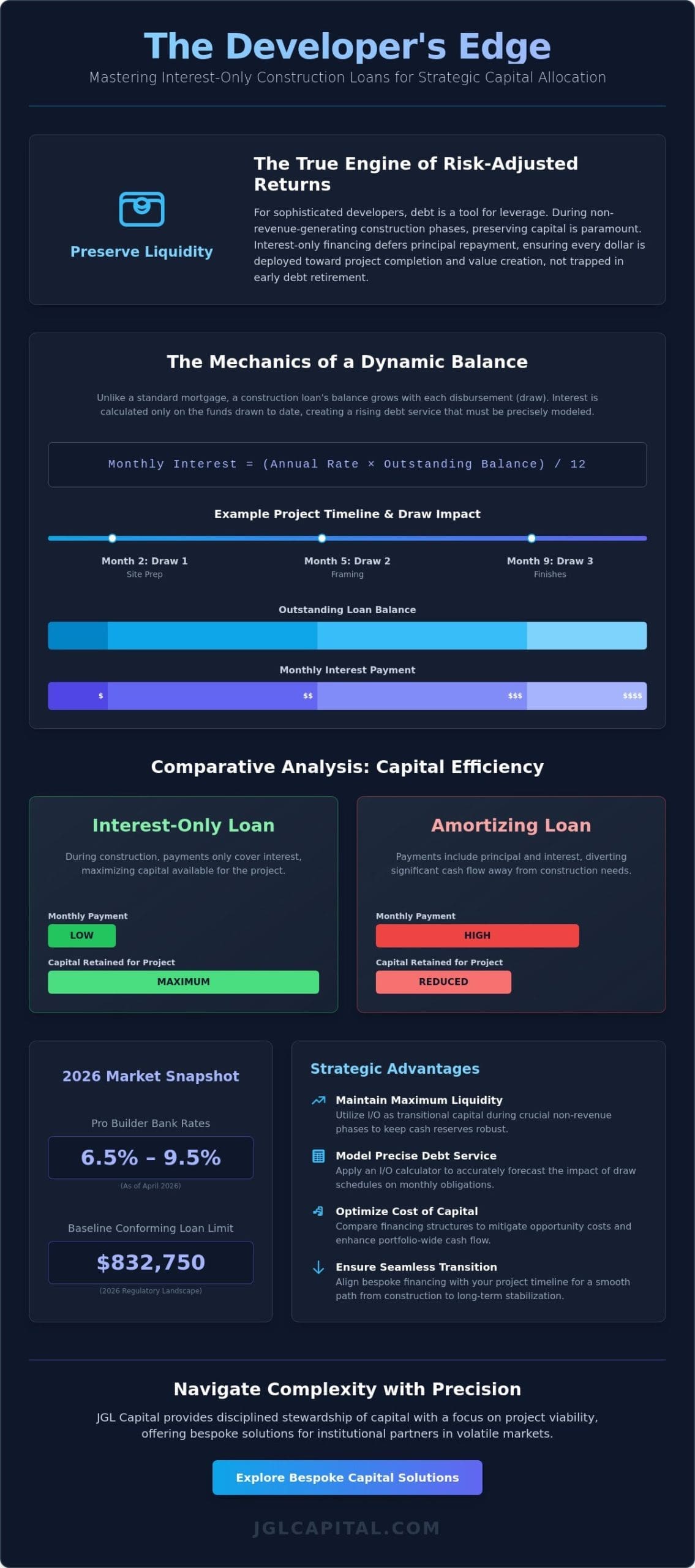

Capital allocation in the development sector is often misconstrued as a mere exercise in debt acquisition, yet the most sophisticated developers recognize that liquidity preservation is the true engine of risk-adjusted returns. When you utilize a precise interest only construction loan calculator, you move beyond simple estimation into the realm of strategic oversight. As of April 2026, with professional builder rates typically ranging from 6.5% to 9.5% for bank financing, the ability to model fluctuating draw balances becomes a critical component of institutional-grade due diligence. You understand that every basis point and every dollar of unutilized capital represents an opportunity cost that must be meticulously managed to avoid the cash flow constraints typical of non-revenue-generating phases.

