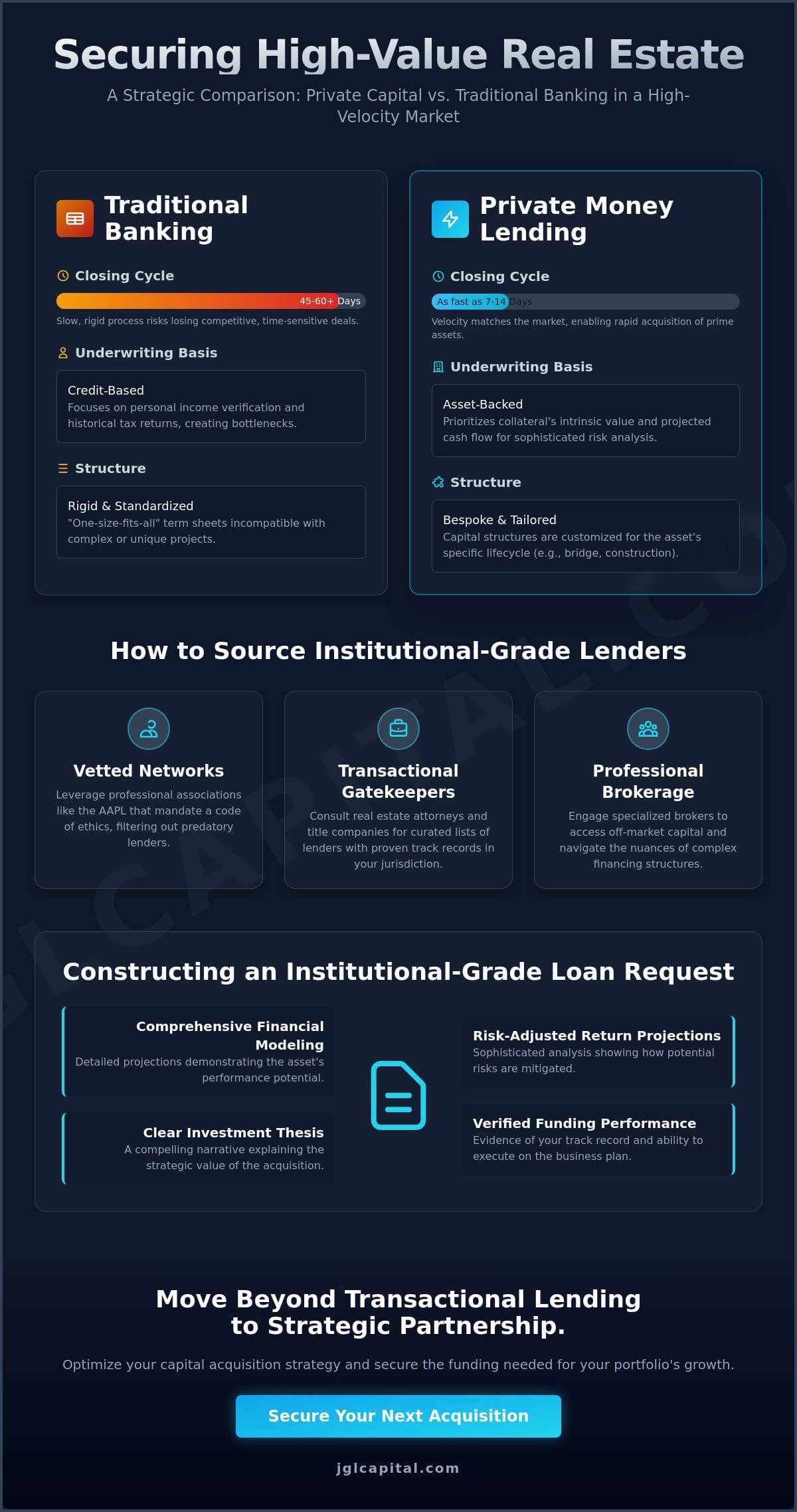

Traditional depository institutions utilize credit-based underwriting that often proves insufficient in a fast-moving market. Their reliance on personal income verification and historical tax returns creates a bottleneck that can jeopardize time-sensitive acquisitions. A 2024 report by the Mortgage Bankers Association indicated that traditional commercial loan cycles frequently exceed 60 days, a timeline that’s often fatal in competitive bidding scenarios. Asset-backed evaluation, however, prioritizes the collateral’s intrinsic value and the project’s projected cash flow. This approach allows for a more sophisticated analysis of risk-adjusted returns, providing the speed of execution required to secure high-stakes assets before they reach the open market.

