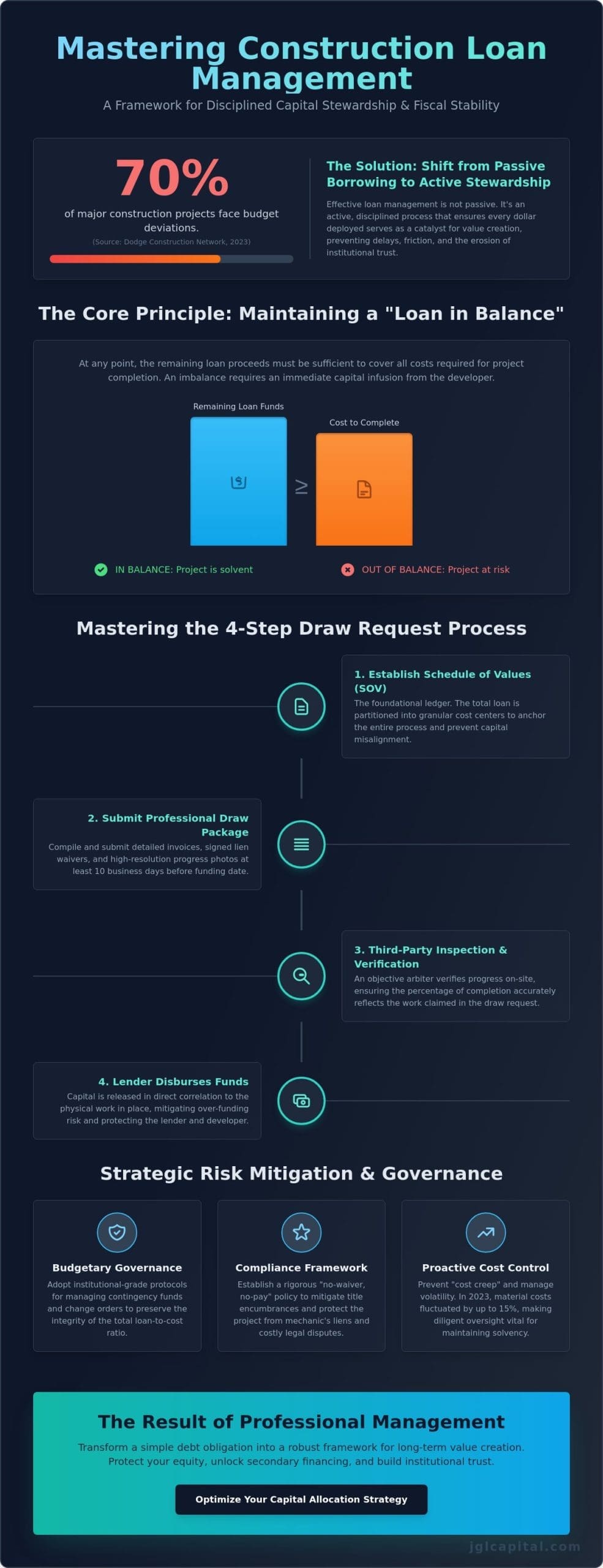

The integrity of a development project rests not on the strength of its foundation, but on the precision of its financial oversight. According to a 2023 report by the Dodge Construction Network, nearly 70% of major projects face budget deviations, often due to friction between capital flows and site progress. Understanding how to manage a construction loan requires a shift from passive borrowing to active stewardship, ensuring every dollar deployed serves as a catalyst for value creation. You likely recognize that even a minor delay in disbursement can trigger a cascade of operational friction, stalling momentum and compromising institutional trust.

This guide provides the framework necessary to master these complexities through a disciplined, institutional approach to loan administration. We’ll examine the mechanics of optimized draw schedules, the mitigation of structural risks, and the rigorous management of change orders that often lead to budget volatility. By the end of this analysis, you’ll possess a strategic blueprint for aligning lender disbursements with contractor performance, ensuring your project maintains the fiscal stability required for long-term success.