You likely agree that the complexity of calculating interest on staggered disbursements often leads to conservative, yet inefficient, pro forma projections that stifle growth. This guide will empower you to master the financial mechanics of interest-only structures, ensuring you can optimize liquidity and maximize the efficiency of your private capital deployment. We will examine the current 2026 regulatory landscape, including the $832,750 baseline conforming loan limit, while providing a comprehensive framework for integrating interest-only modeling into your broader investment philosophy.

Key Takeaways

- Identify the strategic advantages of utilizing interest-only structures as transitional capital to maintain maximum liquidity during the non-revenue-generating phases of development.

- Learn to apply an interest only construction loan calculator to model the precise impact of draw schedules on your project’s monthly debt service obligations.

- Compare the total cost of capital between interest-only and amortizing debt to optimize your portfolio’s cash flow and mitigate the opportunity costs of early principal repayment.

- Discover how bespoke financing solutions can align with your project’s unique timeline to ensure a seamless transition from vertical construction to long-term stabilization.

The Strategic Role of Interest-Only Structures in Construction Financing

Interest-only construction financing represents a sophisticated form of transitional capital, specifically engineered for assets that haven’t yet reached stabilization. Unlike conventional amortizing debt, these instruments prioritize the preservation of liquidity during the high-risk vertical construction phase. For developers and commercial builders, using an interest only construction loan calculator is the first step in a broader strategy of capital allocation. By deferring principal repayment, sponsors can ensure that every dollar of equity is deployed toward project completion rather than being trapped in early debt retirement. This approach is essential for professional developers, fix-and-flip investors, and commercial builders who view debt as a tool for leverage rather than a long-term liability.

The relationship between interest-only payments and the project-level internal rate of return (IRR) is fundamental to institutional investment logic. An Interest-only loan functions as a catalyst for yield enhancement because it minimizes the cash outflow during the periods when the asset is generating zero revenue. For a professional builder facing rates between 6.5% and 9.5% in early 2026, the opportunity cost of diverting capital toward principal reduction is prohibitively high. Principal reduction during construction is often counterproductive. It effectively forces the developer to buy back equity at the same time they’re trying to leverage it for growth, which can significantly dilute the final return on investment.

The Mechanics of Capital Preservation

In the pre-revenue phase of development, maintaining a healthy debt service coverage ratio is less about current income and more about the strategic management of the interest reserve. Interest-only structures allow for the continuous reinvestment of capital into the physical asset, which accelerates the path to stabilization. Investor-grade interest-only loans differ significantly from consumer-grade mortgages because they’re built on the premise that the loan is a temporary bridge. By utilizing an interest only construction loan calculator, developers can model various draw scenarios to ensure that liquidity remains robust even if the construction timeline extends by several months.

Institutional Applications of Transitional Debt

The application of transitional debt is particularly prevalent in new construction loans, where the alignment of interests between the lender and the developer is paramount. Bridge financing serves as a stabilizing force for high-stakes assets, providing the necessary runway to reach a permanent financing event or a strategic exit. JGL Capital adopts a quiet expert approach to these volatile markets, focusing on project viability and the inherent value of the underlying asset rather than relying solely on rigid, traditional credit metrics. This disciplined stewardship of capital ensures that institutional partners can navigate the complexities of 2026’s financial landscape with precision.

Mechanical Overview: How Interest-Only Calculations Function During Construction

Precision in financial modeling is a prerequisite for successful capital allocation. While a standard interest-only mortgage loan typically maintains a static balance throughout its term, construction debt is inherently dynamic. The fundamental formula for calculating these obligations is straightforward: (Annual Interest Rate x Outstanding Balance) / 12. However, the complexity arises from the fluctuating nature of the principal balance as funds are disbursed through a structured draw schedule. Using a specialized interest only construction loan calculator allows developers to move beyond static estimates, providing a granular view of how debt service evolves as the project moves from site preparation to vertical completion.