The Evolution of Asset-Backed Lending in 2026

The 2026 market environment is characterized by heightened interest rate volatility and a cautious stance from regional banks. This shift has accelerated the rise of specialized bridge and construction financing, as private lenders fill the void left by retreating institutional banks. Modern private lending is now a highly regulated and professionalized sector, governed by transparent standards that protect both the investor and the capital provider. Incorporating private capital into a diversified real estate portfolio offers several advantages:

- Certainty of Execution: Private firms often provide firm commitments when banks are still in the initial due diligence phase.

- Bespoke Capital Structures: Loans are tailored to the specific lifecycle of the asset, whether it’s a land acquisition or a complex multi-family project.

- Strategic Oversight: Professional lenders act as partners, offering insights into portfolio optimization and market trends.

Success in this environment depends on your ability to articulate a clear investment thesis to these sophisticated providers. Understanding how to find private money lenders for real estate is the first step toward building a resilient, capital-ready investment vehicle that can thrive regardless of broader economic fluctuations. By focusing on asset-based evaluation rather than personal credit constraints, you position your portfolio for rapid growth and long-term stability.

Primary Channels for Sourcing Reliable Private Money Lenders

Identifying a suitable capital partner necessitates a departure from broad, unfiltered searches in favor of targeted, high-integrity channels. While digital directories offer a high volume of leads, the discerning investor prioritizes quality and institutional reliability over sheer quantity. Professional associations, such as the American Association of Private Lenders (AAPL), serve as critical vetting grounds; they mandate adherence to a code of ethics and professional standards that mitigate the risks associated with predatory lending. These organizations provide a framework for accountability that is often absent in the broader marketplace.

Transactional gatekeepers, including real estate attorneys and title companies, possess granular data regarding which capital providers are actively funding projects in specific jurisdictions. By consulting these professionals, you gain access to a curated list of lenders with proven track records of closing complex deals. This method provides a level of due diligence that’s impossible to replicate through cold outreach. It’s a strategy rooted in empirical evidence rather than marketing claims, ensuring that your search for capital is grounded in the reality of the current lending environment.

Networking Within Professional Real Estate Ecosystems

Active capital identification is most effectively achieved through the analysis of public filings and recent transaction records. Identifying lenders who’ve consistently funded multi-family or commercial acquisitions within the last 12 months provides empirical evidence of their liquidity and appetite for risk. Attending national capital summits allows for direct engagement with these institutional stewards, facilitating a deeper understanding of their investment philosophies and strategic objectives. These face-to-face interactions are essential for building the trust required for high-stakes capital allocation.

Digital Platforms and Directory Strategies

When utilizing online directories, the objective is to filter providers by specific asset classes, such as new construction or bridge financing, to ensure a precise match with your project’s needs. A lender’s digital presence often serves as a proxy for their professional stability; a firm with a robust, transparent history is more likely to provide the steady capital required for long-term growth. Integrating these sourcing methods with sophisticated real estate investing strategies ensures that your capital structure is both resilient and optimized for 2026 market conditions. Understanding how to find private money lenders for real estate through these digital channels requires a disciplined approach to data verification and reputation management.

Ultimately, the most reliable path to securing capital involves moving beyond automated lists toward established, high-level relationships. If your portfolio requires the precision and discipline of an institutional partner, consulting with a seasoned capital advisor can provide the necessary strategic oversight to navigate the complexities of modern real estate finance and ensure your acquisitions are backed by reliable, asset-based funding.

Rigorous Due Diligence: Vetting Your Private Capital Partner

The identification of a potential capital source is merely the preliminary phase of a sophisticated acquisition strategy; the subsequent vetting process determines the long-term viability of the partnership. Professional investors don’t simply accept a term sheet at face value. They conduct a comprehensive audit of the lender’s historical performance, specifically looking for a consistent track record of funding projects of similar scale and complexity. When researching how to find private money lenders for real estate, the focus must remain on institutional stability. A lender’s ability to maintain liquidity during market contractions, such as the volatility witnessed in late 2025, serves as a definitive indicator of their reliability as a strategic ally.

A rigorous transparency audit is required to ensure that your capital structure remains optimized for growth. This involves a meticulous review of the underwriting team’s professionalism and their ability to articulate risk-adjusted returns with precision. A firm that demonstrates analytical rigor during the due diligence phase is more likely to provide the steady, disciplined stewardship required for complex real estate portfolios. Evaluating their responsiveness during preliminary inquiries provides a reliable proxy for how they’ll handle time-sensitive draw requests or mid-project adjustments.

Financial Capacity and Proof of Funds

Verifying a firm’s capital depth requires more than a cursory glance at a website; it demands empirical evidence of recently closed transactions within your specific asset class. You should request a settlement statement or a list of funded projects from the previous 12 months to confirm they’re a direct lender rather than a correspondent intermediary who relies on third-party approvals. This distinction is paramount for developers seeking new construction loans, where the timely release of capital draws is essential for maintaining project momentum and avoiding costly delays.