Key Takeaways

- Understand the fundamental distinction between static mortgage servicing and the dynamic oversight required to effectively master how to manage a construction loan.

- Learn to implement a disciplined draw request execution strategy anchored by a precise Schedule of Values to ensure capital flows align with project milestones.

- Adopt institutional-grade governance protocols for managing contingency funds and change orders to preserve the integrity of your total loan-to-cost ratio.

- Establish a rigorous “no-waiver, no-pay” compliance framework to mitigate title encumbrances and protect the project from legal disputes.

- Explore the strategic advantages of asset-based underwriting and private lending partnerships in optimizing capital allocation for high-stakes development.

The Architecture of Construction Loan Management

Effective capital stewardship begins with a precise definition of construction loan management; it is the systematic oversight of capital disbursement and the verification of project milestones. While traditional mortgage servicing involves a static debt structure, construction financing is inherently dynamic. It requires a sophisticated understanding of how to manage a construction loan to ensure that the financial lifecycle of the project mirrors its physical development. Central to this process is the “loan in balance” concept. This primary metric dictates that at any given moment, the remaining loan proceeds must be sufficient to cover all costs required to reach project completion. If the cost to complete exceeds the remaining funds, the loan is out of balance, necessitating an immediate capital infusion from the developer to rectify the shortfall.

This financial architecture relies on a triad of stakeholders. The lender provides the capital, the developer executes the vision, and the third-party inspector serves as the objective arbiter of progress. By utilizing detailed cost breakdowns and site inspections, these parties maintain the integrity of the capital stack. This level of scrutiny is essential in high-stakes environments where a single budgetary oversight can jeopardize the entire investment. Understanding Floor Loans and their associated holdbacks is critical here, as these mechanisms often dictate the initial release of funds based on occupancy or performance hurdles, ensuring that capital is not deployed prematurely.

The Core Objectives of Capital Oversight

The primary objective of capital oversight is the mitigation of over-funding during the initial stages of development. Strategic management ensures that disbursements align with the physical appreciation of the asset. This prevents the “front-loading” of costs, where a developer might draw down excessive capital for early-stage mobilization or soft costs. By maintaining a disciplined draw schedule, the lender protects the project from potential abandonment. This rigorous alignment of cash flow with tangible progress ensures that the collateral value remains ahead of the debt obligation throughout the 24 to 36-month development cycle typically seen in mid-market projects.

Why Professional Management is Non-Negotiable

Professional management serves as a safeguard for the developer’s equity. Without disciplined oversight, projects often succumb to “cost creep,” which rapidly erodes the profit margin. In the 2023 construction market, where material costs fluctuated by as much as 15% in certain regions, such oversight proved vital for maintaining solvency. Strategic management also preserves secondary financing options. Lenders are more inclined to provide mezzanine debt or preferred equity when a project demonstrates a track record of transparent, accurate capital allocation. Learning how to manage a construction loan through a professional lens transforms a simple debt obligation into a robust framework for long-term value creation and institutional trust.

Mastering the Draw Request Process: A Step-by-Step Execution

The draw request represents the operational pulse of the construction lifecycle. It serves as the primary conduit through which capital flows from the lender to the project site. Effective stewardship requires a rigorous approach to the Schedule of Values (SOV). This document serves as the foundational ledger, partitioning the total loan into granular cost centers. Without a precise SOV established at the onset, the risk of capital misalignment increases. Standardized reporting isn’t optional; it’s a requirement for maintaining the trust of institutional partners. Success in learning how to manage a construction loan hinges on this initial alignment of expectations.

The Anatomy of a Professional Draw Request

A professional draw package consists of more than just a total figure. It requires a detailed compilation of invoices, lien waivers, and high-resolution progress photographs. Lenders typically employ the percentage of completion method to calculate disbursements. This ensures that the capital released correlates exactly with the physical work in place. According to 2024 industry standards, most institutional lenders require these submissions at least 10 business days prior to the desired funding date. Understanding the nuances of How Construction Loans Work allows developers to anticipate these requirements. This precision prevents the common friction points that stall large-scale developments. Verification protocols are strict. Lenders won’t release funds for materials that aren’t securely stored on-site or in a bonded warehouse.