Institutional lenders and private capital partners generally utilize simple interest rather than compounded interest for these instruments. This distinction is critical for maintaining project-level liquidity. In many sophisticated structures, an interest reserve is established at the initial closing. This reserve is often capitalized into the total loan amount, effectively allowing the interest payments to be “paid” from the loan itself during the non-revenue-generating phase. This mechanism ensures that the borrower’s out-of-pocket cash flow remains unburdened while the asset is under development. If you require a more tailored analysis of your specific capital requirements, you may find it beneficial to consult with our strategic advisory team to align your debt structure with your anticipated exit strategy.

Calculating Interest on Cumulative Draws

The calculation of interest on cumulative draws requires a methodical approach to timeline management. Rather than charging interest on the total committed loan amount, lenders only apply the rate to the capital that has actually been disbursed. To estimate these payments accurately, you must follow a logical sequence:

- Identify the projected disbursement amount for each construction milestone, such as foundation, framing, and mechanicals.

- Apply the monthly interest rate to the cumulative balance after each draw is finalized.

- Account for any “average balance” methodologies where the lender calculates interest based on the daily outstanding principal throughout the billing cycle.

Accurate timeline projections are vital. Delays in construction milestones don’t just postpone the completion date; they extend the duration of the interest-only period, potentially leading to significant interest cost overruns that can erode your contingency reserves.

The Impact of Loan-to-Cost (LTC) on Debt Service

In the context of commercial real estate loans, the Loan-to-Cost (LTC) ratio serves as a primary metric for determining the risk-adjusted interest rate. Higher leverage ratios typically correlate with increased rates, as the lender’s position in the capital stack becomes more exposed. When using an interest only construction loan calculator, sponsors must evaluate how different LTC thresholds influence the total cost of capital. A disciplined approach to the capital stack involves balancing the use of debt to maximize IRR with the necessity of maintaining sufficient equity to absorb market volatility. This strategic oversight ensures that the project remains viable even if market conditions shift during the build phase.

Comparative Analysis: Interest-Only vs. Amortizing Debt in Development

Traditional amortizing debt, while suitable for stabilized residential assets, is fundamentally misaligned with the objectives of a vertical construction phase. When you contrast a standard 30-year amortizing structure with an interest-only facility, the disparity in monthly cash requirements becomes immediately apparent. Utilizing an interest only construction loan calculator reveals that the principal component of an amortizing payment represents capital that is effectively locked into the asset prematurely. For a professional developer, this capital is better utilized as a contingency reserve or as equity for a secondary project. Unlike general consumers who build equity through monthly principal paydown, sophisticated sponsors build equity through the physical transformation of the asset and the subsequent compression of cap rates upon stabilization.

The tax implications of these structures also favor the interest-only model for commercial entities. Interest payments are typically fully deductible as a business expense, whereas principal repayments are not. This tax efficiency, combined with the preservation of liquidity, enhances the project’s overall risk-adjusted return. While the eventual balloon payment at the end of the term requires a disciplined exit strategy, the short-term benefits to the capital stack are significant. The objective isn’t to hold the debt long-term but to use it as a high-leverage tool to reach a specific valuation milestone.

Liquidity Optimization for Multi-Project Portfolios

Maintaining a high velocity of capital is essential for firms engaged in real estate investing across multiple simultaneous builds. Interest-only debt facilitates this scaling by lowering the barrier to entry for each individual project. It allows a developer to spread their equity across a broader portfolio, though this requires extreme analytical rigor to avoid over-leveraging. A disciplined steward of capital uses these tools to ensure that no single project’s debt service places a strain on the broader organization’s solvency. Choosing between interest-only and amortizing debt usually depends on the anticipated duration of the build; projects with a timeline under 24 months almost exclusively benefit from the interest-only approach.

Evaluating the Exit Strategy

A successful development cycle concludes with a seamless transition from construction financing to a permanent take-out loan or a strategic sale. For many projects in high-growth regions, transitioning to hard money lenders Florida or institutional bank financing provides the necessary liquidity to bridge the gap between certificate of occupancy and full lease-up. An interest only construction loan calculator helps in determining the necessary sale price or refinance amount by providing a clear picture of the total interest carry cost. This data ensures that the exit strategy isn’t just a hopeful projection but a calculated financial event grounded in the reality of the project’s total cost of capital.