The Ethics and Transparency Audit

A transparent fee structure is the hallmark of a disciplined capital steward. While looking at the regional standards for hard money lenders Florida and other high-growth markets, one finds that reputable firms provide clear, declarative term sheets without requesting exorbitant upfront fees. Any demand for significant capital before the issuance of a formal commitment letter should be viewed as a critical red flag. A professional underwriting team demonstrates its value through a meticulous approach to portfolio optimization, ensuring that all points, exit fees, and interest reserves are articulated without ambiguity. This clarity ensures that both parties’ interests remain aligned throughout the lifecycle of the investment.

Constructing a Sophisticated Loan Request Package

The transition from identifying a potential partner to successfully securing capital hinges on the professional presentation of the subject asset. While entry-level investors often rely on informal pitches, the institutional environment demands a comprehensive loan request package that mirrors the analytical rigor of a private equity memorandum. This package serves as the primary instrument for demonstrating the alignment of interests between the sponsor and the steward of capital. Understanding how to find private money lenders for real estate is merely the prerequisite; the subsequent challenge lies in constructing a narrative supported by empirical data and meticulous property due diligence.

A sophisticated request package should lead with a Borrower Profile that highlights historical performance and strategic oversight capabilities. Lenders prioritize sponsors who’ve navigated previous market cycles with discipline. Including environmental reports, appraisals from established firms, and a detailed schedule of real estate owned (SREO) reinforces the sponsor’s position as a seasoned professional rather than a speculative amateur. This level of preparation signals to the underwriting team that you value precision and transparency in your capital allocation process.

The Executive Summary and Pro-Forma

A robust Executive Summary provides an immediate, high-level overview of the investment thesis, detailing acquisition costs, rehab budgets, and the projected after-repair value (ARV). This document must be supported by a dynamic pro-forma that accounts for 2026 market conditions, including inflationary pressures on materials and labor. For those pursuing commercial real estate loans, the inclusion of debt-service coverage ratio (DSCR) projections and tenant credit profiles is non-negotiable. These metrics allow the lender to assess the asset’s ability to generate risk-adjusted returns throughout the hold period.

Presenting the Exit Strategy

The exit strategy is the cornerstone of any asset-based lending agreement. Lenders are primarily concerned with how their capital will be returned, whether through a transition into long-term permanent debt or a strategic asset liquidation. A credible package addresses contingency plans for construction delays or sudden shifts in the interest rate environment. By presenting a primary, secondary, and tertiary exit path, you demonstrate a commitment to capital preservation that resonates with institutional partners. If you’re ready to align your next project with a disciplined capital source, submit your loan request for a professional evaluation today.

Strategic Partnership: Why Professional Brokerage Outperforms Direct Sourcing

The final phase of a sophisticated capital strategy involves recognizing that direct sourcing, while informative, often lacks the depth and resilience of an institutional brokerage relationship. In the volatile 2026 economic environment, where traditional regional bank liquidity has contracted by approximately 18% since the previous fiscal year, the ability to access “off-market” capital becomes a critical competitive advantage. Understanding how to find private money lenders for real estate through a professional intermediary allows sponsors to tap into private credit funds and high-net-worth family offices that don’t maintain public-facing portals. These discreet capital sources often provide more flexible terms for complex acquisitions, provided the project is presented through a trusted partner who can vouch for the sponsor’s operational history.

A professional broker functions as a strategic filter, ensuring that your loan request package only reaches the desks of underwriters with a demonstrated appetite for your specific asset class. This targeted approach prevents the “shotgun” effect of multiple credit inquiries, which can inadvertently signal desperation to the market. By leveraging established institutional rapport, a broker can facilitate a more nuanced understanding of what is a bridge loan and how its transitional nature serves the long-term optimization of your portfolio. This strategic oversight is essential when navigating the compressed timelines and high stakes of 2026 real estate acquisitions.

The Broker as a Strategic Ally

The efficiency of your capital structure depends on the quality of your relationships. Professional brokers mitigate the administrative burden of managing multiple loan applications, allowing you to focus on asset management and project execution. They align borrower needs with specific lender preferences, ensuring that the capital provided is not just a loan, but a form of high-level partnership. This alignment often results in more competitive terms, including reduced points or more favorable interest reserves, which directly impact the project’s risk-adjusted returns. Established brokers provide a level of certainty that direct sourcing simply cannot match in a shifting market.

