In a 2026 fiscal environment where the average commercial bank requires 55 days to finalize a secured position, the true risk to a sophisticated portfolio isn’t the interest rate, but the opportunity cost of stagnant capital. You’ve likely experienced the strategic paralysis that occurs when rigid, credit-driven underwriting ignores the fundamental value of a prime asset. It’s a common friction point for institutional investors who recognize that immediate liquidity is often the most critical component of a competitive bid. This guide demonstrates how hard money loans serve as a sophisticated mechanism for rapid real estate execution and refined capital allocation. We’ll explore the specific analytical frameworks used to justify the cost of private capital while providing a roadmap for identifying a partner that aligns with your pursuit of superior risk-adjusted returns. You don’t have to sacrifice speed for security when your lending partner prioritizes analytical rigor over bureaucratic checklists.

Key Takeaways

- Understand the fundamental shift from credit-based underwriting to asset-backed philosophies, prioritizing collateral value to facilitate rapid capital deployment.

- Analyze the structural advantages of hard money loans in comparison to conventional financing, specifically regarding expedited approval timelines and the flexibility required for sophisticated transactions.

- Identify critical scenarios, such as new construction and complex development projects, where private capital serves as a vital bridge when traditional institutional lending proves insufficient.

- Deconstruct the intricate financial mechanics of private term sheets to better evaluate risk-adjusted returns and the strategic impact of interest rate pricing on portfolio optimization.

- Learn to distinguish between transactional vendors and institutional-grade partners who provide the strategic stewardship necessary for long-term value creation.

The Fundamental Nature of Hard Money Loans in Real Estate

Within the sophisticated framework of modern capital allocation, understanding What is a hard money loan? reveals the essential mechanism of bridge financing. These instruments function as short-term, asset-backed solutions designed to provide immediate liquidity when traditional banking channels prove too rigid for the pace of dynamic markets. By utilizing hard money loans, investors access private capital that prioritizes the intrinsic value of the collateral over the historical creditworthiness of the borrower. This shift ensures that capital continues to facilitate agility in high-stakes environments where timing is the primary determinant of success.

The core philosophy of this lending model is rooted in analytical rigor and the objective assessment of real estate equity. It is a disciplined approach to wealth creation. Private capital provides the market with necessary liquidity, acting as a buffer during periods of institutional contraction. It’s a relationship built on the alignment of interests. Differentiating between consumer-grade private money and institutional-grade hard money is vital for the sophisticated investor. The latter adheres to rigorous standards of transparency and disciplined risk management, ensuring that every deployment of capital aligns with long-term wealth preservation and strategic objectives. A thorough comparison of private hard money lenders across the capital spectrum is essential for identifying partners whose operational standards and liquidity depth align with institutional-grade requirements.