Navigating the Inspection and Funding Cycle

Navigating the inspection cycle demands proactive coordination. Third-party inspectors act as the lender’s eyes on the ground. They verify that the 60% completion claimed on a line item, such as HVAC rough-ins, matches the actual site conditions. If an inspector identifies a discrepancy, the funding for that specific item will be adjusted or withheld. Promptly addressing these variances is essential for maintaining project liquidity. Once the inspection report is finalized and the lender approves the package, the wire transfer process begins. A disciplined developer ensures that subcontractor payments are issued within 48 hours of receipt. This speed preserves the project’s momentum and safeguards against mechanics’ liens. Mastering this cycle is the core of how to manage a construction loan with institutional-grade proficiency. For those seeking to refine their approach to strategic capital oversight, aligning with a partner who understands these complexities is vital.

- Establish a clear Schedule of Values before the first shovel hits the ground.

- Sync contractor billing cycles with the lender’s specific 30-day draw window.

- Maintain a digital repository of all receipts and invoices for year-end audits.

- Respond to inspection discrepancies within 24 hours to avoid funding delays.

Strategic Risk Mitigation and Budgetary Governance

The primary challenge in learning how to manage a construction loan effectively involves the proactive administration of the contingency fund. This reserve, typically established at 5% to 10% of total hard costs, serves as a strategic buffer against volatile commodity prices and unforeseen site conditions. Successful developers don’t view this fund as a discretionary pool for aesthetic upgrades; they treat it as a critical component of risk-adjusted returns. Maintaining the integrity of the original pro forma requires a disciplined distinction between hard costs, which constitute the physical structure, and soft costs such as architectural fees, permitting, and legal expenses. Capital leakage often occurs when soft costs exceed the initial 20% to 30% allocation, necessitating a rigorous monitoring system to preserve the project’s liquidity. By utilizing new construction loans as a sophisticated tool for scalable growth, institutional partners can maintain a stable loan-to-cost ratio while expanding their portfolios across diverse jurisdictions.

Managing Cost Overruns and Budget Volatility

Identifying early warning signs of budget depletion is essential for maintaining capital stewardship. A variance of 15% or more in any specific line item should trigger an immediate internal audit. When a project becomes “out-of-balance,” the remaining loan proceeds are no longer sufficient to complete the defined scope of work. In these instances, the developer carries the institutional responsibility to infuse additional equity to re-balance the ledger. Effective managers re-allocate funds between line items only after verifying that such shifts won’t compromise the structural integrity or the eventual marketability of the asset.

Change Order Protocols and Approval Workflows

The Compliance Framework: Documentation and Lien Management

Effective capital stewardship requires a rigorous administrative infrastructure to mitigate the inherent risks of real estate development. Understanding how to manage a construction loan necessitates an unwavering commitment to documentation, particularly regarding the mitigation of title encumbrances. This phase of the project demands a disciplined approach to legal safeguards, ensuring that every dollar disbursed is protected by a corresponding release of liability. Without a structured compliance framework, the project’s financial integrity remains vulnerable to third-party claims that can jeopardize the entire investment thesis.

The Critical Role of Lien Waivers

Lien waivers serve as the primary defense against title encumbrances and protracted legal disputes. A sophisticated ‘no-waiver, no-pay’ policy must be implemented across all tiers of subcontractors to ensure that the chain of title remains clear. This process involves distinguishing between conditional waivers, which are provided prior to payment, and unconditional waivers, which acknowledge the receipt of funds. It’s essential to collect these documents from both general contractors and major material suppliers to prevent surprise filings.

Proper documentation does more than protect current equity; it facilitates a smooth transition to commercial real estate loans for permanent financing. Lenders providing take-out financing require a pristine record of lien releases to ensure their security interest is unencumbered. A 2023 industry analysis suggests that projects with disorganized lien tracking experience a 30% higher rate of closing delays during the stabilization phase. Maintaining a meticulous digital ledger of these waivers is a hallmark of professional capital management.