Utilizing an Interest-Only Calculator for Portfolio Optimization

The integration of a sophisticated interest only construction loan calculator into a developer’s analytical framework provides a mechanism for the precise articulation of strategic objectives. To achieve true portfolio optimization, you must move beyond surface-level estimates and input granular variables including the total loan commitment, the anticipated interest rate, and the specific construction duration. This data doesn’t exist in isolation; it serves as a critical feed for your comprehensive pro forma spreadsheet, allowing you to determine the asset’s net cash flow requirements at every stage of the build. Sophisticated sponsors use these outputs to conduct rigorous scenario planning, ensuring that the capital stack remains resilient even if market conditions shift unexpectedly during the project’s lifecycle.

Sensitivity Analysis for Risk Management

Effective risk management requires the calculation of a worst-case debt service scenario, particularly for projects that may encounter unforeseen timeline extensions. If a build extends six months beyond its initial projection, the cumulative interest carry can significantly erode the project’s final internal rate of return. You must also evaluate the implications of floating rates versus fixed rates, as the former introduces a layer of volatility that requires a higher contingency reserve. Identifying the breakeven point where interest-only debt stops being advantageous is a hallmark of disciplined stewardship. This level of analytical rigor ensures that you’re prepared for a 1% increase in rates or other macroeconomic fluctuations that could impact your risk-adjusted returns.

Communicating with Institutional Partners

Precision in financial modeling is the currency of trust when you’re engaging with private money sources and institutional partners. Providing a transparent view of your debt service projections demonstrates a level of strategic oversight that distinguishes professional developers from speculative actors. This transparency is particularly vital when you’re seeking to secure what is a bridge loan or specialized construction capital for a high-stakes asset. Institutional partners value professional-grade modeling that accounts for every basis point and every day of the construction cycle. If you’re looking to refine your capital strategy for an upcoming project, you can evaluate our bespoke financing solutions to ensure your modeling aligns with institutional expectations and long-term value creation.

Bespoke Capital Solutions: The JGL Capital Approach to Construction Lending

JGL Capital stands as a disciplined steward of capital, leveraging over 30 years of institutional expertise to facilitate high-stakes development projects across the nation. Our methodology transcends the rigid, credit-centric models employed by traditional depository institutions, focusing instead on the intrinsic value of the asset and the long-term viability of the project. We recognize that for a professional developer, the ability to model debt service via an interest only construction loan calculator is not merely a convenience but a fundamental requirement for strategic oversight. By prioritizing the project’s pro forma and the sponsor’s track record, we deliver capital solutions that are as sophisticated as the developments they fund. Integrity defines our process.

The financial environment of April 2026 demands a partner who understands the nuance of capital allocation in a fluctuating interest rate market. While national banks may hesitate due to internal credit tightening or bureaucratic delays, JGL Capital remains a steadfast ally for high-net-worth individuals and institutional sponsors. We provide the stability of an institutional partner with the agility of a private capital specialist. This unique positioning allows us to offer terms that align with the specific cash flow requirements of complex builds, ensuring that your liquidity is preserved for maximum impact during the non-revenue-generating phases of the project lifecycle.

The Advantage of Private Money Brokerage

Our national reach and deep-seated industry relationships provide sponsors with a level of exclusivity that is unavailable through standard retail channels. In high-demand markets, the speed of execution is often the determining factor in project success, particularly when securing fix and flip loans Florida. Unlike “one-size-fits-all” bank products that often include restrictive covenants, our bespoke solutions are tailored to the unique lifecycle of each asset. We act as a collaborative partner, ensuring that the debt structure supports the physical progress of the construction phase rather than hindering it through rigid draw requirements.