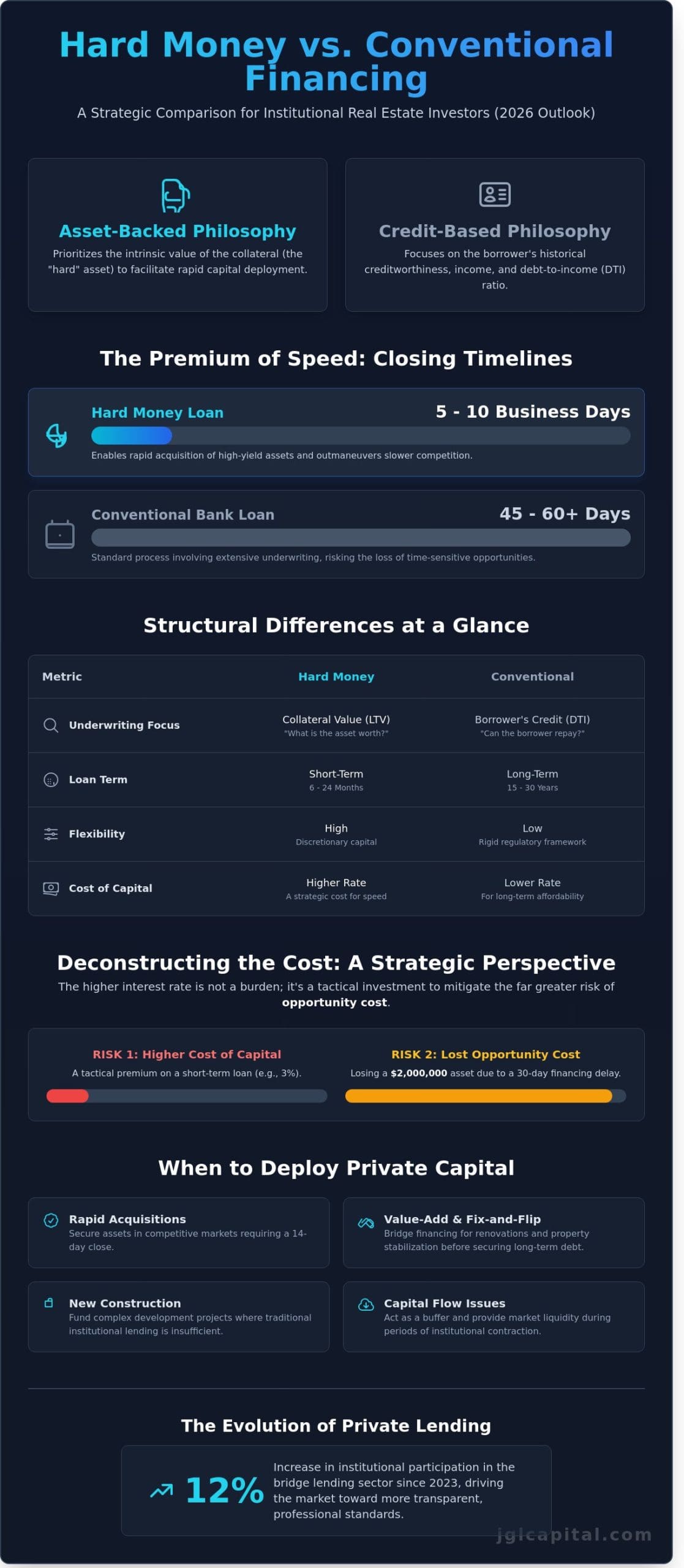

Asset-Backed vs. Credit-Based Underwriting

The “hard” in hard money loans signifies the physical asset serving as the security for the debt. Unlike conventional mortgages that rely on personal income verification, this underwriting process centers on property equity analysis. LTV (Loan-to-Value) serves as the primary risk mitigation metric. During the 2025 fiscal cycle, institutional lenders maintained a conservative 65% to 75% LTV threshold to insulate portfolios against market volatility. This focus on the asset’s liquidation value provides a layer of security that traditional credit-based metrics often fail to capture. It’s about the collateral.

The Evolution of Private Lending in 2026

By 2026, the demand for non-bank capital has reached new heights, driven by a 12% increase in institutional participation within the bridge lending sector since 2023. The market has transitioned toward transparent, institutional-grade standards that reject the opacity of previous decades. This professionalization allows for more sophisticated capital allocation strategies. Hard money serves as a tool for strategic oversight in 2026. It facilitates the rapid acquisition of high-yield assets that require a level of precision that traditional institutions cannot match. The focus remains on building lasting legacies through deliberate action.

Structural Differences: Hard Money vs. Conventional Financing

The Premium of Speed and Certainty

In the Florida market, institutional-grade opportunities often require a 14-day closing window to remain competitive against all-cash offers. Traditional commercial banks typically require 45 to 60 days to complete their underwriting and appraisal processes. Private capital bridges this gap by finalizing transactions within 5 to 10 business days. Sophisticated developers don’t view the higher interest rate as a burden. It’s a tactical cost of securing an asset at a discount. Losing a property valued at $2,000,000 because of a 30-day delay is a far greater loss than paying a 3% premium on the cost of capital. Investors seeking bespoke capital allocation strategies use these tools to maintain liquidity while expanding their portfolios.