Title Oversight and Legal Safeguards

The lender’s primary concern is maintaining a first-lien position throughout the construction lifecycle. To achieve this, the draw process must include title updates and date-down endorsements. These periodic checks confirm that no mechanics’ liens have been recorded since the previous disbursement. If a lien is discovered, it must be addressed through bonding or payment before the next draw is authorized, as unresolved claims often serve as default triggers in loan agreements.

- Insurance Requirements: Maintaining robust builder’s risk and general liability coverage is mandatory to protect against physical loss and third-party claims.

- Final Title Policy: Upon project completion, a final title policy must be issued to reflect the finished improvements and the absence of outstanding construction-related debts.

- Strategic Oversight: Regular audits of insurance certificates ensure that all active subcontractors maintain coverage limits that align with the master policy.

Rigorous documentation is the foundation of successful project delivery. When considering how to manage a construction loan, the emphasis must remain on the precision of these legal safeguards. This methodical approach ensures that the developer’s interests remain aligned with those of the institutional partners, preserving the long-term value of the asset. For a comprehensive evaluation of your project’s compliance structure, partner with JGL Capital to ensure your capital is managed with institutional-grade discipline.

Optimizing Capital Allocation through Private Lending Partnerships

The final stage of capital stewardship involves selecting a lending structure that accommodates the inherent volatility of large-scale development. Sophisticated developers recognize that the efficacy of their financial strategy depends largely on the agility of their lending partner. While traditional banking institutions often impose rigid constraints that can stifle momentum, private capital offers a bespoke alternative. This approach prioritizes the intrinsic value of the development over standardized metrics. Understanding how to manage a construction loan effectively requires an appreciation for asset-based underwriting, which shifts the focus from narrow credit scores to the project’s ultimate viability and the developer’s execution history. By aligning with a private lender, investors secure a partner capable of navigating the complexities of high-stakes real estate without the structural delays inherent in retail banking.

The Private Money Advantage: Speed and Flexibility

Institutional bureaucracy often creates friction that can jeopardize project timelines. In a market where a 30-day delay can result in a 5% increase in material costs, speed isn’t just a convenience; it’s a financial necessity. Private lending eliminates these bottlenecks by providing rapid capital deployment and customized draw schedules. These schedules aren’t static. They’re engineered to match the specific cadence of a project’s unique lifecycle. JGL Capital evaluates the property’s potential and the developer’s track record, allowing for a more nuanced risk assessment than a traditional bank’s algorithm. It’s a system designed for those who value precision and responsiveness. This flexibility allows developers to pivot when market conditions shift, ensuring that capital remains a tool for growth rather than a source of administrative burden.

Building a Lasting Legacy through Strategic Partnership

Effective capital management extends beyond the initial build. It’s about the strategic transition from construction to stabilized real estate investing. With 30 years of industry expertise, JGL Capital functions as a disciplined steward of wealth. We’ve navigated multiple market cycles since the early 1990s, providing the analytical rigor necessary for portfolio optimization. This long-term perspective ensures that every project contributes to a lasting legacy of wealth preservation and growth.

Developers who master how to manage a construction loan through these strategic alliances often achieve superior risk-adjusted returns. Our firm acts as a strategic ally rather than a mere service provider, emphasizing the alignment of interests and the delivery of tailored solutions. We believe that disciplined capital management is the cornerstone of long-term wealth. To begin this collaborative process and ensure your capital is allocated with maximum efficiency, Consult with JGL Capital for your next project and secure a foundation for your future portfolio.

Advancing Your Development Strategy through Institutional Discipline

Understanding the intricacies of capital stewardship is essential for any developer seeking to preserve project integrity and ensure long-term value creation. Effective oversight requires a disciplined approach to the draw request process and a rigorous commitment to lien management. These operational pillars don’t just mitigate risk; they provide a framework for institutional-grade execution across the entire project lifecycle. When you’re determining how to manage a construction loan, the focus must remain on precise capital allocation and the maintenance of asset-backed security.