Initiating Your Strategic Partnership

Securing professional-grade construction funding begins with a methodical underwriting process designed to assess the project’s risk-adjusted return potential. Sponsors are expected to provide comprehensive documentation, including detailed site plans, historical performance data, and a clear exit strategy that accounts for the eventual balloon payment. By integrating the outputs from an interest only construction loan calculator into your initial submission, you provide the analytical rigor necessary for an expedited evaluation. This transparency fosters a relationship of mutual trust and sets the stage for a lasting legacy of value creation. To begin this process, we invite you to Engage with JGL Capital for a tailored construction loan consultation.

Advancing Your Development Strategy Through Analytical Rigor

The strategic deployment of capital remains the most critical variable in the success of any high-stakes development project. By integrating an interest only construction loan calculator into your financial modeling, you ensure that your liquidity remains optimized and your risk-adjusted returns are protected against market volatility. You’ve explored how these structures act as transitional capital, allowing for the reinvestment of equity into project completion rather than premature debt retirement. This methodical approach to debt service management provides the clarity necessary to navigate complex draw schedules and execute a seamless exit strategy.

JGL Capital is prepared to serve as your collaborative partner in this endeavor. With over 30 years of industry expertise and a commitment to national strategic oversight, we operate as a premier asset-backed private money specialist. Our focus on project viability ensures that your capital stack is built for stability and long-term value creation. We invite you to Secure Institutional-Grade Construction Financing with JGL Capital today. Your next legacy project deserves the stewardship of a quiet expert and a disciplined approach to wealth preservation.

Frequently Asked Questions

How is interest calculated on a construction loan with multiple draws?

Interest is calculated solely on the outstanding principal balance that has been disbursed to the developer at any given point in time. As each milestone in the draw schedule is finalized and funds are released, the monthly obligation increases proportionally. This methodology ensures that the sponsor only pays for the capital currently at work within the project, rather than the full committed loan amount.

Can I use an interest-only calculator for a commercial renovation project?

You can absolutely utilize an interest only construction loan calculator for commercial renovation projects. These projects often mirror new construction in their need for transitional capital during the non-revenue-generating phase of improvements. The calculator helps sponsors manage the liquidity required to reach a stabilized occupancy level before transitioning to permanent financing.

What happens to the interest-only payment if the construction timeline is delayed?

If the construction timeline is delayed, the borrower remains responsible for the monthly interest payments on the total drawn balance until the loan reaches maturity or is refinanced. These extensions can significantly inflate the total carry cost of the project. This reality is why accurate timeline modeling is essential for maintaining the project’s projected internal rate of return.

Is the interest rate on an interest-only construction loan typically higher than a standard mortgage?

Interest rates for these instruments are typically 1% to 2% higher than standard residential mortgages due to the increased risk profile of non-stabilized assets. In early 2026, professional builders can expect bank rates between 6.5% and 9.5%, while specialized or higher-risk projects may see rates in the 9% to 14% range. This premium reflects the lender’s exposure during the vertical construction phase.

How does an interest reserve account work within the loan calculation?

An interest reserve account functions as a capitalized fund within the total loan amount that automatically covers the monthly debt service obligations. This mechanism prevents the need for out-of-pocket payments from the developer while the asset is under construction. It’s a strategic tool that ensures the project remains current even while it generates no revenue or income.

What is the maximum interest-only period typically offered by private money lenders?

Private money lenders typically offer interest-only periods ranging from 12 to 24 months. This duration is engineered to align with the standard vertical construction cycle or the stabilization period of a bridge loan. Some institutional partners may grant extensions if the project demonstrates continued progress and the underlying asset value remains robust.

Can an interest-only calculator help in determining my project IRR?

An interest only construction loan calculator is a vital tool for determining the project’s internal rate of return (IRR). By providing precise data on the timing and magnitude of cash outflows for debt service, the calculator allows for more accurate pro forma projections. This clarity is essential for aligning investor interests and securing institutional-grade private capital.

Do I need a separate calculator for bridge loans and construction loans?

You don’t generally require a separate calculator because the underlying financial mechanics are identical for both products. Both bridge and construction loans utilize interest-only structures to maximize borrower liquidity during transitional phases. The primary difference lies in the disbursement method, as bridge loans often involve a single lump sum while construction loans rely on a staggered draw schedule.