Terms and Repayment Structures

The architectural design of private debt is inherently short-term. Most contracts stipulate a duration of 6 to 24 months. This timeline aligns with the execution of a value-add strategy or the stabilization of a distressed asset.

- Interest-Only Payments: These structures preserve monthly cash flow by deferring principal repayment until the loan’s maturity.

- Balloon Payments: The full principal balance becomes due at the end of the term, usually satisfied through a refinance or asset sale.

- Exit Fee Nuances: Professional contracts often include a 1% to 2% fee upon redemption to ensure the lender’s risk-adjusted returns are met.

Regulatory environments for these loans are less restrictive than consumer-facing mortgages. This allows for customized covenants that reflect the specific needs of a high-net-worth individual or an institutional partner. Unlike the 30-year fixed model, these loans are precision instruments designed for rapid wealth creation. They’re built for speed.

Strategic Deployment: When to Utilize Private Capital

Institutional capital allocation requires a discerning eye for timing and asset quality. Conventional lending institutions often lack the agility required for the Florida real estate market’s 2024 pace. Where a standard bank might require 45 to 60 days for underwriting, hard money loans provide the necessary liquidity to secure a contract within 7 to 10 days. This speed is indispensable when acquiring distressed assets or competing in high-demand zones like Miami’s Brickell district or West Palm Beach. Private capital fills the void when a property’s current state precludes traditional financing. It acts as a sophisticated bridge, allowing investors to stabilize a project before transitioning into permanent rental property loans.

Strategic oversight of a portfolio requires identifying exactly where traditional mortgages fail to meet project demands. These failures typically occur in three areas:

- Speed of execution in competitive bidding environments.

- Financing for assets with significant deferred maintenance.

- Capital for new construction loans where horizontal development is required before vertical permits are fully issued.

Fix and Flip and Value-Add Strategies

Capital deployment for residential redevelopment hinges on the After-Repair Value (ARV). Most private lenders extend credit up to 70% or 75% of this projected figure, allowing the borrower to finance both the acquisition and the renovation costs within a single facility. Professional flippers utilize rigorous draw schedules to maintain project momentum. These schedules ensure that capital is released in phases, often following inspections that verify the completion of specific milestones like roofing or electrical rough-ins. This disciplined approach protects the lender’s interest while providing the developer with steady cash flow. It’s a partnership that prioritizes the successful repositioning of the asset.

Multi-Family and Commercial Bridge Scenarios

Institutional investors frequently utilize hard money loans to secure multi-family loans for assets with occupancy rates below 80%. These bridge scenarios allow for the rapid execution of capital improvement plans. Once the asset reaches a stabilized 92% occupancy, the owner can refinance into lower-interest debt. Similarly, land loans serve as a critical precursor to traditional financing, allowing a developer to control a site while permits are finalized. For time-sensitive commercial real estate loans, the certainty of execution offered by private capital often outweighs the higher cost of funds. It’s a strategic trade-off that prioritizes asset control over immediate interest expense.

Evaluating Financial Mechanics: Rates, Points, and Risks

A sophisticated analysis of hard money loans begins with the deconstruction of the term sheet, where capital allocation meets rigorous risk-adjusted return profiles. Investors must view origination points, which typically range from 2% to 4% of the total loan amount, as a strategic cost of liquidity rather than a mere transaction fee. These points compensate the lender for the intensive due diligence and the accelerated deployment required in high-stakes Florida real estate markets. When capital is deployed into a distressed asset or a time-sensitive acquisition, the cost of debt is secondary to the opportunity cost of lost equity. This financial framework ensures that the lender’s interests align with the borrower’s ability to execute a value-add strategy with precision. It’s a calculated trade-off.