JGL Capital brings over 30 years of industry expertise to every partnership, offering national reach and institutional-grade standards that prioritize property value. Our approach moves beyond simple transactions to provide strategic oversight that aligns with your specific investment objectives. By leveraging deep-seated analytical rigor, we ensure your project’s financial architecture remains robust from inception to completion. We focus on the alignment of interests to deliver bespoke solutions that stand the test of time.

Secure Your Project’s Future with JGL Capital’s Strategic Construction Financing

Your vision deserves a partner who values disciplined growth and integrity as much as you do.

Frequently Asked Questions

What is a ‘loan in balance’ and why is it critical for construction loan management?

A loan remains in balance when the remaining undisbursed loan funds, combined with the borrower’s equity, are sufficient to complete the project. This equilibrium ensures that the lender’s collateral value is protected throughout the construction lifecycle. If a cost overrun occurs, the borrower must inject additional capital to restore this balance before any further draws are processed. Maintaining this ratio is a fundamental requirement for institutional capital stewardship.

How often can I request a draw on my construction loan?

Borrowers typically request draws on a monthly basis, aligning with the standard billing cycles of general contractors and subcontractors. This frequency allows for a steady flow of capital while maintaining rigorous oversight of the project’s physical progress. Some institutional lenders may permit bi-monthly draws if the project scope exceeds $10,000,000 in total capitalization. Precise scheduling ensures that liquidity remains available for critical milestones without compromising due diligence.

What happens if my construction project goes over budget?

When a project exceeds its initial pro forma budget, the borrower’s required to cover the deficit using personal equity to maintain the loan in balance status. Lenders monitor these variances through monthly cost-to-complete reports. According to a 2023 study by the Project Management Institute, 35 percent of large-scale projects experience a budget deviation of at least 10 percent. Learning how to manage a construction loan involves anticipating these contingencies through a 5 to 10 percent reserve fund.

Why does the lender require a third-party inspection for every draw?

Lenders mandate third-party inspections to verify that the work described in the draw request has been physically completed to the required standard. These inspectors provide an objective assessment that mitigates the risk of over-funding or paying for materials not yet installed on-site. This verification process protects the lender’s interest and ensures the project remains on schedule for its 12 or 24 month completion target. It’s a standard risk mitigation protocol in institutional lending.

What is the difference between a conditional and unconditional lien waiver?

A conditional lien waiver becomes effective only after the specified payment has been cleared by the bank, whereas an unconditional waiver is effective immediately upon execution. Contractors use conditional waivers to protect their right to file a lien if payment isn’t received. Unconditional waivers are typically submitted after the funds have reached the contractor’s account, providing the lender with definitive proof that no legal claims exist against the property’s title.

Can I use a construction loan to purchase the land and fund the build simultaneously?

You can utilize a construction-to-permanent loan to finance both the land acquisition and the subsequent structural development within a single closing. This integrated financial structure reduces total closing costs by consolidating two separate transactions into one instrument. Lenders often require a minimum 20 percent down payment based on the total acquisition and construction cost to mitigate the higher risk profile of vacant land. This approach streamlines the path toward project commencement.

How do I transition my construction loan into a permanent mortgage once the project is finished?

The transition to a permanent mortgage occurs automatically in a “one-time close” loan once the local municipality issues a final Certificate of Occupancy. If you’ve secured a “two-close” loan, you’ll need to re-qualify for a traditional mortgage and pay a second set of closing fees. Mastering how to manage a construction loan requires selecting the right structure during the initial underwriting phase to avoid unnecessary interest rate volatility during the 30 year amortization period.

What documentation is required for the final draw and project closeout?

The final draw requires a Certificate of Occupancy, final unconditional lien waivers from all major subcontractors, and a signed letter of completion from the architect. Lenders also mandate a final inspection to confirm that 100 percent of the contracted work is finished. This closeout phase typically accounts for the final 5 to 10 percent of the total loan amount, which is held back until all punch-list items are resolved. Diligent documentation ensures a seamless transition to permanent financing.