Securing Your Next Project with JGL Capital

With over 30 years of expertise in strategic capital allocation, JGL Capital operates as a disciplined steward of our partners’ interests. We reject the transactional nature of the industry in favor of building lasting legacies through careful, deliberate action. Our team provides bespoke, tailored solutions for new construction, bridge financing, and multi-family acquisitions, ensuring that every project is backed by reliable, asset-based funding. We invite you to engage with JGL Capital for your professional capital needs and experience the precision and integrity of a seasoned strategic ally.

Optimizing Your Portfolio Through Strategic Capital Alignment

Mastering how to find private money lenders for real estate is the foundational step toward achieving institutional-grade growth. By shifting from transactional searches to rigorous due diligence and sophisticated financial modeling, you ensure that your capital structure remains resilient against 2026 market fluctuations. This guide has detailed the methodologies for identifying professional stewards who value risk-adjusted returns and long-term partnership over short-term gains. The transition from a borrower to a strategic partner requires a commitment to transparency and analytical rigor that distinguishes high-stakes investors from the broader market.

JGL Capital brings over 30 years of industry expertise to your acquisition strategy, providing specialized asset-backed commercial and investment loans that bypass the inefficiencies of the traditional banking sector. Our streamlined underwriting process is designed to match the velocity of your next project, ensuring that your capital allocation is both precise and reliable. We invite you to Partner with JGL Capital for Institutional-Grade Private Funding and secure the strategic oversight your portfolio deserves. Your next acquisition represents a significant milestone in your professional legacy; we’re committed to ensuring its success through disciplined stewardship and a shared vision for value creation.

Frequently Asked Questions

How do I find a private money lender for real estate near me?

Identifying local capital providers is most effectively achieved through transactional gatekeepers, such as real estate attorneys and title companies, who maintain records of 2025 public filings. While geographic proximity was once a constraint, modern institutional firms now offer national liquidity for multi-family and commercial assets. When you’re researching how to find private money lenders for real estate, prioritizing a firm’s historical performance in your specific asset class is more critical than their physical office location.

What is a typical interest rate for a private money loan in 2026?

According to 2025 industry benchmarks from the American Association of Private Lenders, interest rates typically align with the risk profile of the asset, often ranging between 9% and 13%. These figures reflect the premium for speed and the bespoke nature of private capital allocation compared to traditional depository institutions. Rates are influenced by the project’s loan-to-value ratio and the sponsor’s track record in managing similar high-stakes acquisitions.

Can I get a private money loan with no money down?

Institutional lenders prioritize the alignment of interests, which typically necessitates a minimum sponsor equity contribution of 10% to 20% of the total project cost. “No money down” structures are generally absent from professional bridge or construction financing due to the increased risk to the capital steward. Requiring skin in the game ensures that both the borrower and the lender are committed to the project’s long-term value creation and successful exit strategy.

What documents are required to secure a private real estate loan?

Securing capital requires a comprehensive loan request package, including a detailed pro-forma, a schedule of real estate owned (SREO), and a verified primary exit strategy. You’ll also need to provide entity documentation and a clear executive summary of the subject property’s value proposition. These documents allow the underwriting team to conduct the analytical rigor required for portfolio optimization and to ensure the project meets their specific risk-adjusted return criteria.

Is private money lending legal for residential properties?

Private capital is legally utilized for residential investment properties, such as rental or fix-and-flip projects, provided the loan is strictly for a business purpose. JGL Capital does not provide owner-occupied residential mortgages, as our focus remains on high-stakes financial management for investment and commercial assets. This distinction is critical, as business-purpose loans are governed by different regulatory frameworks than consumer mortgages, allowing for greater flexibility in capital structures.

How fast can a private money lender fund a deal?

Closing timelines for private capital often range from 10 to 14 business days, significantly outperforming the 60-day cycles common in traditional banking institutions. This velocity is a primary reason why sophisticated investors research how to find private money lenders for real estate to secure time-sensitive acquisitions. A streamlined underwriting process allows for rapid capital allocation without the administrative delays associated with rigid committee-based approvals found in legacy banks.

What is the difference between a private lender and a hard money lender?

The term “private lender” encompasses a broad spectrum of non-bank capital sources, including individual investors and institutional credit funds, while “hard money” specifically refers to short-term, asset-backed debt. Institutional firms often prefer the designation of private capital partners to signal their disciplined approach to stewardship and strategic oversight. While both prioritize the collateral’s value, a professional private lender offers more sophisticated, tailored solutions for complex multi-family or commercial projects.

Do private money lenders check credit scores?

Credit scores are reviewed as a measure of a sponsor’s financial discipline and historical management of debt, but they aren’t the primary determinant in the underwriting process. The intrinsic value of the real estate asset and the viability of the projected exit strategy remain the most critical factors in the capital allocation decision. A lower score won’t necessarily result in a rejection if the project’s risk-adjusted returns and the borrower’s experience demonstrate a high probability of success.