Interest Rate Determinants in 2026

Private lending benchmarks in 2026 remain tethered to the Federal Funds Rate, which sits at a target range of 4.25% to 4.50% based on recent stabilization trends. However, hard money loans command a premium due to the collateral-centric nature of the underwriting. Pricing is heavily influenced by geographic liquidity; a multi-family asset in a high-growth corridor like the Westshore District in Tampa will secure more favorable pricing than a specialized industrial site in a tertiary market. Lenders price for the volatility of the underlying asset and the compressed timeline of the transaction. This premium reflects the institutional rigor required to facilitate a closing in as little as 5 to 7 business days, a pace that traditional depository institutions cannot match. Investors who conduct a rigorous strategic comparison of private hard money lenders are better positioned to negotiate favorable rate structures that reflect their portfolio’s risk profile and execution history.

The Critical Importance of the Exit Strategy

Mitigating the risks of short-term debt relies entirely on a disciplined exit strategy. Most institutional investors utilize bridge loans or traditional commercial mortgages to retire high-interest debt once the asset’s value has been stabilized. A secondary exit involves the outright sale of the asset, a mechanism that requires a minimum 20% equity cushion to account for market fluctuations. Contingency planning is vital. If construction delays exceed 90 days or interest rates shift by 50 basis points, the borrower’s pro forma must demonstrate the capacity to carry the debt without eroding the principal. Successful stewardship of capital demands that every entry has a verified, multi-tiered departure point. It doesn’t leave room for ambiguity.

Analyze your next project with a partner that understands institutional-grade debt by exploring our bespoke capital solutions.

Establishing a Partnership with Institutional-Grade Lenders

Selecting a capital partner requires a rigorous evaluation of their historical performance and market depth. Professional investors must look beyond mere interest rates to identify a lender who provides strategic oversight and institutional stability. A vendor provides a service; a strategic ally provides a competitive advantage through analytical rigor and market cycle awareness. When you evaluate a brokerage firm, you’re assessing their intellectual capital and their ability to facilitate seamless capital deployment across diverse asset classes. For investors seeking hard money lenders Florida with institutional-grade standards, JGL Capital LLC serves as this disciplined steward, ensuring that hard money loans aren’t just transactional debt but are integrated into a broader, cohesive investment strategy.

- Evaluate the lender’s experience across multiple economic cycles to ensure stability during market volatility.

- Prioritize firms that offer bespoke structuring rather than rigid, one-size-fits-all loan products.

- Assess the firm’s access to diverse liquidity pools, which ensures consistent funding even when traditional markets tighten.

The JGL Capital LLC Approach to Stewardship

We leverage 30 years of industry experience, dating back to our foundations in 1994, to deliver bespoke financing solutions that reflect the gravity of high-stakes real estate management. Our process remains streamlined to respect the velocity of modern transactions. Initial inquiries typically receive a professional assessment within 24 to 48 hours. This speed ensures that your opportunities aren’t lost to bureaucratic delay. We maintain absolute transparency in every transaction, prioritizing the preservation of your capital and the integrity of the deal structure. Our team values long-term growth and disciplined wealth creation over speculative trends.

Initiating Your Capital Allocation Strategy

Successful funding begins with meticulous preparation for an asset-backed review. You’ll need to provide a comprehensive executive summary, a detailed schedule of real estate owned, and a clearly defined exit strategy for the subject property. Our role as your broker involves sourcing and securing private capital that aligns perfectly with your specific risk-adjusted return profiles. This disciplined approach transforms hard money loans from simple bridge financing into a sophisticated tool for portfolio optimization. However, the foundation of any successful capital deployment strategy begins with selecting the right hard money loan lenders who demonstrate institutional-grade transparency and operational stability. Contact JGL Capital LLC today to discuss how we can assist in securing your next real estate investment legacy through professional capital allocation and strategic partnership.

Optimizing Capital Agility in the 2026 Real Estate Market

Navigating the complexities of the 2026 market requires more than just capital; it demands a disciplined approach to asset acquisition. You’ve identified how hard money loans serve as a sophisticated instrument for bridging the gap between immediate opportunity and long-term stability. By prioritizing structural alignment and rigorous risk-adjusted returns, sophisticated investors bypass the inefficiencies of conventional financing. Success in this high-stakes environment hinges on the strategic oversight provided by a seasoned partner who values analytical rigor over speculative trends.

JGL Capital brings over 30 years of industry expertise to your investment strategy, offering a national lending reach that accommodates diverse real estate portfolios. We specialize in crafting bespoke funding solutions that address the specific requirements of institutional partners and high-net-worth individuals. Our commitment to value creation ensures your capital allocation remains precise and effective. Consult with our strategic advisors to secure your hard money financing and begin building a lasting legacy through deliberate, expert-driven action. You’re positioned to capitalize on today’s most compelling opportunities with confidence.

Frequently Asked Questions

Is a hard money loan easier to get than a traditional mortgage?

Yes, hard money loans offer a streamlined path to capital because the underwriting focuses on the asset’s liquidation value rather than the borrower’s personal income history. While conventional banks require a debt-to-income ratio below 43%, private lenders prioritize a 70% loan-to-value ratio on the property itself. This shift in stewardship allows for credit approvals that traditional institutions often decline because they don’t have the flexibility to look past credit scores.

What are the typical interest rates for hard money loans in 2026?

Interest rates for hard money loans in 2026 are projected to stabilize between 9.75% and 13.25% based on current Federal Reserve trajectories. These rates reflect the risk-adjusted returns required for high-speed, asset-based lending in the Florida market. Investors should expect to pay 2 to 4 points at closing to secure these specialized terms, ensuring the lender’s interests align with the project’s success and the firm’s long-term capital preservation goals.

How much of a down payment is required for a hard money loan?

Most institutional lenders require a down payment ranging from 20% to 30% of the acquisition price to maintain a safe equity cushion. If the project demonstrates a high after-repair value, some structures allow for 100% of construction costs to be financed. Maintaining a 25% equity stake isn’t just a requirement; it’s a strategic move that preserves the integrity of the investment’s risk profile throughout the renovation phase and ensures a disciplined capital allocation.

Can I use a hard money loan for a primary residence?

No, these financial instruments are strictly prohibited for use as a primary residence due to the consumer protection mandates within the 2010 Dodd-Frank Act. Lenders exclusively issue these funds for business purposes, targeting non-owner-occupied investment properties. We don’t deviate from this policy to ensure we maintain a disciplined focus on investment-grade assets, as violating this 100% commercial-use rule creates significant legal liabilities for both the borrower and the firm.

What happens if I cannot pay back a hard money loan by the end of the term?

Failure to satisfy the debt by the maturity date typically triggers a default interest rate that can escalate to 18% or higher. Lenders might offer a 3-month or 6-month extension for a fee of 1% of the principal balance if the project shows clear progress. If a resolution isn’t reached, the firm initiates a foreclosure process to recover the capital, protecting the portfolio’s overall strategic oversight and stability while maintaining its fiduciary duties.

How long does the approval and funding process typically take?

The entire lifecycle from initial application to wire transfer generally spans 5 to 10 business days. This pace is significantly faster than the 45-day window required by traditional banks for similar capital amounts. Our firm utilizes a rigorous but accelerated due diligence process that focuses on title clarity and valuation, ensuring that speed doesn’t compromise the precision of our risk assessment or the quality of the partnership established with our institutional clients.

Are hard money loans only for fix and flip investors?

No, these loans serve a diverse range of strategic objectives including land acquisition, commercial bridge financing, and multi-family property stabilization. Approximately 35% of our capital is deployed to investors who need to close quickly on distressed assets before transitioning to long-term debt. It’s a versatile tool for any sophisticated partner who values capital availability over the lower costs of slower, more bureaucratic financial institutions that cannot meet aggressive acquisition timelines.

What is the difference between a bridge loan and a hard money loan?

A bridge loan is a specific application of hard money designed to cover a temporary liquidity gap of 6 to 12 months. While all bridge loans utilize private capital, not all hard money structures are intended for such short durations. Bridge financing often targets stabilized assets with a 1.25 debt service coverage ratio, whereas broader hard money options might focus on distressed properties requiring extensive capital improvements to reach their peak value and optimization.